With the renewed runup in interest rates, I thought it would be appropriate to revisit the homeownership market via a frenzy of charts. Of course, all real estate is local, but these overall trends are pretty powerful, so it would be unusual for most markets to be immune to them.

Since most people use debt to purchase their homes, mortgage rates are vitally important in stimulating or dampening demand. One can see that mortgage rates are hitting 7% again, which is a tremendous jump from one year ago.

Here is a more real-time, granular view of rates. As of late last week, mortgage rates breached 7%, and you can see how they’re up dramatically across all loan types.

After purchasing $1.3 trillion of mortgage-backed securities between 2020 and 2022, the Fed is finally cutting back its holdings with a modest start of a $100 billion curtailment. It has a long way to go to get to where it was pre-pandemic. Unless it chooses to sell some of its holdings, it will have to wait a long time to get repaid because, with rates so much higher than the average mortgage rates within its portfolio, there is very little incentive for homeowners to refinance. And if they choose to sell and pay off their mortgages, then they face the prospect of borrowing at much higher rates.

Borrowers not only benefited from low 10-year Treasury yields, which is the main index upon which mortgage rates are derived, but also from very low spreads over that index. This is because with the Fed being such a large buyer of mortgage-backed securities, it pushed up demand to very high levels, which made these securities expensive to buy and resulted in these low-risk premiums being passed onto borrowers. This has now reversed in a very meaningful way, although it’s coming down from its peak in October and November when the spread hit 3%, which was even higher than the worst of the mortgage crisis in 2008-9. Nevertheless, the premium demanded by purchasers of mortgage-backed securities over government-backed Treasuries is at very high levels, which, along with much higher 10-year Treasury yields, has pushed mortgage rates to north of 7%.

Much higher mortgage rates have slowed down price gains, and it looks inevitable that they will go negative in the months ahead.

From Redfin’s vantage point, however, prices have already fallen.

The culprit, of course, is a dramatic decline in affordability. With housing prices still elevated and mortgage rates much higher, incomes have not come close to keeping pace with the much higher monthly payment to purchase a home.

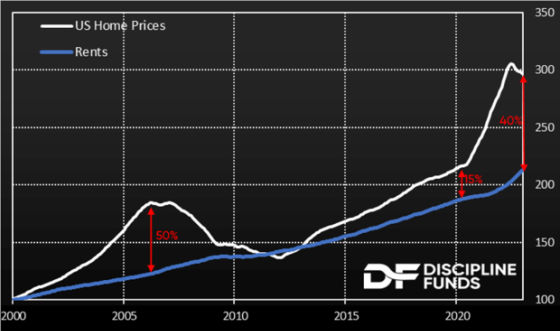

This chart shows how home prices have become much more expensive relative to rents. Either home prices have to drop, rents rise, or both drop, but home prices do so much more than rents. Anyway, you look at it, there’s a disequilibrium that does not favor single-family home prices staying at this level.

The following headline from Bloomberg sums up the situation quite accurately and succinctly.

The percentage of homes bought by first-time home buyers was at a record low in 2022 at 26%. At CWS, we have been saying for many years that one of the tailwinds for apartment demand is that people are getting married later, which naturally results in them starting families later as well. A major catalyst for purchasing a home is needing more space to accommodate growing households. Unfortunately, for many who may now be ready to purchase, it has become much more expensive and will further delay leaving the rental pool.

Indeed, the median age of first-time buyers jumped from 29 in 1981 to 36 in 2022 — the oldest in the National Association of Realtors records. That’s because home values have far outpaced wage gains, said Skylar Olsen, Zillow’s chief economist.

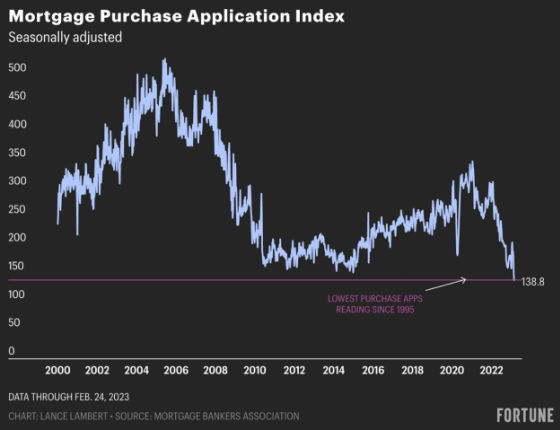

The demand for purchase mortgages has, not surprisingly, plummeted as borrowing rates have shot up and affordability is at a very low level.

