I was going to do a bit of a travelogue from my trip to London but one vital lesson I have come to learn in life is the importance and power of commitments. When one makes a commitment then it often requires preparation to honor that commitment. I like to use this blog for multiple purposes and one of them is to help me organize my thoughts and my thinking, particularly regarding the economy, interest rates, the apartment business, and other important factors that influence what I do at CWS. When raising money from investors we are naturally obligated to report on their investments and keep them informed. The blog helps me prepare for such reporting requirements and interactions.

Last week we had our semi-annual investor call. This of course necessitated being prepared to present to our investors our strategic thoughts, key initiatives, and results to better inform them as to how their investments are doing and what might be on the horizon. Knowing I had my weekly blog commitment I thought I would kill two birds with one stone by using this platform to prepare for last week’s call. As a result, I will use this week to convey some of the key points of what was communicated during our call.

CWS Semi-Annual Investor Call

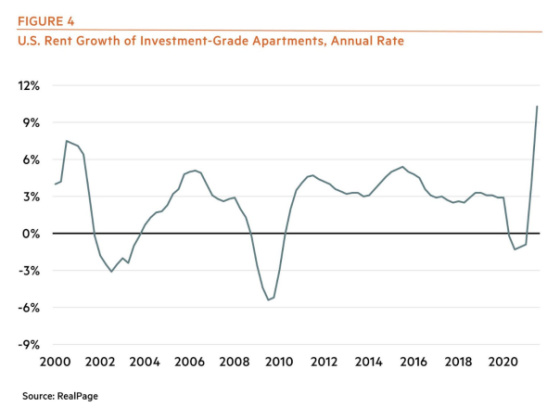

In my 34 years at CWS, I have never seen such significant rent increases as we are experiencing today. What is happening in our portfolio is quite remarkable, and we are by no means unique. The demand for apartments is on fire. Over the last year, over 600,000 units have been absorbed. This is by far a record amount during the 16+ years of data covered by RealPage and I would venture to guess it’s probably the highest since the 1970s.

With demand far exceeding supply, rents have spiked.

The unleashing of people migrating to different locations, particularly those that are business-friendly, have a lower cost, and good quality of life is creating significant demand pressures for apartments. At the same time, single-family homeownership is becoming a little harder to come by as the competition for homes is fierce with low mortgage rates, Covid fever inspired people to want more space while inflationary pressures have created more demand for tangible assets, and a large pool of investors buying homes to rent has propelled the demand for homes.

Homes listed for sale are selling almost as soon as they hit the market.

Construction delays and supply chain issues are also resulting in a large number of homes that have received permits for their construction but have not started yet.

All of these factors are serving to keep people renting longer. This has led to the tremendous growth in rents we are experiencing throughout the apartment industry.

The combination of increasing Net Operating Income with the tremendous amount of capital that has been accumulated to buy apartments has led to an explosion in values. Apartments have proven themselves to be quite resilient during Covid so investors like the stability of the asset class and the yield it offers in this low-interest rate world. In addition, the future looks bright given compelling demand fundamentals as a result of favorable demographics.

At CWS we are both buying and selling in this market.Click To TweetAt CWS we are both buying and selling in this market. In years past, we were primarily buyers while now it is much more balanced for us at this point. We are generally looking to trade out of older assets and exchange into newer ones with less ongoing capital maintenance requirements.

Like everyone, we are faced with labor challenges as we are trying to fill open positions and contend with employee turnover. It is particularly challenging finding maintenance technicians, but we are working aggressively at doing so. While we are making some headway, it is very much 1.25 steps forward and one backward.

During much of the year, we have been contending with the impact the Texas freeze had on many of our properties in Texas. Approximately 2,400 of our units had some form of damage and managing the repair and restoration of these has been a major challenge. Fortunately, the vast majority are now back online.

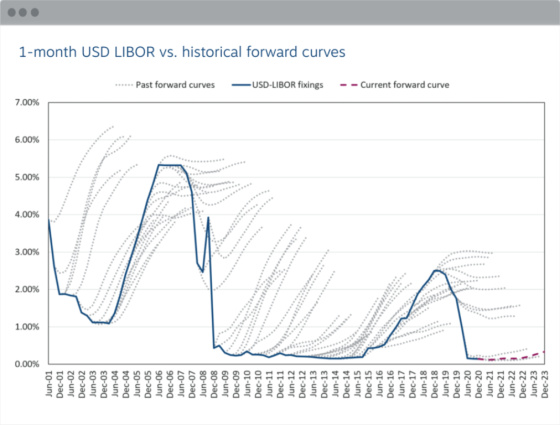

Our variable rate strategy allowed us to weather the storm of the pandemic quite effectively. Our same-store cash flow through October 2021 compared to 2020 grew by nearly 16%, of which approximately 90% of this came from interest savings due to us benefitting from 30-day Libor dropping in conjunction with the Federal Reserve lowering short-term rates. This has allowed us to increase distributions while also reinvesting in our properties and keeping them in good working order. We have reinvested over $33 million into our communities during the first 10 months of 2021, which is up from $29 million in 2020.

