For, you see, so many out-of-the-way things had happened lately that Alice had begun to think that very few things indeed were really impossible.

—Chapter 1, Down the Rabbit Hole

The impact of higher mortgage rates has definitely thrown a wrench into the typical cause-and-effect relationship between rates and home prices. One would have expected that the following chart, which shows mortgage rates more than doubling, would have had a profoundly negative impact on home prices.

And yet, as the following headline shows, this was not the case but actually has led to record home prices due to the “lock in” effect.

Because so many homeowners locked in much lower mortgage rates for long periods of time, and most people who sell their homes end up purchasing another one, they either will not or cannot sell their homes because they don’t want to see their monthly payments skyrocket. The key bullet point in the graphic above is that mortgage payments are up by 50% compared to one year ago. If you’re looking to buy a more expensive home using financing that is at a rate more than twice what you’re currently paying, you’re either going to rule it out entirely or think very long and hard about doing so.

In spite of lower demand due to much higher mortgage rates, the supply of homes available for sale is still less, such that the average home price has been hitting record highs. Of course, all real estate is local, so this doesn’t apply to every market, but the trend has been one of still more demand than supply and increasing home prices. On top of the tremendous increase in mortgage payments, throw in much higher insurance premiums, a shortage of contractors, and elevated property taxes, detailed oriented buyers who run the numbers will find that it is much more expensive to leave renting for ownership and that it is better to stay in place and enjoy the low interest rate one procured during the Covid era versus buying a new home or resale. The one lever with the former, however, is that homebuilders can buy down the interest rate for purchasers of their new homes, which is not something existing home sellers can do.

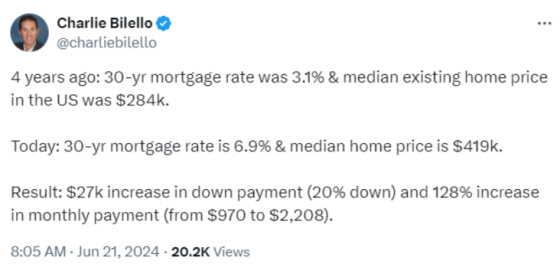

I think this tweet is a good summary of the magnitude of the change in monthly payments.

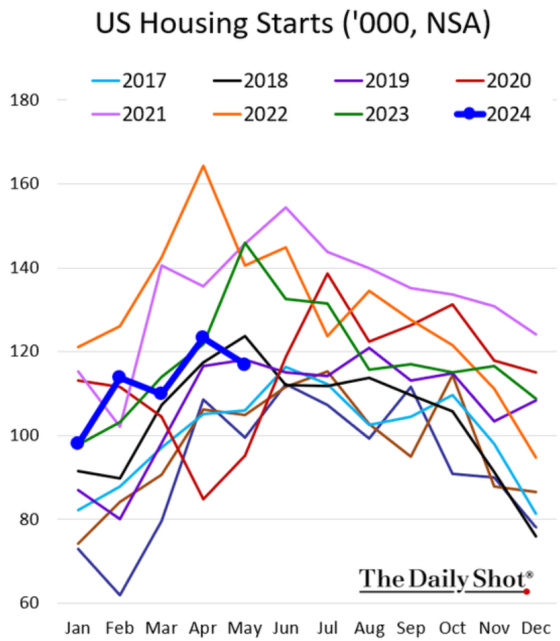

Given that home prices are at record levels one would expect that builders would be highly incentivized to create new homes to help alleviate the supply and demand imbalance. This is not the case, however, as higher borrowing rates, construction costs, and a dearth of lots, combined with an underlying concern about demand at these price levels has put a damper on new home construction.

One can see that housing starts are down approximately 20% year over year.

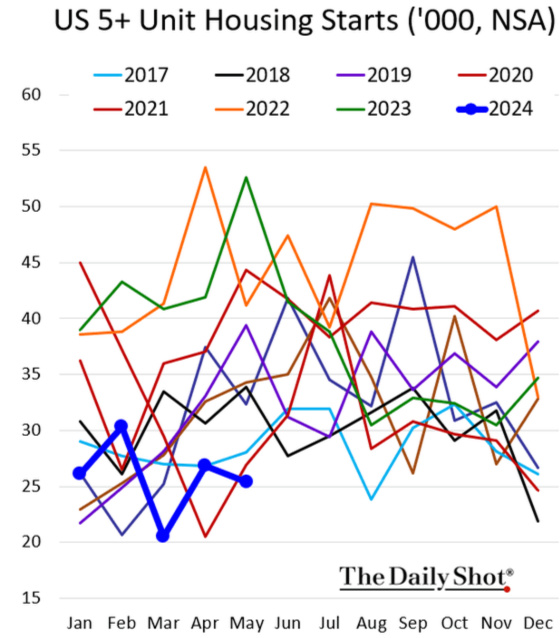

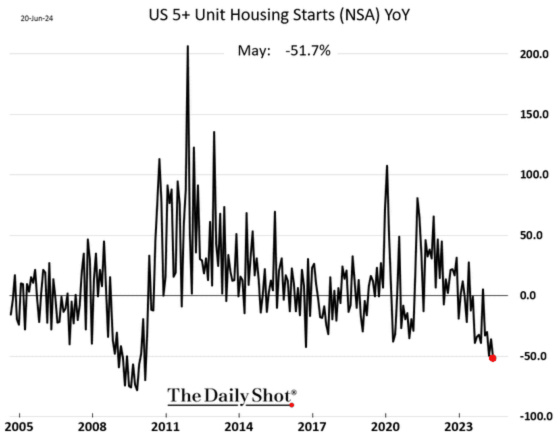

When we turn to multifamily starts, the situation is far more extreme in terms of the contraction of new supply. Starts are down approximately 50%, and, quite frankly, we are not surprised by this.

