Last week we had our annual investor meeting for CWS. This was a huge milestone as we celebrated our 50th anniversary. The attendance was a record with more than 600 people taking time out of their busy lives to join us for dinner and presentations from the CWS principals.

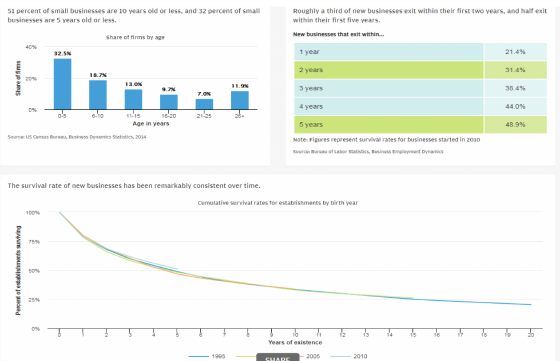

I focused my presentation on some of the reasons I think we have been able to survive and prosper for 50 years. First, to put how improbable a 50-year business is, I shared a few charts to convey how we are in pretty rarefied air. As the following charts and tables show, there’s an approximately 50% chance that if one were to start a business today that it would still be around in five years and after 25 years that would drop down to approximately 12%. So one can imagine that 50 years is a lot smaller of a probability and a business such as CWS is a rarity.

What has enabled us to be able to survive and prosper over this period of time? I think it goes back to Bill Williams and Jim Clayton starting off by raising money from friends and family and the tremendous responsibility that goes along with that. They are highly competitive people who do not like to lose and this translated to them having a fierce commitment to not losing their investors’ money. It continued after Steve Sherwood joined Bill and Jim and remains central to how we operate the business today. It is embedded in our DNA and our culture to do everything in our power to preserve the capital that has been entrusted to us. Only after we feel like we understand the downside can we then focus on the upside. Many firms who have not been as fortunate as CWS learned the hard way that they had it backward and did not truly understand or care to acknowledge the risk they were bearing.

CWS at 50

What have been some of the important ways we have tried to manage risk? To pull from the Buddha who emphasized in the Noble Eightfold Path things like right speech, right effort, right action, etc. there are also some critical “rights” to lessen the probability of losing money for CWS.

Right Focus on the Right Business – One way of determining what a good business is to use Charlie Munger’s inversion approach and first ask what are characteristics of a bad business? As he is famous for saying, “ “All I want to know is where I’m going to die, so I’ll never go there.” More directly, Warren Buffett has said, “When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact.” Here is an example of a bad business: Department stores.

A good business has compelling long-term demand fundamentals which enable its owners to have pricing power to absorb cost increases and to generate an acceptable return on capital deployed. Apartments have exhibited those characteristics and we have been able to do well investing in them because of their positive attributes.

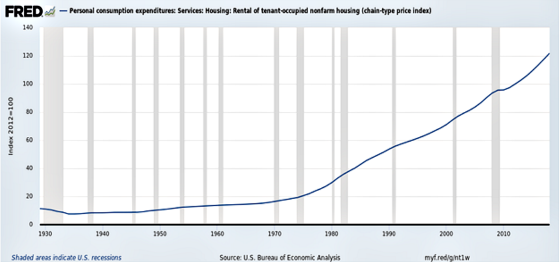

To put this in perspective, the following chart shows the government’s estimate of rental housing consumption over many decades. One can see that it has been in a continuous uptrend which is a business that has a high probability of longevity, particularly if it fills a basic need, such as housing, that is not easily disrupted.

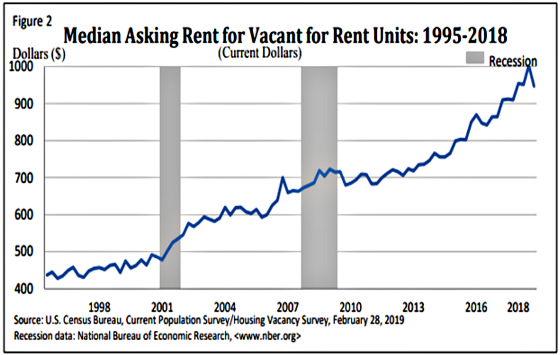

The next chart shows a proxy for rental housing rent growth. One can see that this meets another important characteristic of a good business, which is pricing power.

