I love the word enantiodromia. Maybe it’s because of how esoteric it is or how intelligent it makes me seem (even though I can barely pronounce it). I think the real reason I like it is that it captures a very powerful tendency in people and in cycles for people and nature to shift to their opposites. Think of reformed smokers, people who have overcome their addictions, and those that have experienced religious awakenings, or political changes, just to name a few. They can become the biggest zealots against what they previously believed or the behaviors they displayed. The conversion that Paul went through on the road to Damascus is another example of enantiodromia.

“What the wise do at the beginning, fools do in the end.” ~ Warren BuffettClick To TweetIn the investment arena it can be conveyed by the expression of Warren Buffett who has said that “What the wise do at the beginning, fools do in the end.” Oftentimes wise investors will invest in companies and industries that are out of favor, performed poorly in the rearview mirror, and most would have no interest in investing in because they don’t see any kind of bright future on the horizon. It’s just this pessimism that leads independent thinkers to look at such opportunities with fresh eyes to see if the market’s judgment is overly harsh and assigning too low of a value to these firms relative to their futures, even if they are modest.

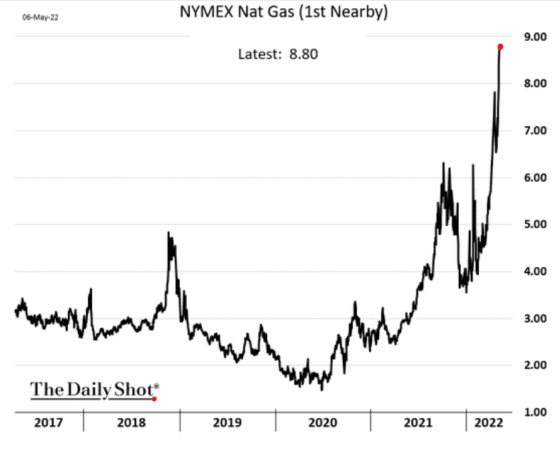

I wrote about this previously with regard to coal companies. It’s one of the most hated industries and it was decimated by a collapse in demand from Covid and huge pressures for utilities to move away from coal as a major input for their energy output. This led to capacity being reduced resulting from mines closing and companies unwilling to invest in growing their output potential and workers being laid off and people leaving the industry.

Eventually, however, the share price of these companies dropped so much that they were trading at very discounted values relative to the value of their assets. If there were any type of recovery, the pricing power they would have could be very strong. To the wise investors, the rewards far outweighed the risks and they have been proven right, especially over the last year as the recovery from Covid has been quite strong and the demand for coal has skyrocketed as natural gas prices have exploded. This has been compounded by many countries shunning Russian gas, oil, and coal in a very tight supply world for these commodities.

The fool part has to do with easily influenceable investors who react to headlines and a torrent of good news that would seem to convey that the good times will last forever and that these investments are sure winners, regardless of their valuation. The smart money exits by selling to the dumb money.

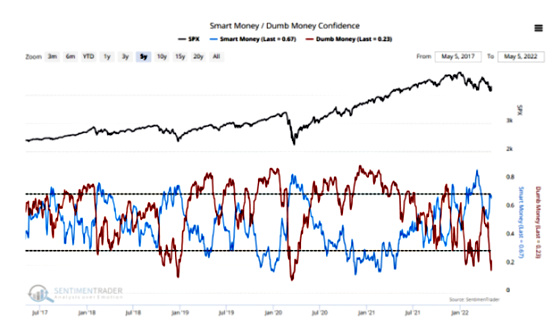

I subscribe to Sentimentrader.com and they believe in this dichotomy so much that they have created a Smart Money/Dumb Money Confidence indicator.

Right now it shows that the smart money is far more confident than the dumb money. This has historically turned out to be bullish for stocks.

Here is a longer-term chart showing how it appears to be a pretty good indicator of future performance (positive and negative) when there is an extreme divergence.

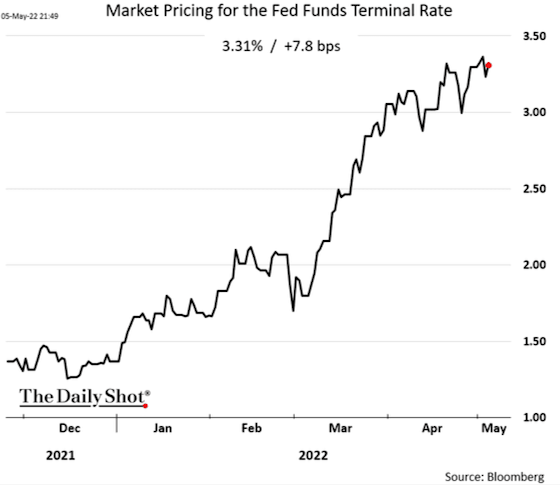

I bring this up because my sense is that Fed Chairman Jerome Powell has gone through his own conversion from being very accommodating and worried about the labor market and undershooting inflation to “Damn the torpedoes” and we’re going to do whatever it takes to break the back of inflation, like Paul Volker, and he doesn’t care if he takes the investor class down with the ship or causes a recession.

