The financial narrative has evolved from a simple “cooling economy” story into a complex tug-of-war between recessionary signals and surprising pockets of resilience. While markets continue to price in future rate cuts, recent data highlights significant cross-currents that make the Federal Reserve’s path forward increasingly uncertain.

1. The Case for Easing: Softening Inflation and Housing Strain

The primary argument for lower rates remains the visible cooling in price pressures and specific interest-rate-sensitive sectors.

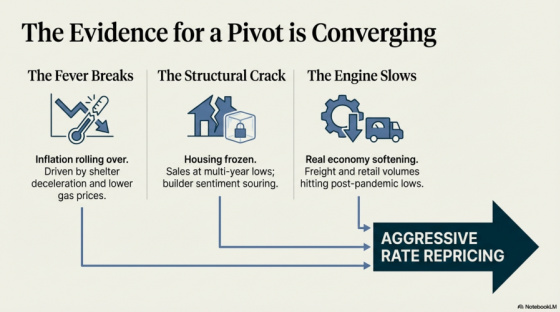

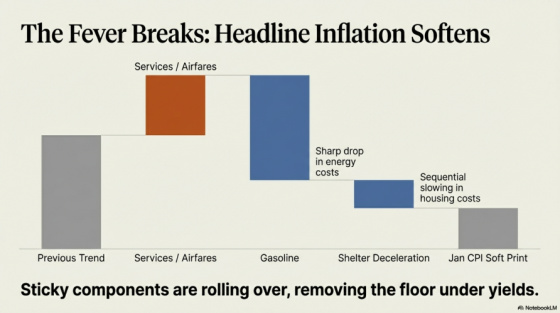

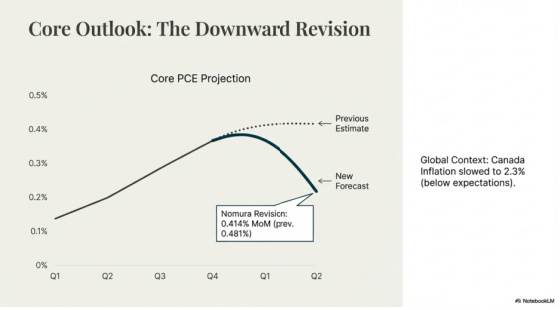

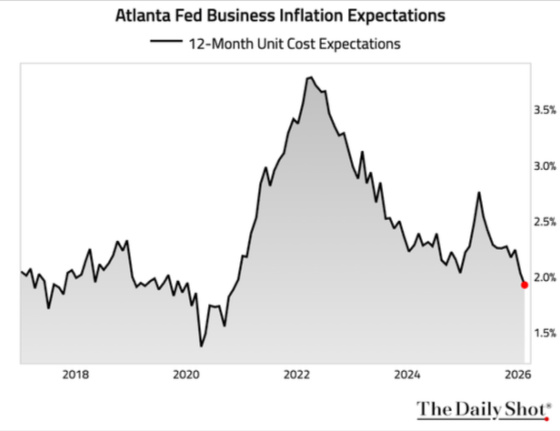

- Inflation Downshifts: January’s headline inflation was softer than expected, driven by a sharp drop in gasoline prices. In response, Nomura lowered its core PCE inflation estimate to 0.414% month-over-month. Rates markets reacted dovishly to these prints, pricing in more rate cuts for 2026 as Treasury yields declined across the curve.

