There’s no question now that the Federal Reserve is in full hawkish mode. The release last week of the minutes of the previous FOMC meeting left no doubt that they are on an aggressive path to squelch inflation through demand destruction and tightening financial conditions. There is a very high probability that they will be raising rates by 0.50% at the next two to three meetings in an effort to get the Federal Funds Rate to what they deem to be neutral. This is the rate in which inflation can come down to its long-term trend rate without hurting economic growth. This is estimated to be 2.25% to 2.50% but it’s a very theoretical concept so we don’t really know what that number is and it can always be changing. Goldman Sachs, which has left a lot to be desired as economic forecasters, says it could be north of 4% in this cycle.

The Fed also finally announced, far too belatedly I might add, that they’re going to start shrinking the balance sheet by approximately $95 billion per month with the goal of reducing it by about $1.1 trillion per year. The consensus opinion is that the Fed’s major policy error was not only being too accommodating for too long, but it should have started reducing its balance sheet much earlier. Chairman Powell kept categorizing the run-up in inflation as transitory which was met with a lot of skepticism by investors. As he has done in the past, Powell pivoted when he saw that he was either wrong or the world had changed.

Prior to the release of the minutes Lael Brainard, who is in line to be Vice Chairman of the Federal Reserve and is considered one of the more dovish members, came out and said that the Fed was essentially behind the curve and needed to start cutting its balance sheet more significantly and rapidly than investors were anticipating. This speech was delivered to prime the market ahead of the minutes. Treasury yields increased, especially on the long end. This chart shows how yields have gone up almost 0.70% over the past month, which is a huge increase on a percentage basis.

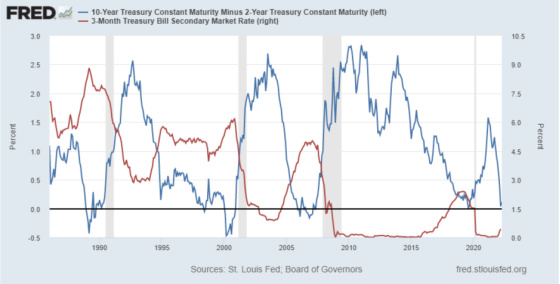

And while most of the yield curve remained inverted with shorter rates being higher than longer ones, the differential between the 10s and 2s went back to being positive as the following chart shows.

One might look at this as a positive sign for future economic growth as inverted yield curves are historically precursors to recession. And with the spread between 10s and 2s now being positive perhaps one could interpret this as a sign that future economic growth is looking more positive. Unfortunately, if history is any guide, the opposite is usually the case. The yield curve turning positive after being negative almost always foreshadows a recession.

One can see from the chart above that the last four recessions (shaded vertical columns) were all preceded by the spread between the 10s and 2s either being negative or very close to zero and then turning positive before the onset of the recession. Investors seem to be factoring in a recession sometime in 2023 as the consensus forecast.

At the same time, or maybe because of a hawkish Fed, the market is pricing a large number of rate increases in a relatively short period of time in conjunction with rising fears of a recession. The Fed seems intent on breaking something in the economy by curtailing demand or tightening financial conditions to make it more costly to access capital to grow and speculate.

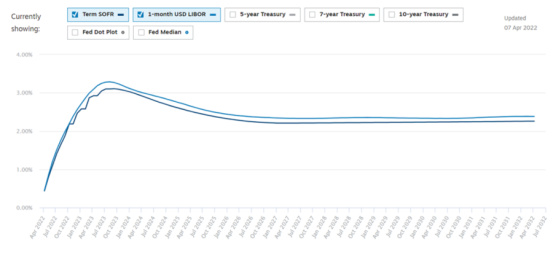

The following chart is the forward curve for 30-day LIBOR and Term SOFR published by Chatham Financial. One can see that the market is pricing these two indices to peak in August 2023 and then start coming back down from there.

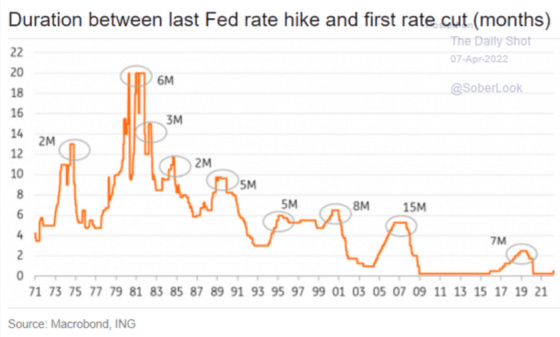

The peak in rates and almost immediate drop goes counter to most previous cycles in which the time between the last rate hike and subsequent cut averaged approximately six months as the following chart shows.

Since we are predominantly variable-rate borrowers in which our loans are tied to short-term interest rates, I’m particularly curious to see what happens to short rates (3-month T-Bills in this example) after the yield curve inverts and prior to a recession. The red line in the chart below is the 3-month T-Bill yield.