The following chart shows the annual percentage change in the Fed’s favorite inflation gauge, Personal Consumption Expenditures Excluding Food and Energy (Core PCE).

One can see how it shot up between 1973 and 1975 and came down after a recession ensued but to a still very high level. It then stayed elevated and shot up again through 1981 and then came down after another recession was brought about after interest rates went through the roof. From that point forward, until Covid, it was on a slow and steady decline such that it rarely exceeded 2% from 1998 through 2020. Interest rates came down accordingly. The following chart shows the trajectory of the Federal Funds Rate and one can see how it has had lower highs and lower lows between 2000 and 2021. This is not surprising given that it has correlated closely with the path of inflation.

The point of all of this is that up until recently the Fed was far more concerned about very low inflation or even deflation than it was about inflation since it could rarely achieve its 2% objective. Thus, when looking in the rearview mirror one can see why the Fed remained very accommodating for as long as it did. History would suggest that given all of the forces in the economy with aging industrialized societies, the financialization of our economy, large debt balances, globalization, and technological innovation, that inflation would be transitory. Based on GDP trends in the following table, it’s hard to argue with the prism through which the Fed saw the world pre-Covid.

Unfortunately what was in front of the car were very different conditions than the road that was taken to get to this point. Covid shifted demand from services to goods, supply chains became snarled due to Covid restrictions, especially in China, there was unprecedented fiscal support, the growth in the Fed’s balance sheet relative to GDP was huge, and tremendous numbers of people dropped out of the workforce to retire early or take time off to take care of children or enjoy government benefits, and remote work led to a huge increase in the demand for housing. All of these created a situation in which the demand for goods, labor, and housing and related services have exceeded the supply. This has led to pricing pressures we haven’t seen in over 40 years.

My sense is that Powell is now akin to a reformed smoker and he now despises being associated with inflation or being perceived as an enabler of it and he will do all in his power to break the back of it even if so much of it is out of his controlClick To TweetMy sense is that Powell is now akin to a reformed smoker and he now despises being associated with inflation or being perceived as an enabler of it and he will do all in his power to break the back of it even if so much of it is out of his control, like supply chain issues. The only way he can take care of that is by eviscerating demand by increasing real interest rates and I don’t think he has an issue doing that. The following chart shows how he has already made progress in this area with long-term, inflation-adjusted yields now being positive again.

I really believe that deep down Powell and other Fed members still believe they are most powerless against the forces of disinflation and deflation, especially if they have no intention of bringing rates below 0%. What they want to show is that they do have the answer for inflation and they want to prove that this can be handled bluntly and then get the economy back to a more equilibrium growth rate at a very stable level of inflation in the 2% range.

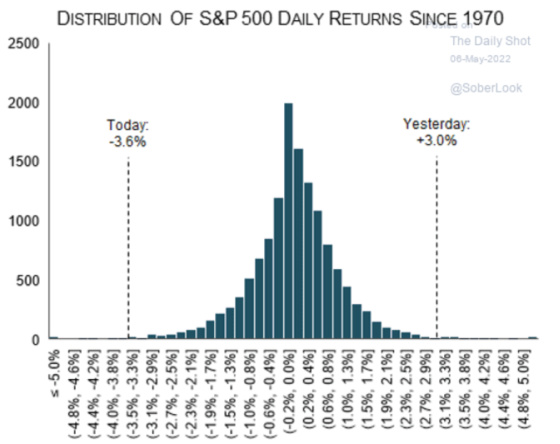

The Fed raised rates by 0.50% last week and the stock market shot up in relief that Powell took future 0.75% increases off of the table. My guess is that upset Powell because the last thing he wants to see is that the investor class thinks it can rely on him to return to an accommodating monetary policy at the first sign of weakness. The next day the market got absolutely crushed as I think investors came to conclude that the Fed is not going to be the friend of investors without a lot more pain. So why expose oneself to risky assets when that’s the last thing the Fed wants to have happen? One can see how rare the market moves were last Wednesday and Thursday.

The NASDAQ got absolutely crushed.

