Our supply chain debacle is front and center for virtually every person in the U.S. in one way or another. This chart is fascinating to me in that orders are now about 5% above previous cycle peaks.

And yet, the following charts show how during those other times we had nowhere near the supply chain issues that we are experiencing now. One can see how challenged the global supply chain is from the following charts.

With the advent of Covid supplier deliveries have never been slower over the last 20 years or so.

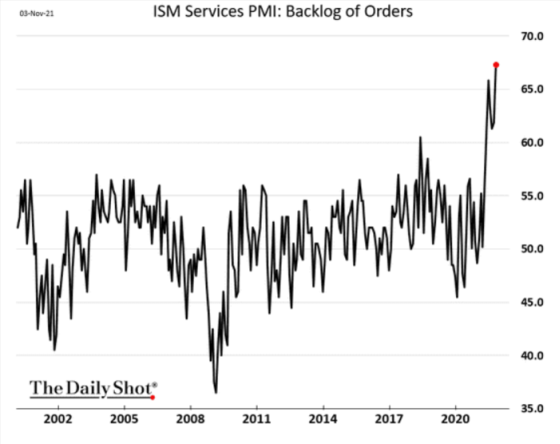

This has led to a very large backlog of orders, far beyond the previous cycle peaks that took place in the first chart related to manufacturing new orders.

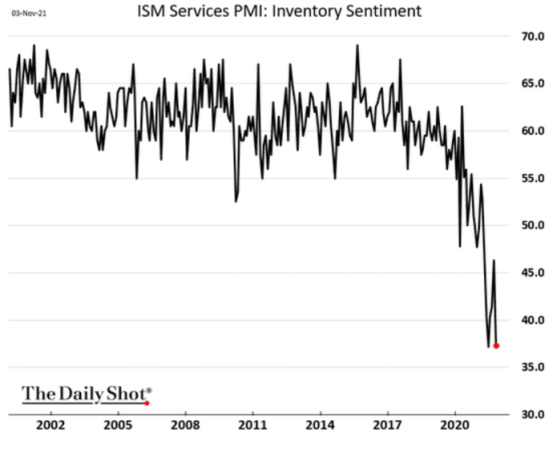

This has led to negative sentiment related to inventories. Firms believe they are way understocked.

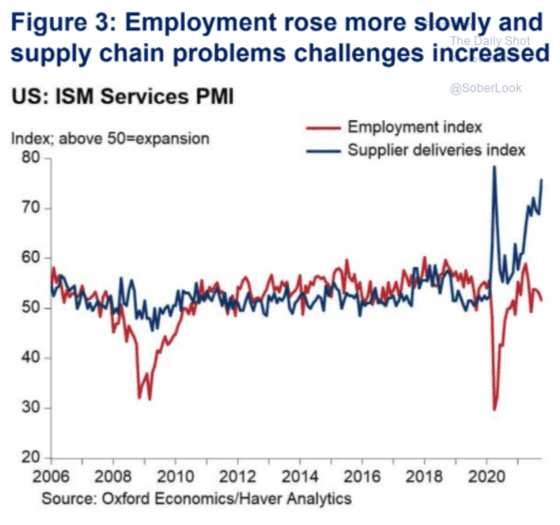

In spite of the slower delivery times, which would suggest the need for more labor, the employment index is fairly subdued. This would seem to corroborate the very challenging labor market for employers, particularly in manufacturing.

Supply Chain – A Truck Drivers Perspective

I read a very interesting post on Medium written by a truck driver who went into great detail as to why we are dealing with a long-term, systemic problem. I love the specificity of the article because the global supply chain is very complex and has so many moving parts so a detailed analysis about one particular aspect of it, domestic trucking to and from ports, is very valuable to read.

As I’ve said before, one of my favorite quotations is that “It’s better to be a meaningful specific than a wandering generality.”Click To TweetThere is a lot more to learn from specifics than generalities. It’s worth reading but I will point out the highlights for those who want to get the gist of it.

There is a huge backlog of shipping containers at sea that need to be unloaded. Unfortunately, most trucking companies won’t get involved with that business. The bottlenecks are tremendous which is resulting in terribly long wait times for trucks to get in to deliver and to leave with cargo. They don’t have enough throughput in terms of the number of lanes available for trucks to go in and out and the ports are incredibly understaffed.

