Powell did it for the third time. He proved for the third time that you should listen to him carefully until he does something completely different, and then you should listen to him again. After raising rates aggressively starting in April 2022, after he had said that the Fed wouldn’t raise rates until the end of 2023 at the earliest, the market never took him seriously that he would keep raising rates a la Paul Volker and that he would eventually blink and reverse course. He has proven to be one of those paradoxical people who can simultaneously be stubborn and flexible. Every time the market fought Powell, Powell won, and two-year and 10-year Treasury yields would march continuously higher to nearly 20-year highs.

Powell Pivot III

And consistent with Powell’s stubborn streak, Powell was firmly in the camp of no rate cut any time soon up until very recently.

This is what Powell’s stance was related to interest rates almost two months ago.

And even less than two weeks before last week’s meeting this is what Powell had to say.

This is what Powell said in a speech he gave at Spellman College.

“It would be premature to conclude with confidence that we have achieved a sufficiently restrictive stance or to speculate on when the policy might ease,” Powell said in prepared remarks for an audience at Spelman College in Atlanta. “We are prepared to tighten policy further if it becomes appropriate to do so.”Click To TweetHowever, he also noted that policy is “well into restrictive territory” and noted that the balance of risks between doing too much or too little on inflation is close to balanced now.

One couldn’t necessarily blame him for the stance he was taking as inflation indicators, while moving in the right direction, still have some worrisome components to them, and core CPI was still high at 4.0% in the December report. On the other hand, it is expected to keep coming down, but it’s still not currently near the 2.0% target. Some longer-term trends may have it settle out higher than had been the case over the last 20+ years or so. These include de-globalization trends, reshoring of manufacturing, infrastructure spending, green energy initiatives, an aging labor force, and a slowdown in immigration, to name some of the major ones.

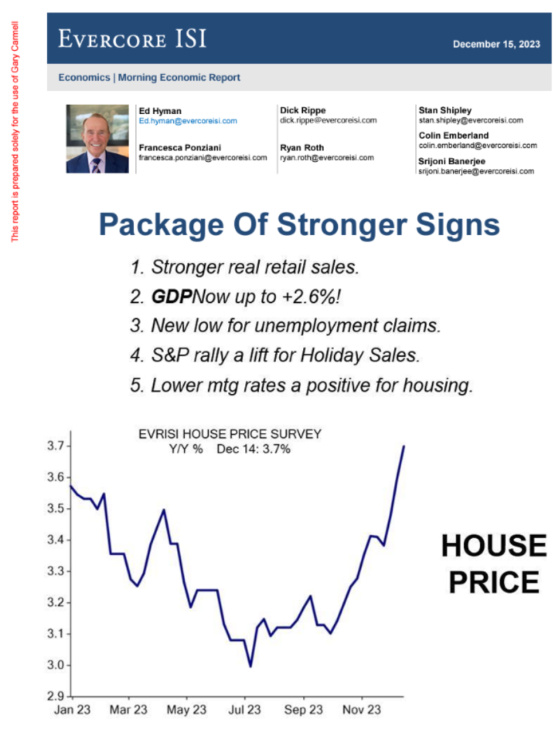

In addition, financial conditions have loosened as rates have come down, even before last week’s huge drop, and the stock market is close to all-time highs. And, as this summary daily economic overview from Evercore ISI shows, the economy is still humming along nicely.

Then, BOOM, the December 13th Fed meeting and follow-up press conference occurred, and the third Powell pivot spontaneously combusted into existence. Powell no longer felt it was necessary to trigger a recession to bring down inflation to the point where the Fed would feel comfortable lowering rates.

Here is the analysis from Neil Irwin of what the Fed’s pivot means. I find myself in agreement with these conclusions.

Why it matters: The end of the war on inflation is in sight. Barring some unpleasant economic surprises, the central bank is now prepared to take its foot off the brakes and move to a stance where it is no longer actively trying to slow growth.

- Importantly, the majority of policymakers are now envisioning significant rate cuts in 2024 while also envisioning the economy remaining basically solid, with low unemployment and steady growth.

- In other words, rates will probably be coming down next year, even in the absence of a severe downturn. That’s a sweet spot both for financial markets and for families and businesses.