I don’t see how Powell engineers a soft landing without reversing course sooner than he would like. Housing is already feeling the impact of higher mortgage rates. This chart is an interesting comparison in that it shows the stock price change between a traditional homebuilder like Lennar and fintech housing companies like Zillow and Redfin. Lennar, in spite of having a price-earnings ratio of approximately 5, has still dropped by approximately 27%. Zillow and Redfin, however, not only have housing market headwinds to contend with due to higher mortgage rates and historically low supply of homes for sale, but they are also getting subsumed by the vicious selling of high P/E, low profitability tech-oriented companies as well. Zillow is down about 66% over the last year while Redfin has lost 78% of its value.

And speaking of high-flying tech companies, how about Netflix? It’s down about 75% from its peak. There is no way that it won’t tighten its belt and slow down spending for content and lower its headcount. That will presumably be the case for other companies that have lost a lot of value. This will have an impact on the demand for labor and be a headwind to consumer spending.

Amazon released its earnings and the market did not like what it heard regarding its outlook. The stock is down approximately 31% over the last six weeks or so. Facebook is down 46% from its peak. My sense is that companies whose stock prices have been hit hard will show more spending restraint. And let’s not forget that this is happening after the Fed has only raised rates by about 25% of where the market expects it to end up.

This is a chart that would probably please Jerome Powell. It shows how investors have been experiencing material losses in funds that purchase high yield debt. Clearly, investors want less exposure to riskier companies who are more leveraged and have less margin of safety in an environment in which the Fed is raising rates and will embark upon shrinking its balance sheet. This will tighten access to credit and be another headwind for the economy.

I feel very strongly that the Fed is tightening into a slowing economy. Let’s not forget that the last GDP report showed a slight contraction.

Returning to housing, look at how traffic has fallen off of a cliff for home improvement retailers.

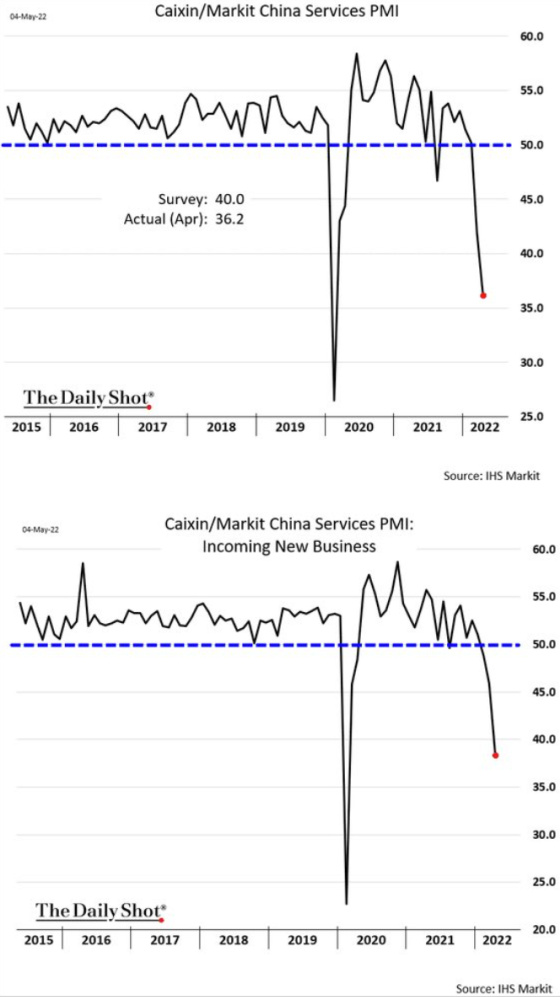

And what is happening in China, the world’s second-largest economy, is pretty dreadful economically. It’s zero Covid policy is wreaking havoc on the economy and global supply chains. Throw in the very weak real estate market and the government crackdown on large tech companies, and you have a very poor business climate and set of conditions, particularly in the service sector as these two charts show.

And one can see that in Hong Kong retail sales are extremely weak. They are on par with the depths of Covid.

Powell has shown great flexibility as evidenced by stating in late 2018 that interest rates were far from neutral and they had a lot further to go higher to shifting shortly thereafter to cutting rates as the economy showed signs that financial conditions were too tight and the economy could slow materially. He has now done the opposite and turned very hawkish. I think he will break something in the economy but he’s ok with that. He’s contending with a lot of rage against the machine, the financial/investor machine that is.

{kind=link}

My old boss Wolf Vedder would say, “If you want to make money, turn right when everyone else is turning left.”

Enantiodromia!