Most drivers are independent contractors which means that the costs of such long wait times are very painful financially. They are paid by the load, regardless of how long it takes to pick it up and drop it off or vice versa. In addition, they are responsible for 90% of the cost of operating the truck (repair, fuel, maintenance, etc.). According to the author, there is no guarantee of receiving a minimum wage and there are situations in which drivers work over 70 hours per week and still owe money to the truck owners. So when Covid led to massive port congestion, drivers stopped showing up because it didn’t make financial sense to do so.

In addition to labor issues, there is a shortage of railcars to transport containers away from ports. There is also a shortage of container chassis, which is the trailer the container sits on. This is something that wouldn’t cross my mind, but why would it be since I don’t work in that field. And that’s the point. It’s specific, nuanced knowledge that gives curious, intelligent, well-informed, industry professionals an edge as compared to an ill-informed outsider like me. The chassis is typically owned by the shippers versus the trucking companies. The chassis shortage is creating even longer wait times for truckers.

Trucking companies are also lacking storage on their lots which are leading desperate ports to clear out containers to anywhere they can find in order to be able to unload containers coming in by boat. This does not entail a plan to deliver the freight so eventually, containers will stack up at ports until sitting containers are delivered. And, unfortunately, this is not going to happen easily any time soon.

Most international containers have to be unloaded by hand because they don’t come in on pallets. This is hard work and is carried out in warehouses by relatively lower-paid workers. Many warehouse crews got laid off during Covid and a great number have not come back. This has led to temp labor doing the work and this has led to chronically short-staffed warehouses. The contents are separated into pallets for drivers to pick up and drop off at many different destinations. What used to take the author 20 to 30 minutes to pick up freight at a warehouse now takes two to three hours. The whole system is backed up.

His outlook is rather pessimistic.

We are not in Kansas anymore to quote Dorothy to Toto.Click To TweetFast and relatively inexpensive shipping is history. If you want it faster than the new normal you will have to pay for it to jump to the front of the line. Expect what used to take a week or so to take much longer. There are not enough qualified drivers to adopt a 24/7 delivery system safely. It’s just not possible according to the author.

What we have is a system with a limited amount of trucks and qualified drivers, many of whom are already working 14 hours a day (legally, the maximum they can), and now the supposed fix is to have them work 24 hours a day, every day, and not stop until the backlog is cleared. It’s not going to happen. It is not physically possible. There is no “cavalry” coming. No trucking companies are going to pay to register their trucks to haul containers for something that is supposedly so “short term,” because these same companies can get higher rate loads outside the ports. There is no extra capacity to be had, and it makes NO difference anyway, because If you can’t get a container unloaded at a warehouse, having drivers work 24/7/365 solves nothing.

What it will truly take to fix this problem is to run EVERYTHING 24/7: ports (both coastal and domestic),trucks, and warehouses. We need tens of thousands more chassis, and a much greater capacity in trucking.

It seems to me that we are going to be dealing with a long-term challenge here. Perhaps we are starting to see some loosening of the labor market which could potentially help the situation over time as the jobs report last week was quite strong with the previous two months revised sharply higher as well.

And yet, the bond market pushed interest rates lower in spite of such a strong jobs report.

And while there is understandable concern about inflation and that maybe the Federal Reserve is too slow to react, my question is how will tighter monetary policy help improve the global supply chain problems?

If the only way is to crush demand then that is a possibility. If that is not the case, then I’m not sure if higher interest rates are the answer. Perhaps bond investors are factoring in a self-correcting mechanism of higher prices and supply chain bottlenecks causing demand destruction which will better calibrate supply and demand via a slower-growing economy.

I will leave you with the following chart that I find absolutely fascinating and may help determine which direction the Fed takes. The Atlanta Fed has come up with GDP Now which is its best real-time estimate of the annual percentage change in U.S. GDP. It then compares its estimate with the range of private economists. One can see that the Atlanta Fed’s estimate has not only been higher than the upper range of the private economists’ estimates, but it is rapidly accelerating.

It will be interesting to see what happens to the estimates in the wake of the strong jobs report. Regardless, the most real-time indicators of all are the yields on the 10-year Treasury, which dropped almost 4 basis points after the jobs report, and the 2-year Treasury which increased approximately 1 basis point. The latter is more sensitive to Fed policy while the former is more indicative of long-term economic growth. My speculation is that the combination of a less accommodative Fed and global supply chain challenges will crimp demand and lower economic growth over the next year, contrary to what the Atlanta Fed’s model is showing.

{kind=link}

Leave a Reply