Fed Chairman Jay Powell understandably garnered a lot of attention after the Fed meetings concluded last week, which resulted in the first pause in rate hikes after 10 consecutive increases. At the same time, to manage expectations, the Fed dot plot forecasts two more interest rate hikes before they’re done for this cycle. For me, however, the most interesting piece of news about Powell that came out last week is that it appears that he is a big fan of the Grateful Dead.

Jay Powell Deadhead

This is a picture of him at a Dead and Company show in Virginia that was posted on Twitter.

One thing I didn’t know until I read the article linked above is that Dead & Co.’s bass player, Oteil Burbridge, said that he got introduced to the Grateful Dead in high school when a friend of his, Monica Powell, gave him Grateful Dead records to listen to. It turns out that Monica is Jay’s younger sister, and she lent him Jay’s records. How cool is that?!

Jay Powell saw his first show in 1973, so he’s been a fan for a very long time.

If I had sat next to him at the concert, besides querying him about his Dead history, favorite shows, era, songs, etc., I would have also asked him why he is seemingly ignoring his favorite yield curve indicator, the Near Term Forward Spread. If he had, in turn, asked me if I had been smoking something to bring that up at a Dead & Co. show, I would have vehemently said no, but with how fast he has raised rates and hurt our cash flows, I probably should be doing just that.

Powell used this indicator to justify starting to raise rates in March 2022 when at the time, the differential between the 10-year Treasury yield and the 2-year had narrowed so much that it was nearly inverted, which is typically a precursor to an economic slowdown or recession. That is typically the time when you want to be raising rates, but he begged to differ.

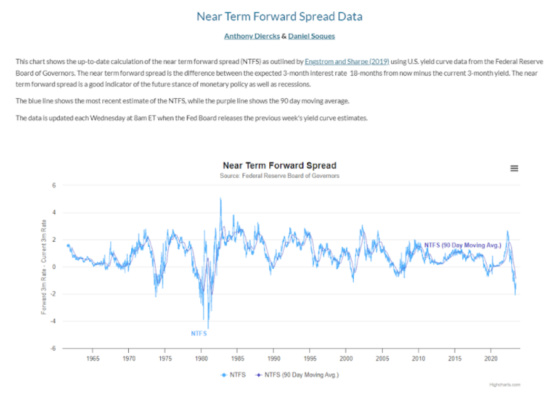

As I have written about before, Powell dismissed the information value of the 10 minus 2 spread and said Fed research showed there was a much better yield curve indicator which is the Near Term Forward Spread. The explanation of what it is is at the top of the following graph.

One can see that the spread has become more negative at any time in the last 40 years, which suggests the Fed is keeping interest rates too high and they should be lowered. I would love to know how Powell would respond to that. I’m sure he would have said the labor market is too strong, and inflation is still running too high to let his foot off of the brake. In addition, the federal deficit is also highly stimulative, which is requiring the Fed to be tighter than it otherwise would have to. Nevertheless, despite Powell’s justifications for ignoring it, this indicator suggests that the longer he keeps the brakes on the more aggressively he is going to have to switch it to hitting the gas by lowering rates.

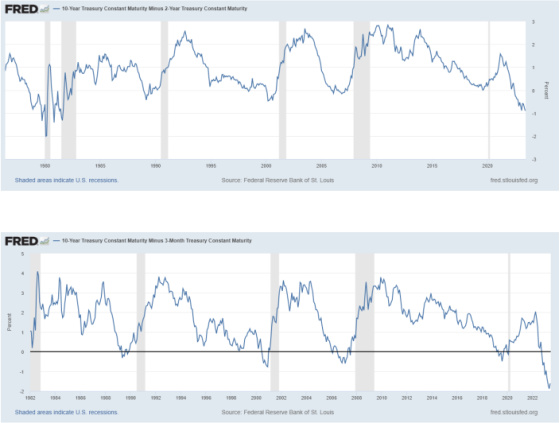

The yield curve, both the 10 minus the 2 and 10 minus 3-month T-Bill yields, are extremely inverted, with short rates being materially higher than long rates, as these next two graphs show.

Many economists and forecasters have understandably been calling for a recession, given the inverted yield curve. And while I have been in the camp that the Fed is engineering a big squeeze in the economy to slow it down and even risk inducing a recession, what is clear from the two previous graphs is that a recession doesn’t kick in until after the yield curve becomes positive again. The vertical gray bars are times of recession, and they don’t begin until the yield curve becomes positive. This either occurs by long rates going up to exceed short rates, which is highly unlikely, or short rates coming down below long rates, which is much more likely. Long rates can also come down, but short rates come down even further. Thus, for me, the most important recession indicator is when the yield curve becomes sustainably positive and increasingly so until it gets to at least 1%.

