Give me a word

Give me a sign

Show me where to look

Tell me, what will I find?

What will I find?

Lay me on the ground

And fly me in the sky

Show me where to look

Tell me, what will I find?

What will I find?

I’m a big admirer of independent thinkers and people who have confidence in themselves and their craft to live their lives in ways that work for them without much concern about what others think of them. Last week I saw Collective Soul, a band with a number of hits over the years and one I had never seen before. They were playing at a small venue, and the tickets were reasonably priced, so I figured, why not? I’m sure glad I decided to go because it was an amazing show, one of the best I’ve seen in a long time. And even though they played for a little under 90 minutes, the show rocked from beginning to end, and you could sense how much fun they have playing together, how connected they are as a band, and how incredibly talented they are. The founder and lead singer, Ed Roland, has a very distinctive voice and, what I would come to learn, a very personal sense of style.

One of these things is not like the other. The other four members of the band were all dressed in black, and then there was Ed.

He said that his outfit was more well suited to going to watch a tennis match or pickleball game versus being on stage as the frontman of a rock and roll band. I couldn’t stop laughing seeing him up there wearing that. And yet, somehow, he pulled it off, and it added to his ever-present sense of joy, gratitude, and awe that he was still doing what he has loved since he was a kid playing music in his parent’s basement (with his brother who is also in the band) in 2023, the year he’s turning 60, and able to make a nice living doing it with people he loves.

He said they recently spent a month in Palm Springs recording at the home Elvis used to own. Having learned this, his choice of outfits made a lot more sense as I spend a lot of time out in that area as well, so I’m familiar with some of the fashion choices there.

Now to the matter at hand. What do Ed Roland and Collective Soul have to do with this blog?

Independent thinking. I have been admittedly perplexed that the labor market has held up so well in the face of a very hawkish Fed that is intent on reducing wage growth by curtailing the demand for labor. Monetary policy acts with a lag but when looking at unemployment claims and the monthly non-farm payroll reports, it seems to be hanging in there. I then read a very thought provoking thread on Twitter that has zeroed in on what could be the primary reason: construction employment.

In most recessions, construction employment has dropped fairly significantly. If recessions were triggered as a byproduct of the Fed fighting inflation by raising interest rates and tightening monetary policy, then this would typically lower the demand for housing as higher mortgage rates make homes less affordable while also making constructing apartments less profitable for developers absent a material increase in rents. Another cause of recessions has been bubbles bursting as they did with the dot com crash that took place between 2000-2 and the subprime collapse that occurred between 2007-9. The latter had a far greater impact on construction employment because housing was at the epicenter of the cause of the bubble, and it was doomed to burst and be deflated. In those two cases, the Fed ended up lowering interest rates quite significantly to help avoid financial contagion, whereas in this one, it has raised rates aggressively to crush inflation.

The following chart shows how construction has ebbed and flowed going back to 1965. It is clearly cyclical as it rises during expansions, drops during recessions, and ultimately recovers all the jobs previously lost. This makes sense as the economy does expand over the long run, albeit with some interruptions, due to population growth, labor hours worked, and productivity gains.

One can see how construction employment growth was on a nearly uninterrupted path higher between 1992 and 2006, and then the subprime crisis hit. Construction employment collapsed and only surpassed the previous peak more than 16 years later.

Since 1973 there have been five downturns in construction employment. The average loss of jobs from peak to trough was 15.9%, with the smallest being 2.5% between June 2000 and February 2003 and the largest being 29.8% between January 2007 and January 2011.Click To TweetOne way of trying to determine how much potential exposure there is for construction job losses is to look at the percentage of construction jobs as a percentage of overall jobs to see if there is an overconcentration in this sector. A couple of observations. One can see the high concentration of construction jobs in 1973 and 2007. Not surprisingly, both saw very sharp contractions when the economy faced inflationary pressures in the early 1970s, and the subprime bubble collapsed in 2007.

In terms of where we stand today, we are at a similar percentage as the peaks in 1979, 1990, and the Covid peak of 2020, although that was so fast and unusual that I wouldn’t extrapolate from that experience except when it comes to labor hoarding, which I will discuss later. With the exception of the early 2000s, the percentage tended to drop to somewhere between 4.2% and 4.5%. I think the 2000-3 period was an exception because the Fed lowered rates quite dramatically, and this led to strong demand for home purchases. It was a very painful time to be an apartment owner, however, as a lot of jobs were still lost, but those who were employed could now buy homes oftentimes at a lower monthly cost than renting an apartment. I distinctly remember this time being extremely challenging for us at CWS.