With 30-day Libor less than 0.10% and the spreads on many of our loans being lower than current market spreads, there is not much more benefit we will be able to get over the next year from our floating rate loans as we do not expect rates to drop or our spreads to compress via refinances. Fortunately, we are now in a position where the next phase of cash flow improvement can come from improved operating performance via higher rents. As discussed earlier, we are experiencing unprecedented rent growth in our portfolio. New renters in October signed leases at our apartments that on average exceeded what the previous resident was paying by close to 20%. This should allow us to continue to provide our investors with growing dividends (on a portfolio basis) for 2022.

Because of our reliance on variable rate loans, the question is whether we will give back much of our gains via materially higher interest rates in the future. Our budgets for 2022 assume that 30-day Libor will average 75 basis points which are conservative based on the forward curve which is projected to average closer to 50 basis points. Not surprisingly, there is a lot of talk that the Fed is behind the ball with inflationary pressures exploding throughout the economy exacerbated by supply chain problems.

These charts show how inflationary pressures have returned with a vengeance as the vast majority of firms in this survey are paying higher prices.

Labor costs are going up as well.

Chairman Powell is still more dovish in his statements relative to what the market believes the Fed will do. This chart shows how the market has typically overestimated future short-term rates in that the Fed has ended up being less aggressive than the market has priced in.

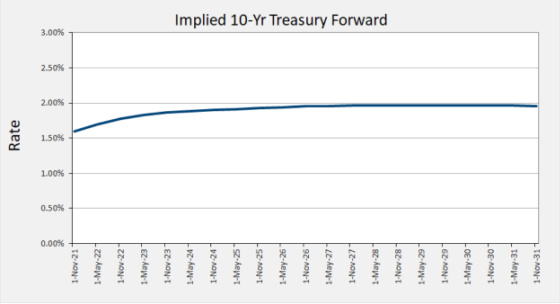

Last week’s forward curve pegged 30-day Libor in 10 years at approximately 1.85%. This is a good segue to future inflation. If the market believed future inflation were to remain elevated at today’s levels or higher than one would think, then the market would be pricing in higher short-term rates. This is clearly not the case, nor is it the case for longer-term, 10-year Treasury yields projected into the future as this chart shows.

Source: Chatham Financial

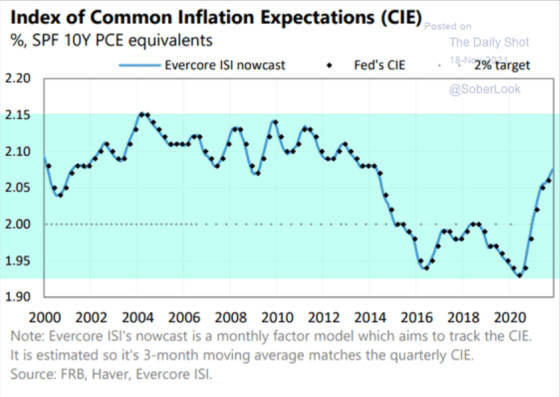

The following chart also shows how investors are not pricing in materially higher inflation in the future. Although elevated from the 2020 lows, the current levels are within the historical range. This series is a measure of expected inflation (on average) over the five-year period that begins five years from today.

Forecasts of future inflation remain anchored at lower historical levels, also suggesting that the current inflationary challenges are more short-term in nature.

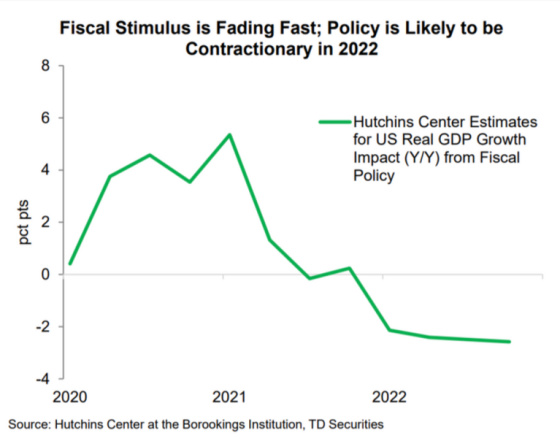

If government stimulus was a large contributor to the inflationary pressures present today then if this were to be reversed, perhaps inflationary pressures would subside. The following chart shows how federal spending will go from a GDP growth contributor to a detractor.

Finally, this chart shows the duration risk of corporate bond investors. The higher the value the more exposed they are to their bonds losing value as interest rates rise. Right now they have never been more negatively positioned to weather higher rates. This, in and of itself, can be a powerful brake on how high the Fed can push rates as it risks creating material financial losses which would lead to tightening credit that would negatively impact the economy.

In summary, our apartment portfolio held up well during Covid and our variable rate loan strategy paid off by lowering our interest costs and increasing our cash flow. We are now seeing the baton being passed from cash flow growth coming mostly from lower rates to it being generated through improved operational results. We continue to believe:

- We are In the right business

- We are In the right locations

- We have the right assets

- With the right customers

- With the right investors

- With the right financing

- With the right capabilities

{kind=link}

ThankYou for your clarifying and positive insights into an economic position given investment venues. You are appreciated.

All the best for a terrifically warm Thanksgiving for you and all of your loved ones.

Great Gary! Congrats.