With over $6 trillion in global stock market losses in one week, it’s clear that investors have woken up to the real risk that the coronavirus is not contained, somewhat akin to the subprime crisis that Ben Bernanke famously said was and led to massive financial losses around the world.

COVID-19 Coronavirus Catch-22

I wrote last week about the disconnect between record-high stock prices and declining Treasury yields. There was really no way to reconcile the two. One of them had to reverse and it was the stock market that cracked as the following chart shows of the S&P 500 SPDR ETF dropping precipitously.

At the same time, the 10-year Treasury yield hit a record low last week.

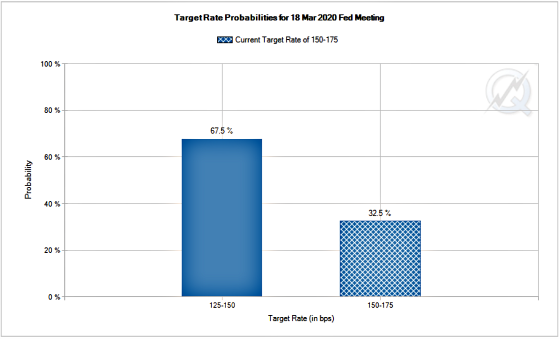

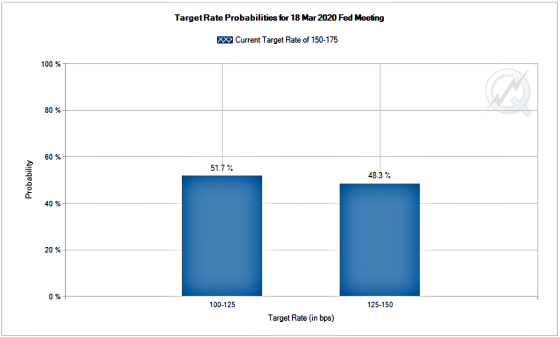

With the dramatic drop in interest rates and the evaporation of so much stock market wealth in such a short period of time, the odds are now 100% that the Fed will cut by 25 basis points and nearly 52% they will cut by 50 basis points!!

LIBOR

LIBOR is often about 10 basis points wider than the Federal Funds rate, so this would be very beneficial for floating-rate borrowers whose loans are tied to LIBOR, as are most of our loans at CWS. Our budgets for 2020 assume that LIBOR would hold at 1.75% throughout the year and it looks like that will turn out to be a conservative projection. LIBOR on a 30-day basis is approximately 1.58% and there’s been a noticeable drop in the 12-month LIBOR foreshadowing future lower rates as the following table shows. This can be seen in the last row with that rate dropping by approximately 22 basis points from the previous week.

This should provide a tailwind for us in terms of cash flow and offer a bit of a hedge if the economy slows and spills over to weakening demand for apartments and less pricing power for owners. This hedge is not available to those who chose to finance with fixed-rate loans as their debt service costs obviously remain unchanged from an interest rate perspective.

Projected Inflation

With rates being where they are and inflation staying relatively low, there was an important speech last week by Federal Reserve Governor Lael Brainard entitled Monetary Policy Strategies and Tools When Inflation and Interest Rates Are Low. She discussed some lessons learned from previous downturns and what the Federal Reserve may do when faced with undershooting inflation and a deteriorating economic environment with slack in the labor market. Her research concluded that during the Great Recession they didn’t move fast enough implementing unconventional policies primarily because they were untested and there were fears that the ramifications of those policies may have negative consequences. These fears turned out to be misguided and led the Fed and other central banks to be more cautious in their implementation than they should have been.

Federal Reserve Governor Lael Brainard

As there are real prospects for a slowdown with the coronavirus I don’t see how we’re not going to be impacted by it in the United States. Given how China has virtually shut down its economy this is already rippling through to tourism via airlines and cruise lines not going to China and other parts of Asia as well as the virus spreading to Italy which will negatively impact tourism there as well. In addition, with virtually no Chinese travelers due to countries not letting them in or their inability to get out, major tourist destinations like Los Angeles and New York City could also be significantly impacted.

Supply chains are already being impacted and have led to companies like Apple and Microsoft either lowering financial guidance or removing it altogether. All of this is happening even before any impact from more cases showing up in the United States.

With California now experiencing its own issues related to the Coronavirus, I may be safer where I’m going. Wish me luck!

{kind=link}

Stay safe in your travels … and look forward to your observations