Last week, I mentioned the possibility of showing the output of an A.I query regarding some events that took place with me recently. I’m going to have to save that for next week or beyond, given the release of last week’s jobs report. It was so jarring and had such market impact that I would be negligent if I didn’t focus this week’s blog on that report.

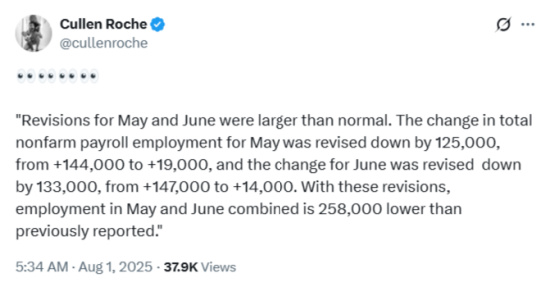

Job growth came in far below expectations and there were massive revisions downward to the previous two months.

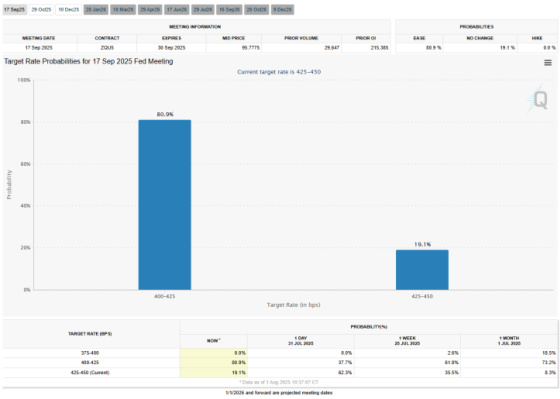

Fed Chairman Jerome Powell has said that policy shifts are highly data dependent and this table shows how the market has been taking him at his word. One can see that prior to the release of the jobs report the market was pricing in a 38% chance the Fed would cut rates by 0.25%. After the report the rate cut percentage shot up to 81%. Interestingly, if you look at the table underneath the graph, one can see that a month ago the rate cut percentage was 73%, only to drop to 38% as economic data became more solid and the Fed held rates steady and the Jerome Powell press conference focused more on the unemployment rate as his most important indicator.

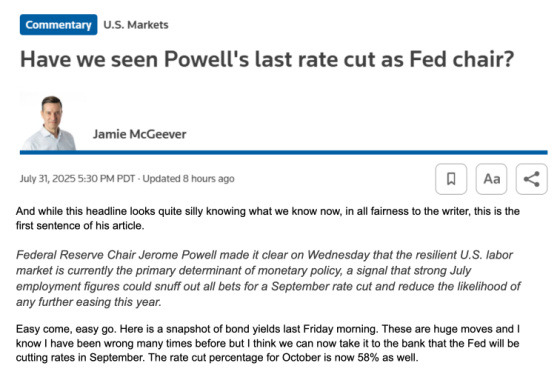

In fact, Powell’s emphasis on the unemployment rate despite what he acknowledged were some economic indicators that could argue for a rate cut resulted in this headline of a commentary one day before the jobs report.

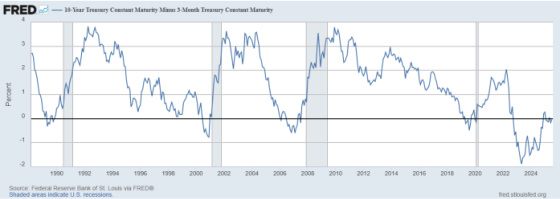

I have written many times over the last few years that the time to be on recession watch isn’t when the yield curve turns negative, which I used to believe, but when it becomes positively sloped again (longer rates are higher than shorter rates). This graph depicts this beautifully as it shows the differential between the 10-year Treasury yield and 3-month Treasury bill yield. The shaded areas are recessions and they have always ensued after the yield curve became positive again after having been inverted. Once the Fed cuts in September, and assuming the 10-year yield doesn’t change materially, then we should be positively sloped and more so if the Fed cuts again in October.