I’m not worried about long rates going up to a level that exceeds short rates because inflation is clearly coming down, and the Fed wants to slow the economy. In addition, short-term rates are now well above the rate of inflation, and the longer they stay there and inflation continues to come down, the more it will squeeze credit-sensitive areas of the economy and create more challenges for borrowers with floating rate loans and for those who have loans maturing in a much more difficult and conservative lending environment.

This chart shows the forecast for inflation-adjusted short-term rates even if the Fed doesn’t raise rates anymore. One can see that with inflation projected to fall. It’s going to put an even tighter squeeze on the credit-focused parts of the economy as real rates are projected to exceed 3% in less than one year. That is highly restrictive and painful.

This next chart shows that even with short-term rates projected to come down, they will still be at restrictive levels. Said differently, they will continue to exceed inflation estimates by a wide margin.

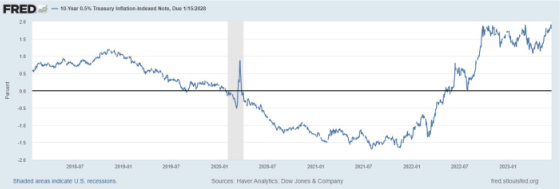

The real rate of interest as measured by 10-year Treasury Inflation-Protected Securities (TIPS) is at its highest levels in the past five years. It was about 1% pre-Covid and then went deeply negative during Covid, and now it is 1.78%. This premium is most likely due to the need to wash out some of the excesses that took place during the very loose monetary policy and credit conditions during those times, along with the extraordinary fiscal response and its lingering effects.

Higher rates and tighter monetary policy are starting to have the Fed’s desired effect of slowing the economy. Retail sales on a same-store basis are no longer growing, as this chart shows.

The outlook is also challenging as banks’ willingness to make consumer loans has dropped sharply to recessionary levels.

Finally, the labor market is starting to soften a bit as initial jobless claims are now clearly at levels that are higher than the average for 2018, 2019, and 2022. 2020 and 2021 are excluded due to the Covid distortions.

Throw in the resumption of student loan payments in August, which will undoubtedly impact consumer spending, and we should presumably have an additional headwind for employment growth, although it may take some time to feel the full effect. Approximately 45 million people have benefited from not having had to pay interest and principal on their student loans since Covid. According to Speaker of the House Kevin McCarthy, it has cost the federal government $5 billion per month in revenue. These are dollars that will now have to be redirected from spending and savings to the federal government, which is akin to a tax.

To conclude, I’m glad to see that Jay Powell is a Grateful Dead fan. I’m also concerned that his approach of going Dead ahead with the Fed’s highly restrictive policy in the face of much more difficult credit conditions and slowing retail sales, and a starting to soften labor market, albeit somewhat mitigated by large fiscal deficits, will create a fire that will spread and cause a fair amount of damage. One of the Dead’s most beloved songs is Fire on the Mountain. If you read the lyrics carefully, I think they convey some of the concerns I have about Powell’s Dead Ahead approach to squeezing the economy.

Long distance runner, what you standin’ there for?

Get up, get out, get out of the door

You’re playin’ cold music on the barroom floor

Drowned in your laughter and dead to the core

There’s a dragon with matches that’s loose on the town

Takes a whole pail of water just to cool him down

Fire! Fire on the mountain

Fire! Fire on the mountain

Fire! Fire on the mountain

Fire! Fire on the mountain

Almost ablaze, still you don’t feel the heat

It takes all you got just to stay on the beat

You say it’s a livin’, we all gotta eat

But you’re here alone, there’s no one to compete

If Mercy’s a business, I wish it for you

More than just ashes when your dreams come true

Fire! Fire on the mountain

Fire! Fire on the mountain

Fire! Fire on the mountain

Fire! Fire on the mountain

Long distance runner, what you holdin’ out for?

Caught in slow motion in a dash for the door

The flame from your stage has now spread to the floor

You gave all you had, why you wanna give more?

The more that you give, the more it will take

To the thin line beyond, which you really can’t fake

Fire! Fire on the mountain

Fire! Fire on the mountain

Fire! Fire on the mountain

Fire! Fire on the mountain

{kind=link}

Leave a Reply