If a recession is really on the horizon in 2023, then it’s conceivable the Fed may not be able to move rates as high as the market is pricing in. One contrarian point of view comes from a quantitative analyst at SocGen who correctly made an out of consensus call in 2018 that the Fed would have to pivot and start cutting rates since it could go no higher than 2.50%. He turned out to be right.

His current belief is that in our more highly leveraged, financialized economy, rate hikes can only capture approximately 70% of the previous rate cuts because markets have come to rely on lower rates in each cycle.

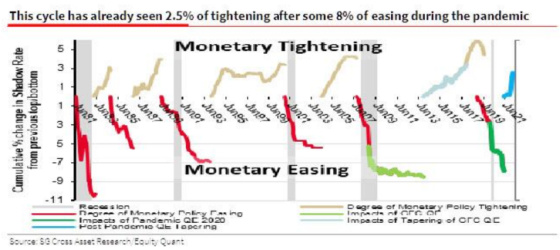

Since rates went down to 0% the analyst uses the shadow rate to calculate how negative rates came down to at the bottom during the 0% period. He believes that they dropped to -5.00%, which was an estimated 8.00% cumulative reduction. 70% of this is 5.60% which would push the maximum Fed Funds Rate to 0.60%, or 1.00% to round up. He believes that there has already been 2.50% tightening with just a 0.25% increase in the Fed Funds Rate when combined with the announcement of quantitative tightening (the Fed reducing its balance sheet). Here is his graph showing the previous easing and tightening cycles.

Prior to Brainerd’s speech, he was anticipating that the remaining 3.00% of tightening would come from bringing the Fed Funds Rate to 1.50% (1.25% increase from current rates) and the other 1.75% coming from quantitative tightening. After her speech, however, he now believes that the maximum Fed Funds Rate in this cycle will be 1.00% (0.75% increase from current rates) with the other 2.25% coming from quantitative tightening.

One can see from the next chart that 5.50% of tightening is quite large relative to past cycles. In addition, tightening stops before the economy enters into a recession.

And let’s not forget that every time the Fed embarks on a tightening cycle, a financial crisis almost always ensues.

Let’s add to the mix much higher mortgage rates.

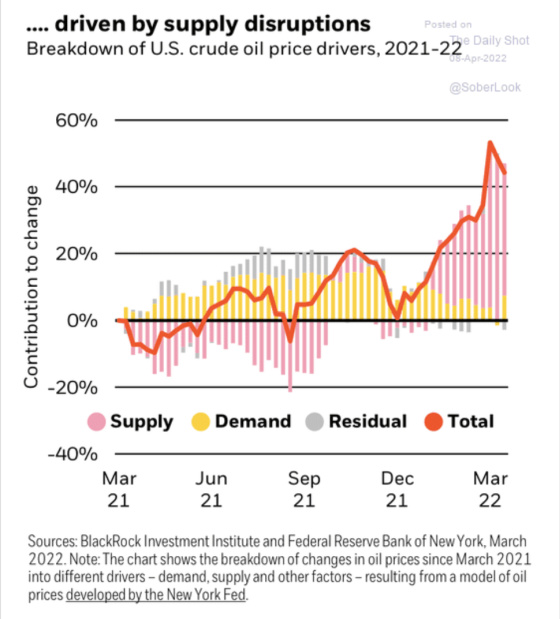

As well as much higher gas prices which may be here for a while due to supply challenges being quite acute with OPEC having major issues increasing production.

OPEC has a lot of incentives to meet its quota given how high oil prices are. And yet, most countries are falling short which has led to a shortfall of close to 700,000 barrels per day.

OPEC’s shortfall, on top of challenges for shale producers to access labor, sand, pipelines, etc. has added to the supply issues and has left U.S. inventories at very low levels.

And let’s not forget about much higher food prices causing the potential for social instability in poorer countries, the war in Ukraine and the collateral effects of that from an energy and humanitarian standpoint, possible over-ordering by firms to make sure they have enough inventory in the face of supply challenges, and China’s massive challenges with Covid and the bursting of its real estate bubble, the Fed is walking on a tightrope between fighting inflation and pushing the economy into a recession and having to stop sooner than it was anticipating or even having to reverse course and lower rates.

It will be interesting to see how the Fed’s tightrope walk will unfold. If history is any guide, then they will not be very successful and this will lead to a recession, financial distress, or a combination of the two.

{kind=link}

Excellent article. The US ran a 2.8T budget deficit in 2021. Through the first four months of 2022, it was over $400B or roughly $1.2T annually . That’s quite a drop in credit expansion. Credit needs to expand around 2% per year to forestall recession. Can the private sector make up the difference? We’ve had significant asset inflation the last couple of years, financial assets and real estate are expensive. Where are the investable opportunities? Are we addicted to budget deficits driving credit growth?

I completely agree. I’ve written about the contraction in fiscal expansion previously but it is going to be a substantial economic headwind as well. Thanks for pointing this out.