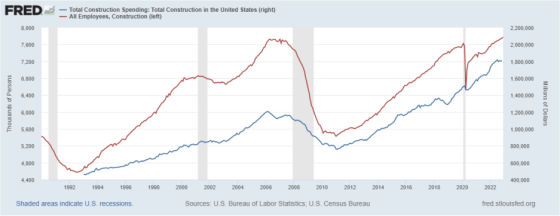

If we use a rough estimate of a 15% drop in construction employment, then this would result in 1.1 million jobs lost.Click To TweetI must say, though, that this feels too heavy, although if we think about a drop in the 10% range and add the multiplier effects, then total job losses of 1 million or so starts to seem more plausible. This chart shows total construction employment overlaid with construction spending. Not surprisingly, they tend to move in the same direction. One can see how construction employment got way ahead of construction spending in the 2000s. And while construction employment dropped sharply during Covid, spending did not, thereby leading to a quick rehiring of construction workers.

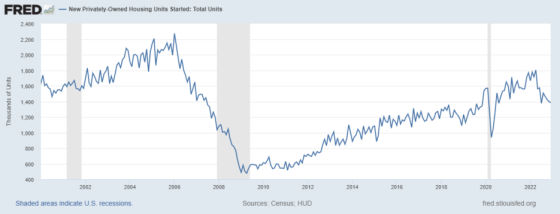

There are clearly headwinds for construction spending and, ultimately, employment. New home starts are falling.

This is not surprising as new home sales have dropped in the wake of higher mortgage rates, and starts are following in the face of weaker demand.

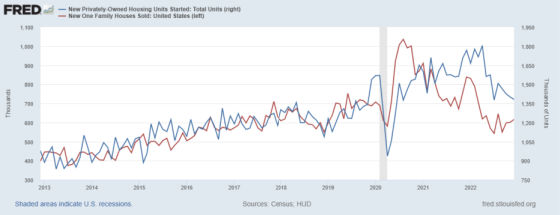

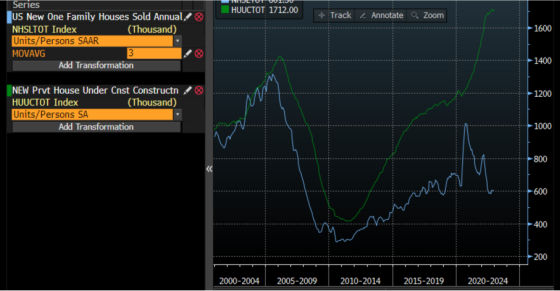

Here is another chart showing the very large gap between new single-family home sales and new homes under construction. This shows why builders have slowed down starting new homes. There are too many homes that are under construction and in inventory relative to the diminished demand.

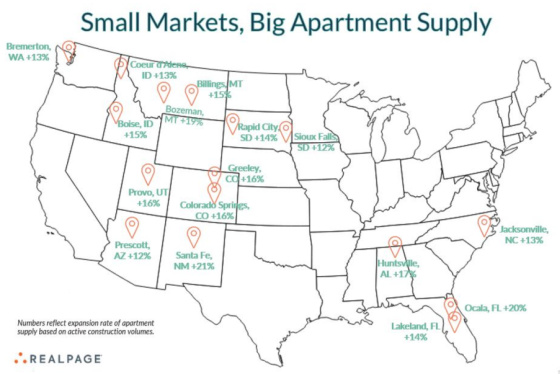

Apartment construction has also been quite elevated. And while it is starting to drop, there is still a huge pipeline that obviously requires construction workers to complete the jobs.

From this map, it appears that smaller markets that benefited from remote work mobility may be at the highest risk of overbuilding. Similar to firms like Meta, Facebook, and Amazon, which expanded during Covid based on the assumption that the demand increase was permanent only to find this was not the case, apartment developers in smaller markets may be facing similar circumstances.

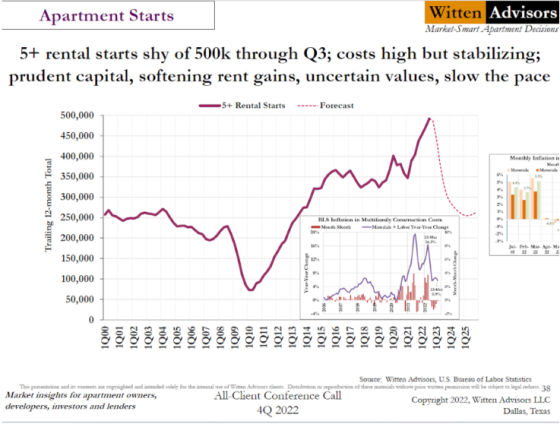

We have been hearing about a lot of apartment development projects being dropped because developers can’t get the equity and/or debt terms and have made the deals non-economic with higher rates and more conservative underwriting standards. Witten Advisors, a multi-family research firm with whom CWS works, is projecting a fairly meaningful drop in apartment starts over the next three years.

