Cantor Fitzgerald CEO Howard Lutnick – Bloomberg Television

In a recent interview on Bloomberg Television, the CEO of Cantor Fitzgerald, Howard Lutnick, was asked what he thought about young investment bankers complaining that they were being overworked.

The headline for an article about the interview captures his opinion quite succinctly.

Lutnick is an incredibly accomplished, tenacious, and successful CEO who famously and courageously navigated the loss of 658 out of 960 of its New York City employees on September 11th, 2001 to rise out of the ashes to build a very powerful investment banking firm as well as a strong real estate brokerage holding company. What he did to rebuild the firm is nothing short of astounding. He is as Type A as they come. Lutnick is the prototypical Alpha Male so his attitude is hardly surprising.

While some may take what Lutnick says as callous, I call it realistic. There are certain professions in which a lot of money is on the line with clients calling the shots who are willing to pay top dollar for expertise, competence, effectiveness, and reliability to get things done to meet important deadlines. It also applies to medicine when people’s lives are in the balance and they need top care without delay. Our bodies and circumstances don’t work on a clock. We need what we need when we need it. Here are a couple of Lutnick’s comments.

“Young bankers who decide they’re working too hard — choose another living is my view,” Lutnick said Thursday in an interview on Bloomberg Television. “These are hard jobs.”

“There is a path to becoming an investment banker that requires an enormous amount of work,” including late nights and weekends, Lutnick said. Clients want their deals finished under tight deadlines, he said. “You should know that going in.”

If you want to be someone who does well financially but elects to enter a career on the client services side then you have to know that rising to the top not only comes with commensurate financial rewards but can also entail having to work in very high-pressure environments requiring enormous hours of work. This is particularly true for attorneys and investment bankers. It is not easy being at the beck and call of very demanding and, yes, high-paying clients, at all hours of the day and on weekends. It is very difficult to truly break free from the work and decompress. And while it can often come with very high financial rewards, the costs can also be quite high as well in terms of the toll it takes on one’s health, relationships, and family functionality.

The stresses and strains are not just for investment bankers, lawyers, and doctors. In a fascinating study, public company CEOs bear a lot of the burden as well. I will discuss this shortly.

Over the years we have had discussions at CWS as to whether we want to go public and access capital in that manner versus continuing to do so privately. Every time the subject is brought up I keep thinking about the scrutiny by analysts, investors, media, the SEC, and the regulatory compliance associated with being public and I get a pit in my stomach. I love working in a private company with partners who I admire and respect greatly. We are able to collaborate and try to align on the best course of action and strategic direction based on doing what’s smart when it’s smart and not being pressured by outside forces who may have their own idiosyncratic needs that may interfere with what is best for the investments.

This is not to say that having investor accountability can’t make us a better company because over the years it has. It’s just that we have found that it has been much more challenging and frankly sub-optimal in terms of organizational stress and resources devoted to investors who represent institutional money or individual capital who may be operating more out of fear than understanding and accepting of the variability and vicissitudes of owning apartments over the long run and that it is not an investment that is optimized by short-term thinking.

A budget is a way of capturing the priorities and financial picture of an investment as well as the resources available to reinvest in the property and what’s available to distribute to its owners each year. It also should not be an end all be all because it has only a one-year time frame connected to an asset/business that should have the potential to exist for many, many decades if managed well and in an area with stable to growing demand. Budgets will be missed because the unexpected can happen. That doesn’t mean the process shouldn’t be reviewed to understand why the variances materialized, but it shouldn’t automatically lead to fear and paranoia and make decisions to make cuts to get back on budget when this may harm the competitiveness, safety, or upkeep of the property. It’s not wise to look at investments with the potential to live in perpetuity through a one-year prism.

The institutional investment world has incentives and constraints that often have people more focused on career preservation and job security than independent thought and doing what is right for the investment even if it’s costly in the short term. Endless reports and CYA are not the path to investment success. Generating great insights, having the capability to act on those insights, accessing the right debt and equity capital to take advantage of opportunities quickly as well as to give breathing room to execute the plan and allow for the risk of going off track, and having a resilient organization that can identify and prepare for risk and recover from setbacks are some of the attributes needed to make successful apartment investments. What is not needed are overzealous, short-term oriented, insecure outside parties that are being driven by their own fears that get in the way of interacting with us in an open, honest, and professional manner such that we can add the most value together.

For whatever reason, the way I’m wired I feel that I am much more suited to working in a private firm in which I have some influence than being in a public company with many stakeholders looking over my shoulder, even if the monetary rewards are potentially greater. And after reading a summary of a report published by the National Bureau of Economic Research, my feelings for wanting to stay private have only grown. The title of the study is CEO Stress, Aging, and Death. It’s not the most optimistic title but it gets to the heart of the research. The headline of the article is as follows.

Because CEOs of public companies are usually financially secure, the authors wanted to look at the stress of running a public company under the pressure of being at risk of a hostile takeover or managing the business when it’s under financial duress. Since they are financially secure this variable should not be a cause of negative health outcomes. This allows them to focus on the non-financial price of being at risk of a buyout and dealing with corporate financial distress.