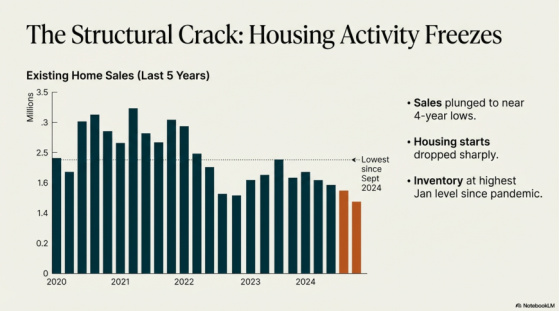

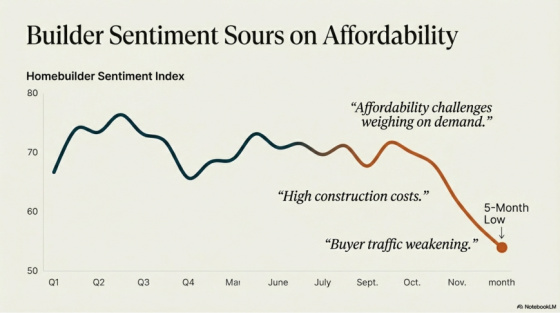

- Housing Market Pressure: Existing home sales recently experienced their largest plunge in nearly four years, hitting their lowest level since late 2024. Furthermore, homebuilder sentiment slipped to a five-month low as affordability challenges and high construction costs continue to weigh on demand.

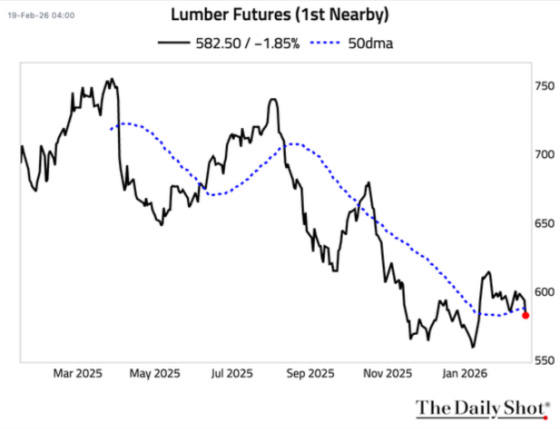

With weak housing demand due to affordability issues and a pessimistic outlook among homebuilders, lumber prices, a key input to home construction, have been dropping fairly consistently for the past year, and they look like they could test their most recent lows.

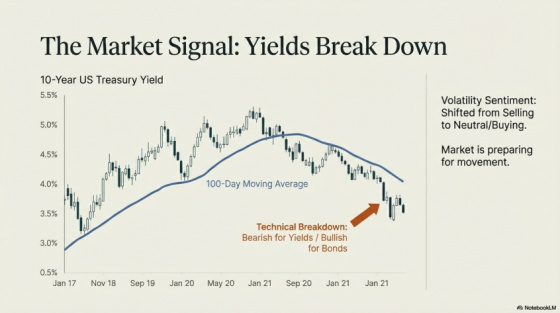

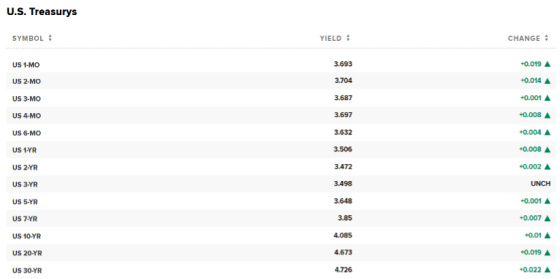

- Technical Breakdown in Yields: The bond market reflected this cooling, with the 2-year Treasury yield hitting its lowest level since September 2022 and the 10-year yield slipping back toward 4%.

• Weaker than expected GDP

For people who fret over the deficit, here is what happened to Treasury yields after the Supreme Court struck down Trump’s tariffs, creating the potential for having to fund $170 billion to importers, which would increase the deficit even more. Yields were essentially unchanged, suggesting that these potential refunds cause no concern for Treasury investors.

2. The Resilience Counter-Punch: Business Investment and Production

Countering the “slowdown” narrative is a series of robust data points suggesting the economic engine is still humming at a healthy clip.