Right Locations – To generate a compelling return over time one also has to be in the right locations. The markets that we are in have generated jobs at approximately four times the rest of the country since 2000. The same is true for population growth. We believe we have done a good job of going where the growth is as well as the high-paying jobs. We have been focused on where knowledge workers want to be since the late 1990s and this has served us well.

Right Financing and Right Investors – We have come to learn how important it is to have the right financing in place to give us options to be able to refinance loans when rates or structures become more favorable or to be able to sell properties without being constrained by onerous prepayment penalties. The tradeoff has been that we have taken on interest rate risk compared to fixed-rate borrowers and this has led to volatility in our cash flows. With that being said, however, thus far we have still generated significant interest savings and the relatively minor prepayment penalties that come with these loans have enabled us to make early repayments since 2013 of 70 floating rate loans of over $1.7 billion via refinances and property sales, generating prepayment savings well in excess of $100 million as compared to what we would have had to pay in prepayment penalties for fixed-rate loans. Of course, we were not able to refinance our complete portfolio in that time frame, but we would be happy to share the entire portfolio performance during that period upon request. For example, in 2015 we refinanced 18 properties when interest rate spreads compressed and loan structures became more favorable with longer interest-only periods. In addition, at the end of 2018, we refinanced 12 loans to take advantage of another favorable window for borrowers. We could not have done this with fixed-rate loans as the prepayment penalties would have been too onerous. We had the added benefit of having our prepayment penalties waived because we refinanced with the same lender. This would not have been possible with fixed-rate loans, as they do not waive them even if refinancing with the same lender.

Once we have the right business, apartments, in the right locations and matched with optimal debt capital, it’s then critical that we bring the right investors into the fold who share our long-term orientation and recognize that apartments are a get rich slowly type of business that requires patience and capital to weather inevitable downturns. With such partners, we become more able to manage the cyclicality of the business and better align the returns we think we can generate with our investor expectations.

Right Team – With the right business in the right locations financed with the ideal debt and equity we have found that controlling our own destiny has served us well by having a deep and capable team to execute our business plans and comprised of people who embody CWS’ values and are additive to our culture. And because the environment is always changing we must also be able to generate compelling ideas so that we can continue to add value.

Putting that altogether results in the “easy” way of being successful.

The hard way is when problems arise. And with over 100 properties in our portfolio and the more than 70 properties, we have sold since being in the apartment business, we will inevitably make mistakes. Our premises may be wrong, our assumptions too optimistic, or we just can’t hit our stride. Whatever it is, we will not get them all right. And this is where the rubber meets the road. Fortunately, apartments, because they have winning characteristics for the long-term investor, particularly in the right locations, can be somewhat forgiving if you can hang in there during the tough times. This requires strong values, a great team, a sterling reputation, and financial staying power.

And that’s where you need the right values to avoid temptation and a culture and organization that is one of shared sacrifice, cooperation, creativity, competitiveness, long-term orientation, community-oriented, caring, has a commitment to excellence and growing people and with that, we can overlay tenacity and staying power and we will have increased the odds substantially that we will make it through the difficult times and downturns. If you don’t have the staying power then you are going to have a high probability of losing properties when you’re leveraged, times get tough, and rents drop. Despite the revenue decline you still need to keep maintaining your properties and attracting residents to either stay or to move in.

Losing properties is quite detrimental to one’s reputation with one’s lenders and investors as well as hurts one’s track record. All of these conspire to make it more difficult to attract growth capital, particularly during those dark times when values are most compelling. This is something that we experienced when we aggressively invested in the aftermath of the creation of the RTC and in the wake of the Great Recession. It’s vitally important to have capital when it is in short supply and others are playing defense trying to clean up problems and asset values are depressed with a lot less competition to purchase them. Our goal is to minimize errors of optimism during the good times so that we can remain on offense during the difficult times.

So there you have it. CWS 50 years summed up in a little under 1,600 words. It has been an extraordinary honor and privilege to have worked at such an outstanding company with people who are like family to me and will be lifelong friends. And to know that I have played my part in helping to enhance the lives of our investors, residents, and employees make it even more gratifying.

{kind=link}

Leave a Reply