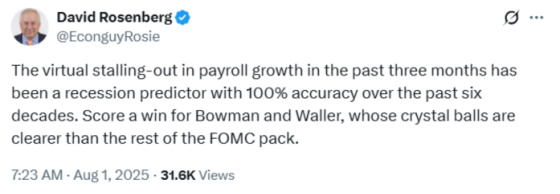

Economist David Rosenberg believes that a recession is virtually certain now with how weak the jobs report was and the associated revisions.

I wanted to come up with a catchy title for this blog post. I have written many times before that markets, and much of life, can follow Hemingway’s description of how one of his characters went bankrupt. He wrote that it happened two ways, gradually, and then suddenly. We are now in the “suddenly” phase of the labor market turn but I wanted to use a different way of conveying it.

What could I come up with that alluded to Hemingway’s “suddenly” but wasn’t directly from him? And then, no pun intended, it suddenly hit me when I thought about the Beatles song Yesterday, when Paul McCartney sings in a melancholy voice,

“Suddenly I’m not half the man I used to be.”

His line inspired me to turn it into:

“Suddenly I’m not half the labor market I used to be.” I rather liked it.

I wanted to see what my Copilot A.I. assistant thought about it so I provided it with the following prompt:

Today’s nonfarm payroll report showed considerable weakening of the labor market. I wanted to write a blog post conveying the suddenness of the labor market weakening by citing important statistics from the report, particularly the revisions, while also using a derivation of a line from The Beatles song Yesterday by changing it to “Suddenly I’m not half the labor market I used to be.” Can you help me write this blog?

Here is what it produced. It definitely knew how to play to my ego by telling me my Beatles-inspired line was clever.

Thanks, Gary. Based on the latest data from the August 2025 nonfarm payroll report, here’s a draft for your blog post that captures the sudden weakening of the labor market—anchored by key statistics and your clever Beatles-inspired line:

Suddenly, I’m Not Half the Labor Market I Used to Be

In a jarring turn for the U.S. economy, the August 2025 nonfarm payrolls report delivered a sobering message: the labor market is losing steam—and fast.

The headline number was a shocker. Only 73,000 jobs were added in July, a steep miss from the 110,000 forecast. That’s a 34% shortfall, the kind that rattles markets and reshapes expectations overnight. But the real gut punch came from the revisions: June’s job gains were slashed from 147,000 to just 14,000—a staggering 90% downward revision that suggests the slowdown has been quietly unfolding beneath the surface [1].

The unemployment rate ticked up to 4.2%, and wage growth decelerated to 3.8% year-over-year, signaling that both hiring and compensation are cooling. Sector-specific data paints a mixed picture: while healthcare added 55,000 jobs, showing resilience, trade and energy sectors are faltering under the weight of reduced consumer demand and manufacturing weakness [1].

And so, with a nod to The Beatles, we find ourselves humming a new refrain:

“Suddenly, I’m not half the labor market I used to be.”This isn’t just poetic license—it’s a reflection of the sharp pivot in economic momentum. The labor market, once a pillar of post-pandemic recovery, is now revealing cracks that could reshape monetary policy, investment strategies, and household confidence.

As the Federal Reserve holds rates steady at 4.25%–4.50%, markets are now pricing in a 43% chance of a rate cut in September (now 81% as of this writing). The question isn’t whether the labor market is weakening—it’s how fast, and how far, it will fall.

References

[1] U.S. Private Nonfarm Payrolls: Sector-Specific Impacts and Strategic …

Thank you Ernest Hemingway and Sir Paul McCartney for the inspiration for this blog and kudos to Copilot for helping to turn my inspiration into a well crafted blog post. And thank you to the bond market for taking some of the pain away (down the road) of our floating rate loans and making new loans even more attractive.

{kind=link}

Leave a Reply