- The cycle of monetary tightening that has whipsawed markets and the economy for the last two years is over for all intents and purposes.

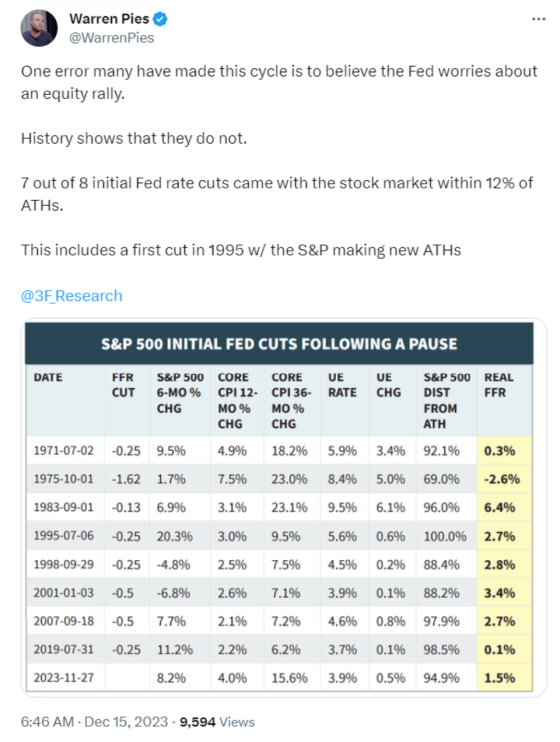

There has been concern that the Fed would not pivot with stock markets performing so well for fear of unleashing further animal spirits and hurting the fight against inflation. However, historically, this has not gotten in the way of the Fed cutting rates, as this tweet and corresponding table show.

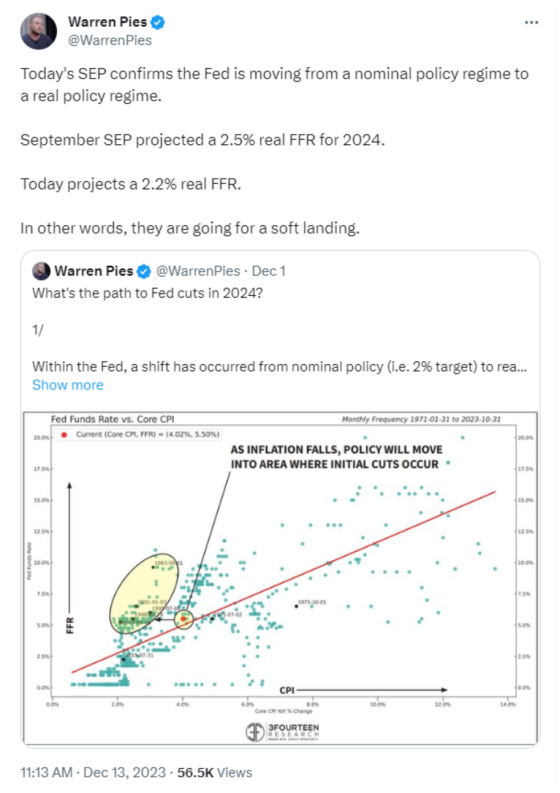

The Fed now believes that inflation is clearly going to trend down to a level such that inflation-adjusted interest rates are going to be too high and that rate cuts will now be necessary to keep economic growth going in 2024. The Fed has now projected three rate cuts in 2024 while the market is up to six. Turning again to Warren Pies, this tweet shows how the Fed typically starts cutting when the real rate is 2.50% or higher and that this will happen in 2024.

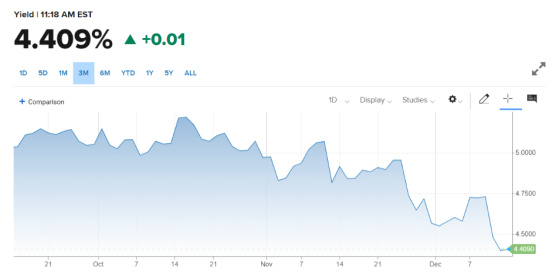

And while rates were coming down prior to the Fed meeting, they dropped dramatically after, as this chart of the 10-year shows. It has dropped approximately 30 basis points in five days.