The combination of meager borrowing costs and rents spiking during Covid as the supply of units under construction coming to market was delayed because of labor and supply chain issues, along with more demand for space due to many more people working from home, led to an acute supply and demand imbalance. This chart shows how rents spiked significantly.

This created very profitable opportunities for developers to create new rental units. This has led to the highest number of multifamily units under construction since the mid-1970s. Although demand has come in much higher than projected, proving that supply can stimulate demand, this has been catalyzed by move-in incentives which has led to a significant deceleration in rent growth.

Developers have used free rent and gift cards to entice people to move in to fill up their communities as developers are under a great deal of financial pressure. When most of these projects were started interest rates were a lot lower. With rates having gone up so much in such a short period of time, however, this has led to interest costs being much higher than originally projected. In addition, most projects have taken longer to complete and have experienced cost overruns at a time when competition has only gotten more fierce such that the revenues being generated are quite a bit less than originally projected.

And if all of these factors weren’t challenging enough let’s throw in that apartment values are down approximately 27% according to Green Street. This has led to even more financial pressure because when construction loans come due in many cases developers will have to come in with additional cash to repay them since the combination of higher rates, lower values, and current underwriting standards make it difficult to generate enough new loan proceeds to fully repay maturing construction loans.

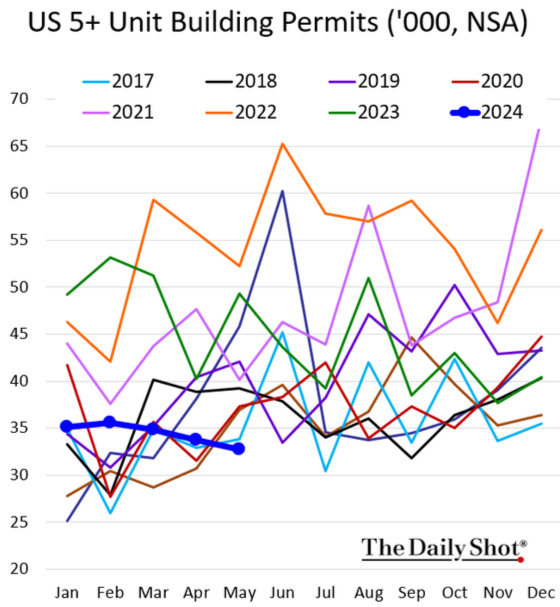

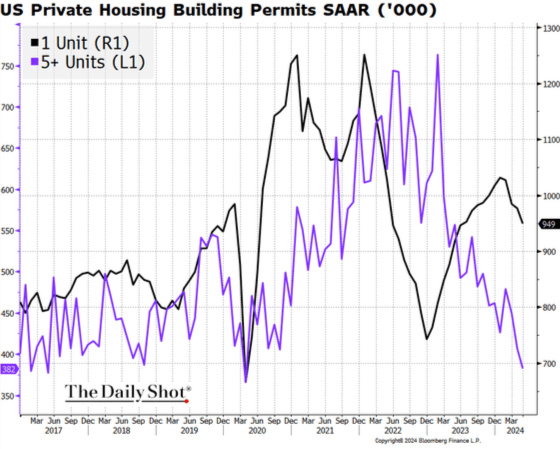

When combining all of these factors, capital access for developers to start new multifamily projects has become virtually non-existent. Lenders don’t have much of an appetite to add to their book of business and equity capital can find better returns purchasing existing assets from sellers under financial pressure and at prices meaningfully below the cost to build new. As a result, one can see that building permits for new multifamily projects have dropped significantly.

One can see how multifamily permits have dropped far more than single family permits and are now back down to the lower end of the range that was in place prior to the Covid boom. We think that this supply contraction will continue at least through the end of 2024.

Putting all of this together suggests to me that apartment owners are well positioned to regain pricing power once the excess supply is absorbed which we think should occur towards the end of 2025 or early 2026. If one can get through 2025 with few loans maturing then those hanging in there through these more challenging times should start to be rewarded with stronger operating income growth and value increases. Those with financial and emotional staying power, capital access, and a deep operations-focused platform, should be well positioned to prosper when the cycle is expected to turn after 2025.

I started this post by citing a passage from Alice in Wonderland. I’ll end it with one of Alice’s most famous lines to summarize the housing market.

“Curiouser and Curiouser!”

{kind=link}

A good summary.

Let’s hope that the Fed will act more wisely and let interest rates decline. It appears to me that the Fed attempts to cure inflation with these excessive interest rates have had is the impact on housing.

And then, we also need to stop our federal and state governments to stop the excessive spending spree they have been on. Excessive spending induces inflation.

Great article/forecast. I always enjoy reading your thoughts 😉 CWS changed my professional career. Your leadership will always be valuable to me 🙏🏾

Thanks Gary. Good to know.