Being the CEO of a public company, particularly one that is at risk of being taken over and/or experience financial distress, is detrimental to one’s health as compared to those who don’t face the same concerns and challenges.Click To TweetThe authors find clear evidence that being the CEO of a public company, particularly one that is at risk of being taken over and/or experience financial distress, is detrimental to one’s health as compared to those who don’t face the same concerns and challenges.

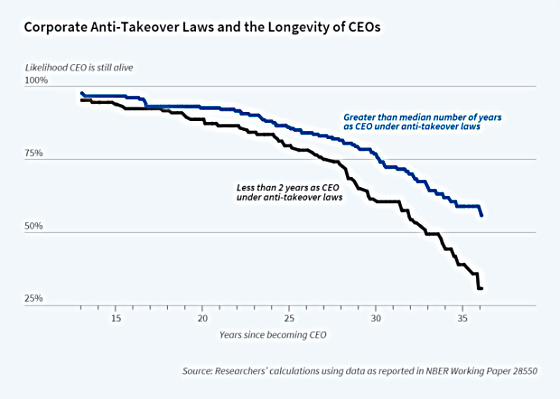

The researchers studied CEOs whose companies were domiciled in states that had laws that made hostile takeovers more difficult and those in states where there were no restrictions. The former would obviously be under less pressure from a hostile takeover arising as compared to the latter. This is what the researchers found.

Working for more years with anti-takeover protection was associated with longer CEO life expectancy. Working an additional year in a legal environment with greater takeover protection lowered the annual mortality rate by about 5 percent for a typical CEO, increasing his or her lifespan by just over two years.

And the longer the CEOs worked under anti-takeover laws, the longer their life expectancy compared to those who worked less time under them as the following chart shows.

Since we don’t have to worry about being taken over, this stress is not present for us at CWS. What we do have exposure to, as well as all public CEOs, is the risk of a material downturn in our business. And I know from experience that this can be extremely stressful because of the responsibility we feel to our investors to protect their capital. Downturns often necessitate dividend cuts and sometimes the need for additional capital. These are not fun conversations to have with investors but they are necessary because the goal is to not lose properties that will come out the other side much healthier if there is the financial and emotional staying power to ride out the storm.

What did the authors find out about the impact of financial stress on a CEO’s life expectancy?

The researchers also study how industry-wide distress — defined as a 30 percent drop in the stock price of the median firm in the industry, persisting for at least two years — affects CEO longevity. Forty percent — 648 out of 1,605 CEOs in the sample — experienced at least one period of industry distress. Fewer than 20 percent experienced two or more shocks, and fewer than one in ten faced three or more shocks. CEOs who were in office during industry-wide distress, on average, died 1.4 years earlier than those who did not experience such shocks. This effect is smaller than the estimated effect of BC laws, perhaps because the latter apply to much longer periods.

The lesson here is to follow the advice that Warren Buffett gives about how to avoid avalanches. Don’t be on the mountain when one strikes. Run a company with very good fundamentals and build it for resilience. The research shows that 40% of CEOs in the study experienced financial distress at least one time. This is not an insignificant percentage and shows the importance of building a company that recognizes that downturns have a high probability of occurring and doing one’s best to prepare for them.

Finally, in what I find to be the most fascinating part of the study, the authors use machine learning software to look at pictures of CEOs before and after the financial crisis of 2008 to come up with how many excess years they have aged compared to those who didn’t run firms under financial stress. We all see how presidents grow much older looking after four to eight years in the presidency and we intuitively know it must be largely related to the stress and incredible responsibility of the job. Presumably the same would be true for CEOs who ran companies that were under financial distress during the financial crisis.

The study also considers stress associated with the 2008 financial crisis. The researchers analyze the evolution of the “apparent age” of corporate leaders (how old they look), comparing those who led firms that were hard-hit by the crisis with those at firms that were less affected. They measured CEOs’ “apparent age” using visual machine-learning software, which was applied to about 3,000 pre- and post-crisis facial images of a recent CEO sample consisting of the 2006 Fortune 500 CEOs. Prior to the financial crisis, the software generally returned estimates of apparent age that did not systematically vary depending on whether CEOs would subsequently be hit hard by the crisis. During and after the crisis, however, there was a substantial increase in the “apparent aging” of CEOs leading firms in distressed industries compared with other CEOs. The apparent age of CEOs in industries that suffered the most during the crisis rose by about 1.2 years more than that of the CEOs in non-distressed businesses.

What’s the bottom line of their research?

The researchers conclude that “stricter governance and economic downturns constitute a substantial personal cost for CEOs in terms of their health and life expectancy.”

When I look at pictures of Howard Lutnick he does not seem to have aged rapidly in spite of all of the pressures he has faced over the years. Something tells me he thrives on crisis management and being in the public spotlight.

If this is not how you’re wired then I suggest you think long and hard about going into high-pressure fields where missing deadlines have huge consequences and the pressure you get from clients and investors can be relentless.

The financial rewards may be very significant but from the research cited it can come at a cost to one’s health and welfare.

{kind=link}

Leave a Reply