Last week we had our annual investor meeting. It was the first time we met in person since 2019. It was so nice to be together again. Despite not communicating the rosiest of messages, it was an evening that had great positive energy. We showed how higher interest rates have negatively impacted our cash flows, given our reliance on variable-rate debt. I spent the bulk of my presentation discussing why we have emphasized variable-rate loans since 2011 and why we didn’t convert to fixed-rate financing when rates were lower. The presentation was too lengthy and detailed to cover all of it here. I thought I would focus on one aspect, which was showing two datasets that have influenced our thinking as to why variable rate financing offered such a compelling risk-reward relationship.

The underlying premise behind this strategy is that for the economy to function optimally, banks must be healthy and profitable so they can continue to provide credit prudently and continuously to help support the economy’s needs so that it can grow and innovate. For this to occur, the yield curve should be positive for a large percentage of the time. Said differently, long-term interest rates need to be higher than short-term rates since banks pay depositors and holders of certificates of deposit based on short-term rates, and they then, in turn, lend out money to make longer-term loans based on long-term interest rates. This spread helps remain profitable, while an inverted yield curve can put pressure on the profitability of the banking sector.

I went back and looked at some interest rate statistics to see if this theory was correct, and I used two-time frames. The first was from 1990 to 2002 when rates were quite a bit higher, and then from 2003 to the present, when rates continued lower until late 2022 and 2023. I looked at daily closing yields for the 10-year Treasury Note and 3-month Treasury Bill for these time frames.

I used the 10-year as a proxy for the cost of 10-year fixed rate loans and the 3-month for the cost of floating rate loans. The assumption is that the spreads over the two indices were the same. It’s not a perfect assumption, particularly since our floating rate loans have been pegged to 30-day LIBOR and now SOFR, but for testing my hypothesis, it works just fine. The point is that if a positive yield curve is the most common state of affairs versus an inverted yield curve, then being a floating rate borrower should result in a lower cost of funds over the long term. So what does the data say? Here is the first table with the key data.

1990 – 2002

| Positive | Inverted | |

| # of Days | 3,136 | 116 |

| Percentage | 96.4% | 3.6% |

| Avg. 10-Year Yield | 6.36% | 5.62% |

| Avg. 3-Month Yield | 4.51% | 5.96% |

| Differential | 1.85% | -0.34% |

| Current 10-Year Yield | 3.45% | |

| Current 3-Month Yield | 5.21% | |

| Differential | -1.76% |

When it comes to this dataset, the results are overwhelmingly supportive of the hypothesis that a positive sloping yield curve is the default state for the economy as it was positive 96% of the time with an average spread between the 10-year and 3-month of 1.85%. In addition, during those rare times when the yield curve was inverted (approximately 4% of the time), it was only inverted by an average differential of -.34%. This provided a very asymmetric risk-reward relationship for floating rate borrowers in that when it was positive, it was positive for the vast majority of the time and with a much higher spread (1.85%) as compared to when it was inverted (-.34%).

The second dataset has very similar results, although, in the first one, the 10-year yield was higher when the curve was positive, while in the second one, the 10-year yield was lower when the curve was positive versus when it was inverted.

2003 – 5/5/23

| Positive | Inverted | |

| # of Days | 4,669 | 410 |

| Percentage | 91.9% | 8.1% |

| Avg. 10-Year Yield | 2.86% | 3.72% |

| Avg. 3-Month Yield | 1.01% | 4.16% |

| Differential | 1.85% | -0.44% |

| Current 10-Year Yield | 3.45% | |

| Current 3-Month Yield | 5.21% | |

| Differential | -1.76% |

Once again, the curve was overwhelmingly positive, with this being the case 92% of the time versus 8% when it was inverted. What’s fascinating to me is that in spite of the 10-year yield being much lower when the curve was positive (2.86% average) versus in the first dataset (6.36% average), the spread was still 1.85% between the 10-year and 3-month.

Here are a couple of takeaways. This dataset also had a very positive risk-reward relationship if you were a floating rate borrower. The 1.85% average spread has been in place approximately 92% of the time, while for the other 8%, it was only -.44%.

In addition, one can see what an incredible anomaly today’s inverted yield curve is and how it has to be a temporary phenomenon as this is not the natural state of affairs as it has not only wreaked havoc on the banking system with bank failures and deposit outflows to much higher yielding money market funds but will continue to do so as banking pressures continue to build as profitability is eroded, there is more pain on the horizon with office building loans defaulting, and credit will become harder to access.

This chart shows the performance of the Regional Banking Index (KRE), and it is down 44% over the last six months, reflecting investor concern about the profitability and risk profile of smaller banks.

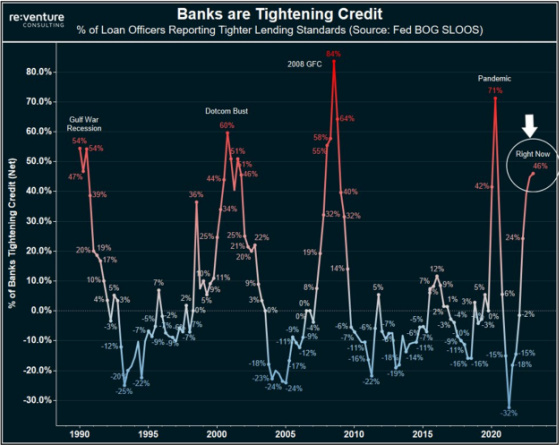

This is the quarterly Senior Loan Officer Opinion Survey carried out by the Federal Reserve. It uses these surveys to determine if credit conditions are tightening, loosening, or remaining the same. One can see that conditions have tightened quite a bit and will probably be a headwind for the economy.