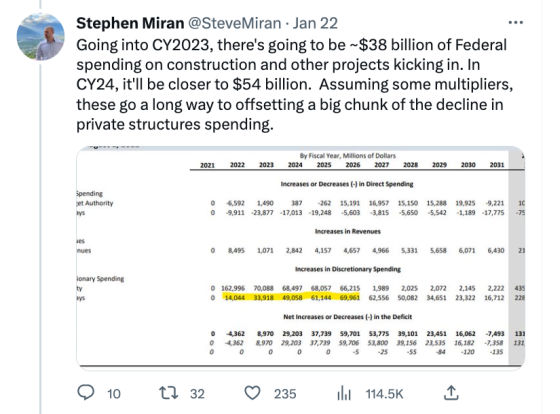

With a contraction in housing construction, very little need for new office buildings, retail still weak, and industrial showing some signs of slowing down, there are a lot of headwinds facing construction spending. The one bright spot, however, is the planned construction spending from the Infrastructure Investment and Jobs Act.

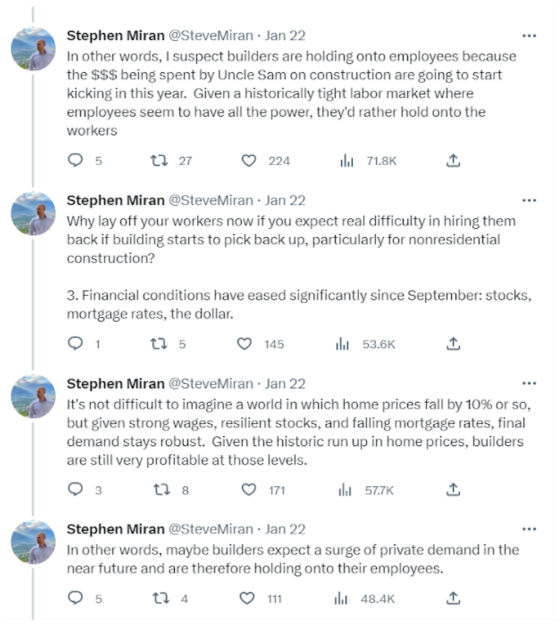

After builders learned during Covid that they were premature in laying off construction workers (20-20 hindsight, of course), they are probably much more hesitant to do so again, especially since public construction spending is set to really take off. Of course, not every builder can pivot to that type of work but from an overall construction labor standpoint, the job losses may be less than previous correlations would have predicted because of a tighter labor market leading to labor hoarding and large public spending on the horizon.

I think this thread sums this up nicely.

So there you have it. I previously wrote about how all eyes were on the Two-Year Treasury yield to ascertain when a Fed halt or pivot may be upon us. Now I would add construction employment to this as well, as this holds the key to whether a recession will materialize or the immaculate disinflation and soft landing will have been engineered by the Fed with the help of the federal government.

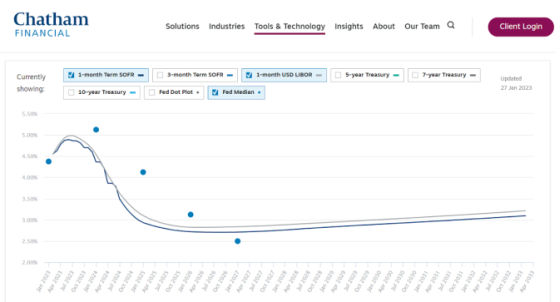

Thank you, Ed Roland and Stephen Miran, for reinforcing the power of independent thinking and living a life of authentic self-expression. I now have to moderate my thinking regarding the inevitability of a painful enough recession such that the Fed will drop interest rates to around 2.50% (the rate they have the Federal Funds rate leveling off at in the future). Per this chart, it looks like the market thinks we’re going to have a bigger downturn than the Fed thinks but in the longer run not significant enough to result in rates going as low as the Fed believes. Only time will tell. In the meantime, keep eyeing the Two-Year Treasury yield and construction employment for windows into the future.

{kind=link}

Leave a Reply