The two big events last week were the release of the non-farm payroll report and Heather and I attending the Oasis concert at the Rose Bowl. I will target discussing the latter next week while focusing on the former for this week’s blog. That said, I will weave in some Oasis songs to make the dry topics of employment data and interest rates a bit more interesting and entertaining.

I’m not sure who Trump is going to fire now that he got rid of the head of the Bureau of Labor Statistics after last month’s report, but this one, not surprisingly, was also very weak.

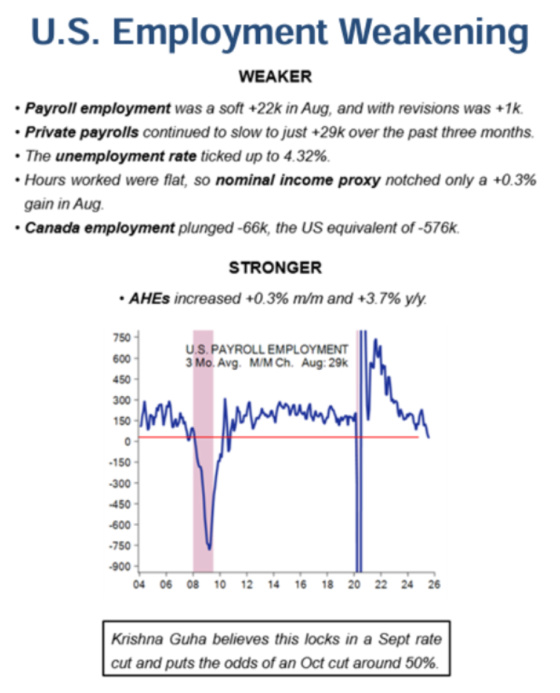

This chart from Evercore ISI shows the significant slowdown in employment and their belief that a September rate cut is locked in and a 50% chance of an October rate cut.

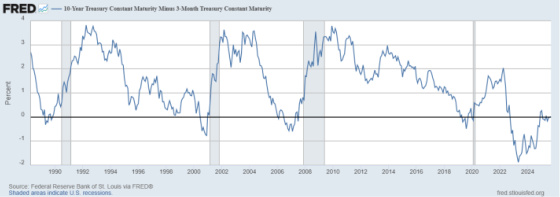

I have been saying for a while now that recession watches start not when the yield curve first inverts, which I had thought for a long time, but when the yield curve de-inverts, which it has now done. The 10-year yield is now 5 basis points higher than the 3-month T-bill yield so the curve has de-inverted after having been inverted since October 2022.

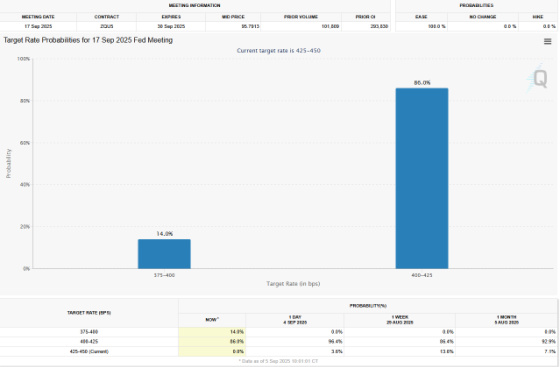

Looking at CME Fed rate cut probabilities one can see that prior to the jobs report the probability of the Fed cutting rates by 0.25% for the September 17th meeting was 96% and now it has dropped to 86%. The reason it has dropped is because now there’s a 14% chance that it cuts rates by 0.50%! Thus, there is now a 100% chance the Fed will cut rates at its next meeting.

I am now aligned with the market that the Fed will cut rates three times by the end of this year. Powell has clearly articulated that his eyes are squarely on the labor market and that weakness there will take precedence over inflation concerns from the tariffs. I just don’t see any data coming out in the next couple of months that will have the Fed pause with just one rate cut.

This is how an Oasis fan would frame the situation.

🎶 Don’t Look Back in Anger: Why the Fed Will Cut Rates Three Times

As the labor market softens and economic momentum wanes, the Federal Reserve faces a familiar crossroads. The September 2025 nonfarm payroll report revealed just 22,000 jobs added, a third consecutive decline. Unemployment ticked up to 4.0%, and wage growth slowed to a mere 0.1%—a trifecta that signals a cooling economy.

Much like Oasis’s anthem “Don’t Look Back in Anger,” the Fed must now look forward with resolve, not regret. The data is clear: the time for easing is now.

🎸 Slide Away from Tightening: The Labor Market Breakdown

| Indicator | July 2025 | August 2025 | September 2025 |

| Nonfarm Payrolls (Jobs) | -13,000 | 79,000 | 22,000 |

| Unemployment Rate (%) | 3.6 | 3.8 | 4.0 |

| Avg. Hourly Earnings (%) | 0.3 | 0.2 | 0.1 |

This table tells a story of retreat—of an economy that’s “Half the World Away” from the robust labor market of early 2025.

🧠 Live Forever? Not Without Stimulus

The Fed’s dual mandate—maximum employment and price stability—is under threat. With inflation cooling and employment weakening, the Fed must act. Market expectations are already aligned:

- A 25 bps cut is priced in for September.

- 125 bps of cuts expected by September 2026.

As Oasis sings in “Live Forever,” the dream of sustained growth needs nurturing. Rate cuts are the Fed’s way of keeping that dream alive.

🔮 Morning Glory for Markets: Why Three Cuts Are Coming

- September FOMC: A cut is nearly guaranteed.

- November FOMC: Continued softness will justify another.

- December FOMC: A third cut will stabilize growth heading into 2026.

This trilogy of easing mirrors the emotional arc of Oasis’s “Champagne Supernova”—a slow build, a peak, and a release.

🎤 Encore: Wonderwall of Support

Just as Oasis closes their set with “Wonderwall,” the Fed’s rate cuts will be the encore that markets have been waiting for. They won’t fix everything, but they’ll offer support—just like the song’s refrain:

“Maybe you’re gonna be the one that saves me.”

I look forward to reporting back next week on the Oasis concert which, admittedly, my most eagerly awaited concert for at least the last 10 years.

{kind=link}

Leave a Reply