Last week, the GDP report for the 4th quarter was released as well as the Fed’s favorite inflation index, the Personal Consumption Expenditures price index (PCE). The Fed should be very pleased with what the reports revealed and how it has defied the overwhelming consensus that a hard landing was necessary to break the back of inflation. To be fair, however, Powell and the Fed, up until recently, thought that a recession would be necessary to bring this about. Its tune is now changing such that it believes it can keep the economy growing and still bring rates down since inflation is dropping quite faster than it expected.

The Fed has navigated through the Covid shutdown, the supply-constrained, inflation-inducing recovery, and the return to trend inflation even after significantly contracting its balance sheet and raising interest rates far faster and higher than virtually anyone would have predicted.

Let’s first look at the PCE.

One can see how the year-over-year of change rate has finally dropped below 3% and looks to clearly be headed to the Fed’s 2% target based on the last three and six months annualized rates.

And when food and energy are stripped out, the core PCE is now below 2%.

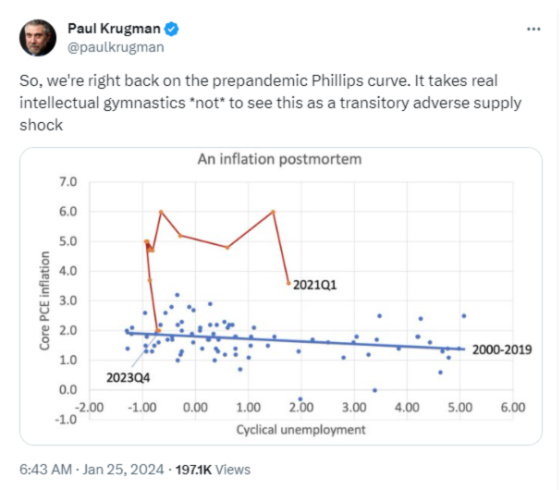

And while the Fed got excoriated for being in the transitory inflation camp (as I was as well), perhaps we were correct after all as Paul Krugman shows. It was a supply-constrained inflation spike, after all, and once the situation got normalized, so did inflation. The relationship between unemployment and inflation has returned to its pre-pandemic trend.

And while the Fed’s balance sheet is still approximately $3.5 trillion above its pre-pandemic size, it has still contracted by approximately $1.5 trillion from its peak.

And here is what happened to the Federal Funds Rate. It went from 0% to approximately 5.33% in one year.

Once it became clear that the Fed would do what was necessary to slay the inflation dragon it was understandable why so many would have thought a recession was an inevitability. This is a great tweet from Ben Carlson that shows how this was the base case for many sophisticated people in 2022.

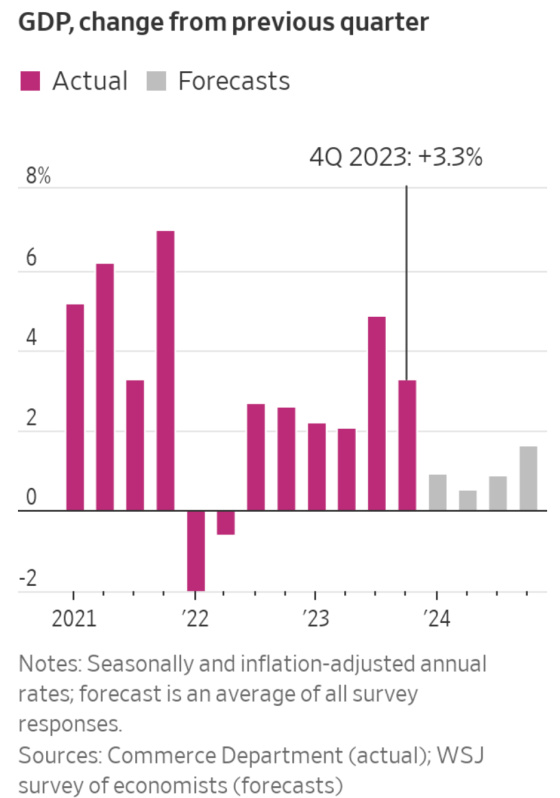

Now, let’s turn to the GDP report to see what it showed.

Growth has been remarkably resilient, given the monetary headwinds. And what’s even more surprising is that growth has accelerated, as this chart shows.

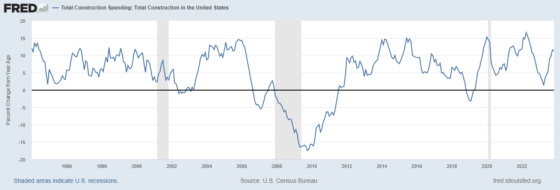

What has been the source of resilience and strength? To me it’s centered around something I have written a lot about before and that is government spending, particularly in terms of construction and infrastructure. Construction spending has not dropped like it has during previous recessions. In fact, it has gotten even stronger. This first chart shows the absolute level of construction spending while the second is the annual percentage change.

One can see that the rate of growth has accelerated.

But now, let’s look at the rate of change for public construction spending. It is mildly off its highest growth rate since 2001, but it is still extremely elevated so this is good visual evidence of the lift it’s giving to the economy in spite of much higher rates.

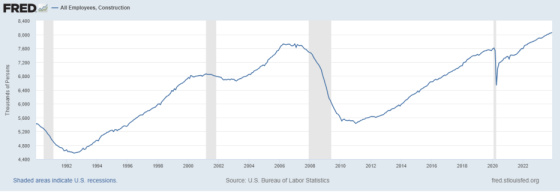

By now, we should have seen over 1 million construction jobs lost, given the rapid rise in interest rates, but instead, they have grown as spending has clearly held up.

Add to this that many homeowners have locked in long-term, low-rate mortgages, and those with cash balances are earning higher risk-free rates of return. Now we have some reasons as to why the economy has held up as well as it has. Here is a good summary.

When all is said and done, there is very little to dislike in last week’s reports. In fact, there was a great deal to like. And while this probably puts off a March cut I think the Fed has enough cover with lower inflation and high real rates to bring short term rates down in the second half of 2024.

{kind=link}

Leave a Reply