The Great Financing Question: From a Decade of Floating-Rate Success to a New Era of Uncertainty

One of the most important strategic decisions we make as multifamily owners is not simply what properties to buy, but how to finance them. The choice between floating-rate and fixed-rate debt can have an enormous impact on investment outcomes.

For much of our history, we were enthusiastic users of floating-rate debt. Between roughly 2012 and early 2022, that strategy proved exceptionally successful. The environment was almost ideal for floating-rate borrowers: short-term interest rates remained extraordinarily low, interest rate caps were inexpensive, lending spreads were attractive, and the flexibility of floating-rate loans created opportunities to refinance whenever market conditions improved.

Then the world changed.

The End of a Remarkable Era for Floating-Rate Borrowers

The Federal Reserve’s rapid response to inflation beginning in 2022 produced one of the most dramatic increases in short-term interest rates in modern history. The very feature that had made floating-rate debt so attractive—its sensitivity to short-term rates—became its greatest weakness.

Borrowers who had benefited enormously from floating debt for more than a decade suddenly faced sharply higher debt costs, expensive interest rate caps, and a refinancing market that became far less forgiving.

While we had profited handsomely from our floating-rate strategy over many years, we also gave back a meaningful portion of those gains during this period. The experience reinforced an important lesson: a financing strategy should not be evaluated only by its expected return, but by its resilience under adverse scenarios.

Our Refinancing Strategy Since 2024

Beginning in 2024, we took a hard look at our debt portfolio and made a significant strategic shift.

Since then, we have refinanced 27 loans, and we chose fixed-rate financing on 23 of them. The remaining four loans were debt fund executions where fixed-rate alternatives either did not exist or were not economically viable.

This decision was not based on a strong conviction that long-term rates were about to fall. In fact, we had several concerns that made maintaining large floating-rate exposure less attractive.

First, we were not particularly bullish on apartment NOI growth over the next several years. The multifamily sector was entering a period of elevated new supply, rent concessions, and more modest revenue growth. In a world where NOI growth might be limited, relying on future earnings growth to offset potentially higher interest expense felt imprudent.

Second, we believed that solving today’s refinancing problem had significant value. A loan that could be refinanced comfortably today might not be so easy to refinance in the future if interest rates moved higher or lenders became more conservative in their underwriting assumptions. Avoiding the possibility of being forced into a difficult cash-in refinance was worth sacrificing some of the flexibility associated with floating-rate debt.

Third, we did not believe short-term rates were likely to decline enough to create a substantial advantage for floating-rate borrowers. At the same time, fixed-rate spreads were exceptionally attractive. The market was effectively offering us relatively inexpensive insurance against the risk of higher short-term rates and a more challenging refinancing environment.

In our view, the risk-reward tradeoff of remaining floating simply was not compelling.

Taking Advantage of Floating-Rate Flexibility

One advantage we did have was that our floating-rate loans generally carried much greater prepayment flexibility than fixed-rate debt.

That allowed us to remain patient and opportunistic. Rather than locking into fixed rates at unfavorable moments, we could wait for periods when Treasury yields moved to attractive levels and then bring loans to market.

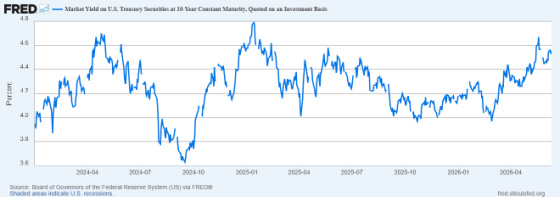

As the attached chart of the 10-year Treasury yield illustrates, there were several periods during 2024 and 2025 when long-term rates temporarily declined. We used those windows to execute refinancings and lock in fixed-rate debt.

Looking back, we are very pleased with this decision. By converting a substantial portion of our portfolio to fixed-rate financing, we not only reduced our exposure to future interest-rate volatility, but also eliminated the need to purchase expensive interest-rate caps.

The New Question: What Do We Do With the Next 20 Loans?

Today, however, the decision is far more nuanced.

We have 22 loans maturing between now and 2027, and the optimal strategy is much less obvious than it was over the last two years.

The reason is that the market has changed.

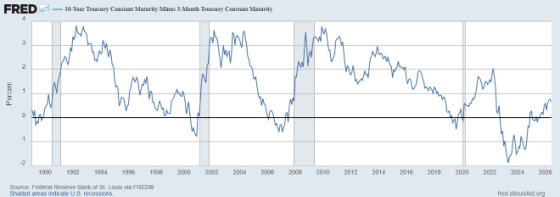

While the yield curve has steepened somewhat from its deeply inverted levels, the spread between short-term and long-term rates remains relatively narrow by historical standards. The second chart, showing the difference between the 10-year Treasury yield and the 3-month Treasury yield, illustrates that although the inversion has ended, the curve is still far from steep by historical measures.

This creates a more difficult tradeoff.