Here is a chart of the two-year which has dropped approximately 35 basis points over the past five days.

Famed investor Stanley Druckenmiller had this to say in an interview published on October 31st.

Good for him. I’ve always been a big fan of his and have learned much. He has always been willing to change his mind and position on a dime if necessary; this is another profitable example.

CWS

For CWS, this large drop in rates and the Fed clearly now in the rate cut camp begins to take pressure off of our variable rate portfolio. The initial benefit to us will be the cost of interest rate caps dropping. On the other hand, we don’t expect to see much interest rate relief because cuts won’t start for a bit; they will take time to have an impact cumulatively, and in many cases, the caps we have in place are at lower rates than where SOFR is today and will be by the end of next year. What it does do, however, is allow for more of our loans to become refinanceable at materially lower rates than we’re paying now, given the yield curve is still inverted.

Because we almost always gravitated to longer-term, lower leverage, lower spread, full-term interest-only loans, we are in a fairly healthy position despite interest rates having risen so far and so fast. This doesn’t mean we don’t have challenges to contend with, but they are quite manageable overall.

as Warren Buffett has famously said, “It’s only when the tide goes out that you know who’s been swimming naked.”Click To TweetFor other more aggressive borrowers in the apartment space, however, they are facing some existential challenges. These are sponsors who binged on 3-year high leverage, high spread, floating rate loans deployed at peak valuations, and absent a dramatic reduction in rates in a short period of time, I don’t see how they get out of their loan maturity problems without significant pay downs (20%+). Many of these loans were originated in 2021, and 2022 so 2024 and 2025 will reveal who, as Warren Buffett has famously said, “It’s only when the tide goes out that you know who’s been swimming naked.” I’m afraid there will be a not insignificant number of newer sponsors without any experience managing through downturns who had relatively easy access to large amounts of capital, who may not make it, or if they do, will come out severely bruised.

It’s also very possible that those with the second half of 2024 and 2025 maturities may not have the wherewithal to get to loan maturity because many of these loans are contending with significant negative cash flow as leverage levels are high, rates far exceed what was projected, aggressive rent growth was never attained, and costs have increased substantially. And if they had the benefit of an interest rate cap then they will have a payment shock when it expires as well as needing a large amount of capital to purchase new caps if the lender requires these.

Add to all of this more operating challenges as competition heats up from a generational high number of apartments being delivered, and owner-operators are going to be facing headwinds even without bad debt structures.

Given banks’ exposure to office buildings as well as construction loans for apartment developers, particularly among regional banks, the combination of construction delays, cost increases, much higher interest costs than projected, lower rents, and declining values in the wake of still significantly higher interest rates compared to when these projects broke ground, many developers, especially those who accessed mezzanine or preferred equity, will also be facing the need to de-leverage or refinance into new, shorter-term bridge debt that comes at a high cost. Essentially they will be buying time in order to avoid having to come up with cash to get out of their construction debt in order to get to the other side when apartment fundamentals improve significantly because new starts will be coming to a screeching halt.

It will be particularly interesting to see what happens when properties with mezzanine or preferred equity need additional capital and those investment groups don’t want to put in more money. Will they allow new capital to come in ahead of them? If not, then there’s no incentive for the new money to fund. Perhaps these groups will bring in the necessary funds and further dilute the original equity. These structures will add more complexity and challenges to coming up with resolutions for overleveraged real estate.

All of this is to say that while the Fed pivot is definitely very helpful for a company like CWS, it will do very little for office building owners and over-leveraged apartment owners and developers because cap rates won’t come down enough to overcome the valuation issue impacting the collateral and rates won’t fall far enough and fast enough to turn negative cash flowing properties into break even or better. It will, of course, lessen the pain, but the patient may have lost too much blood by this point to be able to survive, even if the bleeding has lessened. For this myriad of factors, I think cap rates will remain more elevated relative to interest than they have in the past to compensate investors for the risk of more distressed assets coming to market, which can impact values, operating income that is at risk of deteriorating, and lending standards staying relatively conservative.

{kind=link}

Thanks for the update!