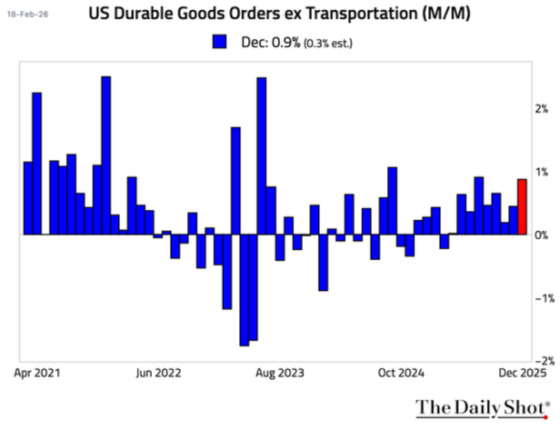

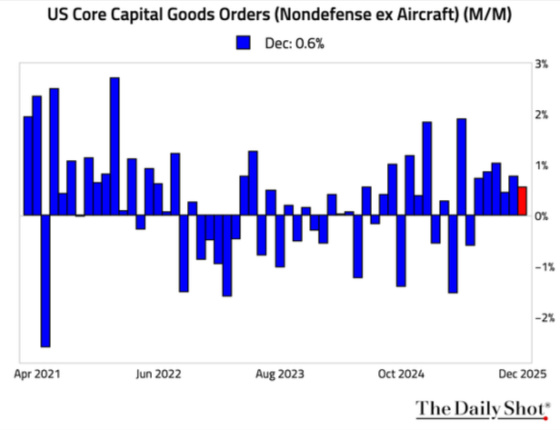

- Robust Business Investment: Core capital goods orders—a key proxy for business investment—rose by a robust 0.6%, signaling solid underlying momentum. Stripping out volatile aircraft, durable goods orders rose by a solid 0.9%, significantly beating consensus.

• While some retail estimates showed a slight dip, the Redbook index of same-store sales actually accelerated, indicating that consumer demand remains a wildcard.

3. Market Cross-Currents: Treasury Weakness and Sector Rotations

The “tug-of-war” is most visible in the recent volatility and conflicting signals within the rates and equity markets.

- Weak Treasury Demand: A recent $16 billion 20-year Treasury auction was notably weak, featuring a “large tail” and the lowest foreign demand since 2021. This forced dealers to absorb more supply, driving longer-dated yields higher even as shorter-term rates showed downward pressure.

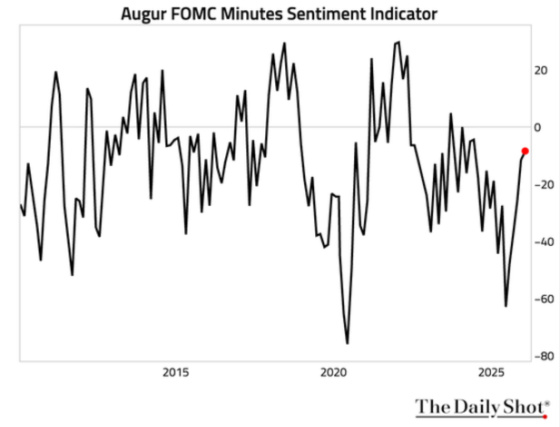

- The Fed’s Hesitation: January’s FOMC minutes were less dovish than some expected. While several participants signaled support for cuts if inflation declines, others favored holding rates longer, and some even noted that hikes could become appropriate if inflation remains above target.

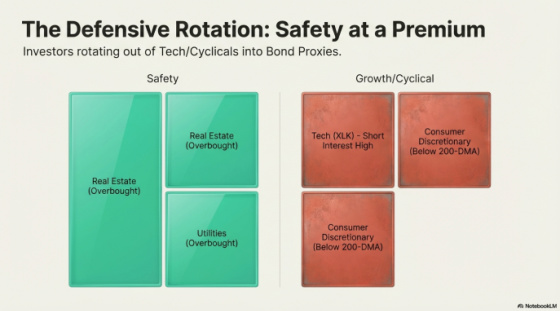

- Aggressive Sector Rotation: The equity market is reflecting these split views. While Real Estate and Utilities have entered overbought territory as investors bet on lower rates, the Technology sector recently led a selloff, with short interest in the XLK ETF hitting a decade high.

Conclusion

We are witnessing a market trying to price in a “soft landing” while simultaneously grappling with high business investment and a volatile Treasury market. As building permits show surprising near-term strength and same-store sales accelerate, the Fed is unlikely to rush into deep cuts until these conflicting cross-currents resolve.

{kind=link}

Leave a Reply