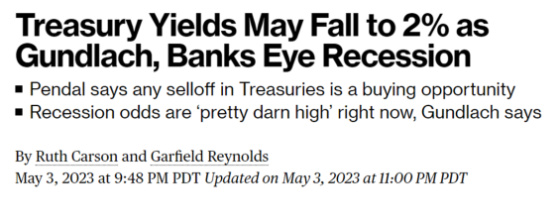

If one accepts that the 1.85% spread is a good rule of thumb for the differential between long rates and short rates and we also assume that the 10-year Treasury does not change such that all of the yield curve reversion to return to a positive 1.85% comes from falling short-term rates, then this would imply a future 3-month yield of approximately 1.60%. There are some outlier forecasts that 10-year Treasury Note yields could drop to 2% as this headline attests. If this were the case then short-term rates would go even lower.

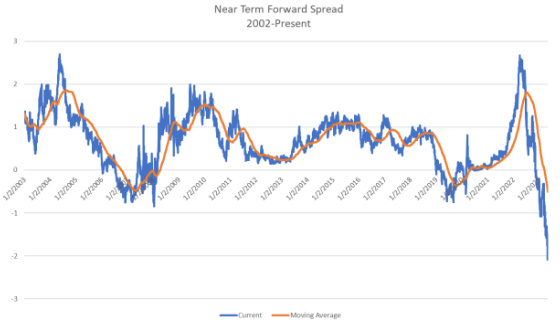

I’m not necessarily in this camp that long-term rates, and correspondingly short-term rates, will fall so significantly. The more important point I’m trying to convey is that while it’s very painful to be a variable rate borrower today, there is a plausible scenario that future short-term rates may be a lot lower over the next 2-3 years. In fact, the Fed’s favorite yield curve indicator to help determine if the market thinks the Fed is too accommodating or too restrictive is flashing a very concerning red signal that it is way too restrictive.

Source: www.neartermforwardspread.com

Powell used this indicator to justify raising rates when the more widely followed yield curve indicator, the differential in yields between 10 and 2-year Treasuries, was signaling worrying signs that Fed tightening could only go so far before hurting the economy. If he were intellectually honest, he would be hard-pressed to ignore this indicator suggesting the Fed is being much too restrictive.

Before wrapping up, I’ll reference a couple of charts calibrated from the conference calls management teams hold to discuss their earnings reports for S&P 500 companies as well as data related to wage growth and spending by income category.

The first earnings call chart relates to the average number of mentions of “weak demand” and other similar words or phrases. One can see it is at record levels which doesn’t bode well for corporate earnings.

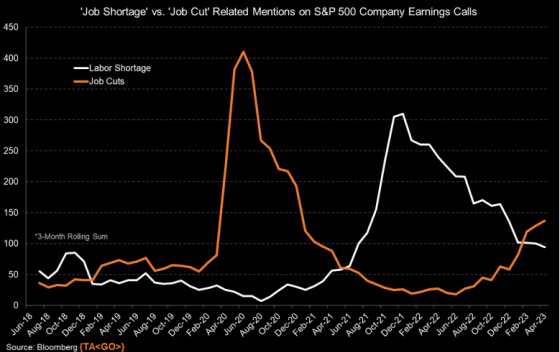

The second chart graphs the average number of mentions of “Job Shortage” vs. “Job Cut.” One can see that during the early phases of Covid, “Job Cuts” was mentioned far more than “Job Shortage.” This reversed fairly quickly, such that “Job Shortage” was mentioned far more than “Job Cuts” as the shortage of labor, particularly in the service sector, was particularly acute. The situation has now reverted back to “Job Cuts” now ahead of “Job or Labor Shortage,” although these levels are still above where they were pre-Covid.

With many of the job cuts coming among higher-paid, white-collar workers, one can see that their earnings and spending have been falling.

It appears we’re on the verge of a white-collar recession in which overall jobs may hold up but the buying power of those jobs eliminated may be quite significant, thereby masking the overall pain to the economy that continued job growth may suggest is healthy.

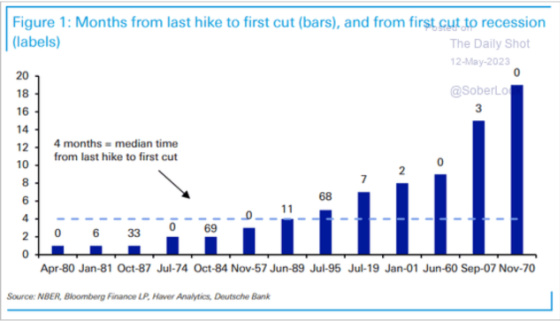

Finally, if we think the Fed has finally stopped raising rates for this cycle, then it’s helpful to see how quickly the Fed cut in past cycles. The average gap between the last Fed rate hike in a cycle and the first cut thereafter is about six months. The median gap is four months. Typically, rate cuts occur when a recession has already started or roughly three months afterward.

Yes, it’s been painful to be a variable rate borrower, but since we have utilized these loans in a very significant way over the last 12 years, we have benefitted immensely from having a lower cost of funds and much lower prepayment penalties than the fixed rate alternatives. In fact, during the last 10 years, we have prepaid 100 loans representing a principal amount of approximately $2.7 billion. This has allowed us to sell properties free and clear such that buyers did not have to assume our financing and enabled us not to have to limit our buyer pool. We also carried out a significant number of refinances that allowed us to extend our maturities, lengthen or commence interest-only periods, lower our spreads, and in many cases, return capital to our investors and improve our properties’ working capital positions.

With patience and financial and emotional fortitude, we should be very well positioned if the economy does weaken and the Fed is forced to cut rates quite substantially as the market is projecting.

{kind=link}

Leave a Reply