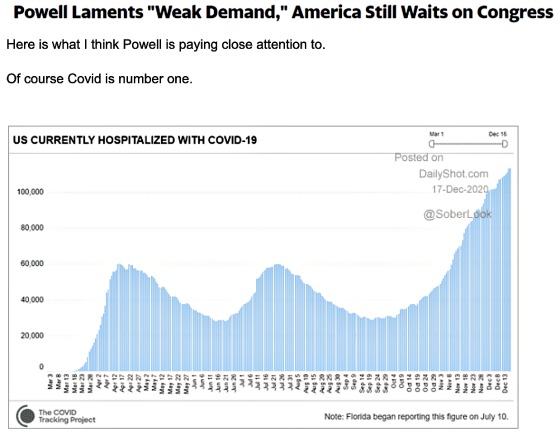

This week will be another one focused on charts and graphs that caught my attention. The emphasis will be on the story of the Fed remaining very dovish in spite of what appears to be some pockets of economic strength (e.g. housing, commodities, semiconductors), higher long-term rates, enhanced inflation expectations, and a very strong stock market valuations, particularly for technology companies. The Fed met last week and this is what Chairman Jay Powell said.

Fed Chair Jay Powell said the Federal Reserve will continue buying bonds until “substantial” progress is made in economic growth.

And until herd immunity occurs, the Fed cannot do all of the heavy lifting so it’s vitally important that Congress act to continue to shore up incomes through more fiscal stimulus.

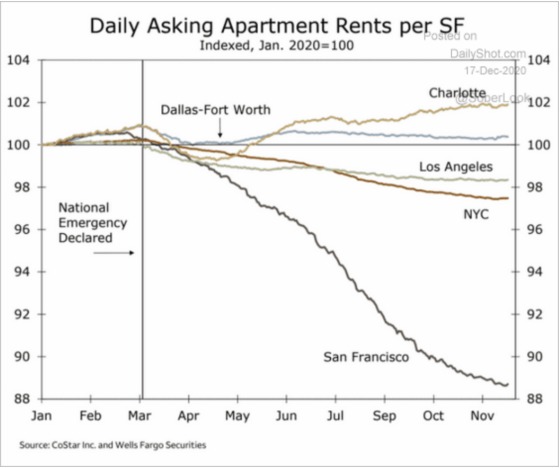

Remote work and the inability or lack of desire for people to congregate in close quarters and in large numbers has decimated the office economy, particularly in urban areas.

Businesses serving workers and people congregating together have been hit hard, as well as urban apartments as there is less desire to live in cities and pay high rents and not have the associated advantages.

The home economy has clearly benefited relative to the office/social gathering economy.

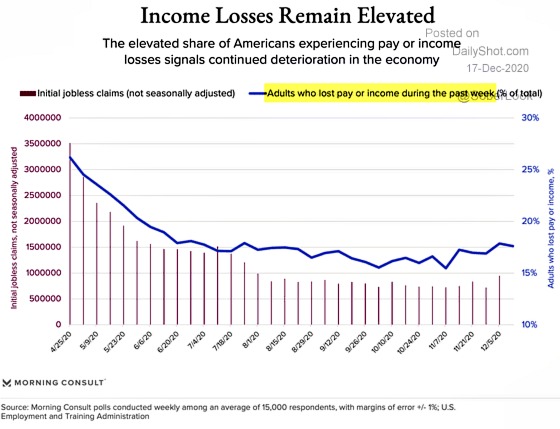

The bifurcated economy of clear winners and losers has led to a still-high percentage of people losing income.

And I think this is the money shot in terms of what is ultimately influencing Jay Powell and his monetary strategy and why he is imploring Congress to act.

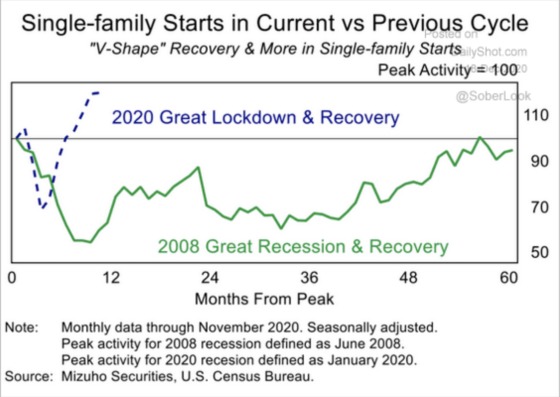

And this trend will probably continue to lead to this.