Here is the index on a much longer-term basis and puts the magnitude of the current contraction in demand in perspective. Although the drop was nothing like it was from 2005 through 2015, we are still at very low levels of demand on an absolute basis.

This next chart shows how residential construction spending has grown significantly over the last four years and has dramatically outpaced the relatively muted growth in non-residential construction.

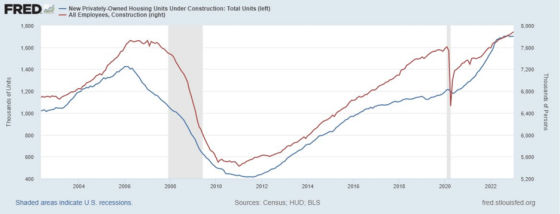

I have written previously about the missing crack in the job market is construction workers being cut on a meaningful scale. This has been a common feature of past recessions, but no signs so far of this happening. There’s a belief that labor hoarding is going on due to the perceived temporary nature of higher interest rates and the prospects for much higher government spending on infrastructure. I’m watching this very closely. If apartments are any indication, however, we should start seeing layoffs in this arena towards the latter half of this year, as we are hearing about a lot of development projects being dropped because they can’t get funding. At the same time, there is still a huge number of multi-family units under construction that need a large construction labor pool to complete.

This chart shows how construction employment has grown with housing starts.

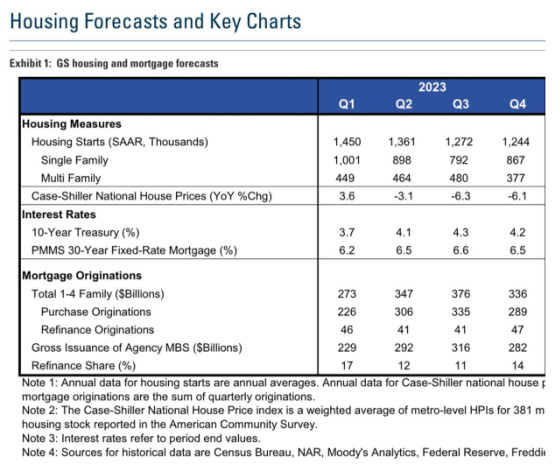

Here is Goldman Sachs’ forecast for housing starts, home prices, interest rates, and mortgage activity. One can see that it’s not surprisingly projecting a drop in housing starts (approximately 15% for 2023) as well as a fall in home prices. Mortgage rates are anticipated to be approximately 6.5% for the year, with very little refinance activity.

The Fed is in a bit of a conundrum. It wants to use much higher interest rates and the contraction of its balance sheet to curtail demand such that inflation comes back down to its stated target of 2%. Rent increases were a big contributor to this inflation as huge demand was unleashed in the wake of Covid, which led to more households being formed as people occupied more space per dwelling unit since they were doing more work from home. At the same time, supply chain issues, along with labor challenges, made the delivery of apartments take much longer than historically had been the case. This led to a supply and demand imbalance which resulted in rents exploding higher.

These trends are now reversing as remote work is no longer as prevalent and apartment supply is coming on in force. This should serve to slow the rate of rent growth quite significantly. On the other hand, the Fed’s extremely aggressive approach to raising rates is undoubtedly going to lead to much less supply of new housing as the affordability of new homes has plummeted. This should keep people renting for longer than they otherwise would have, which could serve to raise apartment rents at a faster rate and hurt the Fed’s war on inflation.

{kind=link}

Gary, you are dead-on in your assessment, Orange County has been defying the gravity of the situation due to a supply crisis and although less Buyers, there are half the homes of normal. We need something to shake up the economy that will motivate people to leave their mortgages. A temporary restrain on Capital Gains perhaps targeted at the 60 year old and over group, so many have multiple homes want to sell, but they won’t sell because of taxes; ins. Remember the temporary restrain on 1099 income of unpaid debt during the housing crisis? It worked and everyone finally stopped stalling and sold.

This is a supply side housing crisis and prices are still strong. I know the day will come when I hear everyone say, “I remember when I could of sold my house for…” This state is losing it’s youth because they have allowed single family homes to be owned by corporations, used as VRBO’s, used as rehab centers and a host of other things. Between all these ownership uses and capital gains, plus with 70% with mortgages under 4%, who and why would someone move unless it’s a life changing event?

Why would anyone trade-up from a 3% mortgage to a 6% if they wanted a larger home? All these issues are creating a situation were people are staying longer in their homes. The turnover rate has gone from 7 years to 22 in Orange County since I entered the business nearly 35 years ago. Amazing window of opportunity for homeowners to sell and ride the market down or get out of O.C. The big question, is where to go?? Great blog, keep up the good work!!

Great insight Greg