On one hand, long-term Treasury yields are now near the upper end of their recent trading range. Locking in fixed-rate debt today means accepting a higher starting rate than was available during some of the windows we were able to capture in 2024 and 2025.

On the other hand, floating-rate debt has become less attractive in another important respect: interest-rate cap costs have increased materially. The options market is now assigning a higher probability that the Federal Reserve could be forced to raise rates again, rather than simply continue cutting rates. In other words, the downside protection that floating-rate borrowers require has become more expensive.

A Different Kind of Interest-Rate Environment

One of the more interesting developments recently has been the divergence between short-term funding rates and longer-term Treasury yields.

SOFR has declined as expectations for Federal Reserve policy have moderated, while longer-term Treasury yields have remained elevated due to concerns about persistent inflation, large federal deficits, Treasury supply, and a higher term premium demanded by investors.

This distinction matters because it means the old assumption—that short-term rates will naturally remain below long-term borrowing costs—may no longer hold in the same way it did during the decade following the Global Financial Crisis.

The market may be transitioning from a world dominated by central-bank policy to one where fiscal deficits, inflation uncertainty, and a higher cost of capital play a much larger role.

The Right Question Is No Longer “Fixed or Floating?”

In our view, the financing decision today is not a simple choice between fixed and floating debt.

The more important question is:

How much interest-rate risk are we being compensated to accept?

During the years following the financial crisis, the answer was clear: floating-rate debt offered compelling economics with limited perceived downside.

Today, the answer is far less obvious.

Fixed-rate debt provides certainty and protection against a scenario where inflation proves sticky, rates rise again, or lenders become more conservative. Floating-rate debt provides flexibility and the potential to benefit if short-term rates decline more than the market currently expects.

The challenge over the next several years will be balancing those competing risks.

The market may be transitioning from a “Fed shock” regime to a “fiscal/inflation uncertainty” regime.

That tends to create:

- more volatile long rates,

- but potentially less persistently restrictive short rates.

If that interpretation is right, floating debt could again become more competitive than it was in 2022–2024 — but probably without the nearly one-way advantage it enjoyed in the 2010s.

And yet, with all of the very understandable concerns for higher structural inflation due to very large persistent deficits and energy prices having increased significantly due to the Iran war, inflation expectations seem to still be very well anchored.

One can see from how this post has wavered without any clear conviction, as there are so many crosscurrents and variables to take into consideration. Every refinance decision will have to be evaluated on its own merits with the anticipated hold period being the most important variable while also taking into consideration overall portfolio composition in terms of maturity dates and what percentage is fixed versus floating. In the past couple of years we have gone from approximately 80% floating to 60%. I would expect the floating percentage to continue to drop.

Between 2012 and 2021 the macro trumped the micro as going floating was so beneficial from an interest rate savings standpoint and prepayment flexibility. This enabled us to prepay 100 loans with $2.7 billion of principal value. The prepayment flexibility provided us with enormous benefits. Today, not so much for the reasons cited above. As a result, the micro is much more significant in our decision making process as it’s so difficult to feel firmly convicted about the macro outlook.

One subtle point: apartment fundamentals matter enormously here

If you have:

- strong NOI growth,

- constrained supply,

- and resilient occupancy,

then floating becomes more tolerable because inflation partially “hedges” the liability through rent growth.

But if you enter a lower-growth apartment environment with:

- elevated deliveries,

- slower rent growth,

- and higher concessions,

then floating becomes much more dangerous because your revenue loses inflation pass-through while your financing remains volatile.

That dynamic may matter more in 2027 than the exact SOFR level itself.

The good news is that our experience over the last two years has given us flexibility. By proactively refinancing 27 loans and fixing 23 of them when the risk-reward was favorable, we have substantially reduced our exposure to an uncertain interest-rate environment.

The next 22 loans will require a fresh analysis. The answer may not be the same as it was in 2024.

And that, perhaps, is the most important lesson of all: the best financing strategy is not a permanent preference for fixed or floating debt—it is the willingness to adapt when the economic landscape changes.

{kind=link}

Threading the needle takes skill and perseverance. And you will not always be correct when you decide.

My forecast is that we will continue to have to deal with inflation for the next couple of years. But the larger looming problem is the continued high level of growth of our national debt. Hopefully, there will be a broader recognition of the potential harm that will occur if we do not drastically reduce Government expenditures. We are currently headed toward a very steep cliff!

Perhaps, CWS should be mostly a seller rather than a buyer — and turnover the assets more rapidly. But, of course, there have to be willing buyers!

My bottom line is that it is unlikely to have the kind of low interest rates we enjoyed in the recent past.

Much of the recent inflation is the result of (a) excessive Government expenditures and (b) supply constraints. Neither of these two causes are effectively cured by high interest rates. Nevertheless, the Fed has ignored this and has continued to try to use interest rate increases to deal with the problem. Yes, there are other factors involved but I still think that Fed policies have been very narrowly and badly focused.