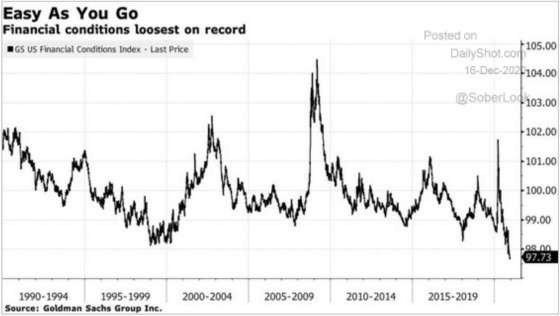

Which has led to this.

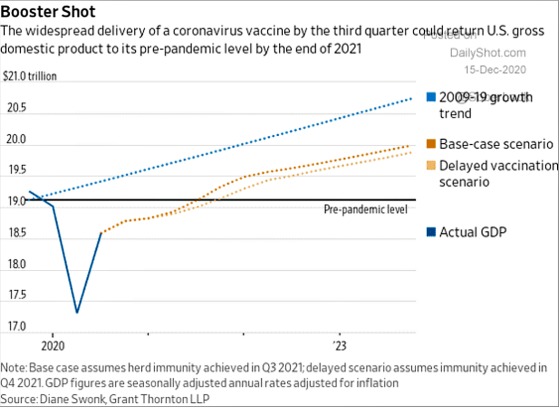

As a result of very loose financial conditions, risk assets have soared, especially for a monetary alternative like Bitcoin which appeals to investors who believe that the dollar will erode in value and inflation will increase as the Fed remains highly accommodative for many years to come.

One of the big winners is of course housing due to record low mortgage rates and more people working from home. Unlike the last recession, housing is a major source of growth.

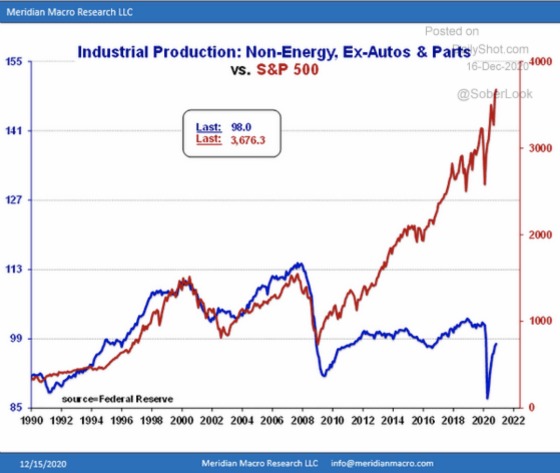

Economic rewards have flown too high growth, low capital intensity technology/platform companies while much of the rest of the economy has produced negative returns.

This has translated to a stock market that has decoupled from industrial output.

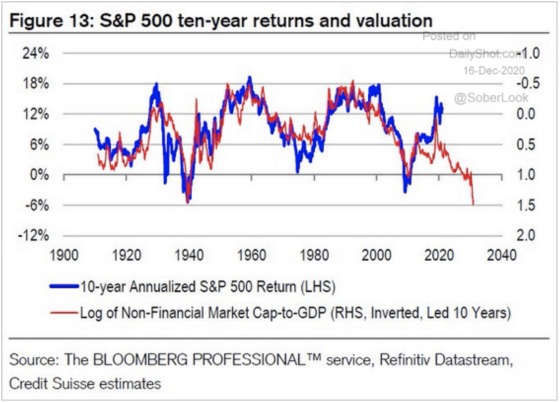

Valuations are now very stretched on a historical basis, although interest rates are also very low.

This doesn’t look so good for future stock market returns, although since tech has dramatically outperformed, there could be compelling opportunities in the more beaten-down value category.

{kind=link}

GARY, great info to plan 2021 business and investing.

thanks,

Bill Williams