How Energy, Geopolitics, and Inflation Are Triggering a Global Market Chain Reaction

Financial markets have a long history of overreacting to geopolitical headlines and then quietly moving on. This time feels different. The recent surge in energy prices following events in Iran—coming on the heels of U.S. intervention in Venezuela—has triggered unusually broad market stress: collapsing Asian equities, rising long‑term interest rates, and renewed inflation anxiety.

What markets are confronting is not simply an oil shock. It is something more systemic—a China Syndrome—a chain reaction that begins with China’s energy dependence and radiates outward through inflation, capital markets, and global risk appetite.

The Trigger: Iran, Venezuela, and the Return of Energy Shock

At first glance, the market response looks familiar. Iran sits astride the Strait of Hormuz, through which roughly 20% of globally traded oil flows. Any threat—real or perceived—to that chokepoint creates a nonlinear price response. Energy‑importing economies react immediately, and equity markets wobble.

Venezuela, meanwhile, is no longer a swing producer. Yet its oil still matters. Venezuelan crude is heavy, scarce, and structurally important for certain refineries. More importantly, it had become a deeply discounted marginal barrel, flowing primarily to China through opaque arrangements designed to evade sanctions.

But this was not just a supply scare. It was the ignition point for a broader realization.

The Core of the China Syndrome: Subsidized Energy and Strategic Exposure

For years, China quietly absorbed the bulk of sanctioned oil from Iran and Venezuela, often at steep discounts. Independent “teapot” refineries, shadow fleets, ship‑to‑ship transfers, and barter‑based payment systems allowed these flows to continue largely outside Western financial channels.

Cheap energy acted as an implicit subsidy:

- Lower manufacturing input costs

- Improved export competitiveness

- A buffer against global inflation pressures

That system is now under direct pressure.

Recent U.S. actions suggest a strategic shift: not merely punishing bad actors, but targeting China’s access to subsidized energy itself. Expanded sanctions on Chinese refiners, intervention in Venezuela framed around limiting Chinese influence, and a higher tolerance for oil price volatility all point in the same direction.

This is where the China Syndrome begins: when a country that anchors global demand suddenly faces structurally higher energy costs, the shock does not stay contained.

Contagion Phase One: Asia Breaks First

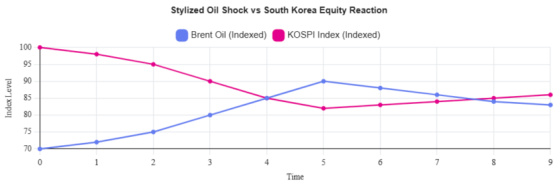

The first visible casualty of the China Syndrome was South Korea.

South Korea imports virtually all of its oil and a significant share of its liquefied natural gas, much of it sourced from the Middle East. Its equity market had also become one of the most crowded expressions of the global AI and semiconductor cycle.

When oil prices surged and shipping risk rose, global investors de‑risked immediately.

The result:

- The KOSPI fell more than 12% in a single session, the worst one‑day decline on record

- Semiconductor leaders Samsung Electronics and SK Hynix led the sell‑off

- The Korean won weakened sharply, amplifying equity losses

This was not panic. It was mechanical contagion high energy dependence meeting crowded positioning.

Chart 1: Oil Shock vs. Korean Equities (Stylized)

This stylized illustration shows the inverse relationship markets feared, rather than precise historical data.

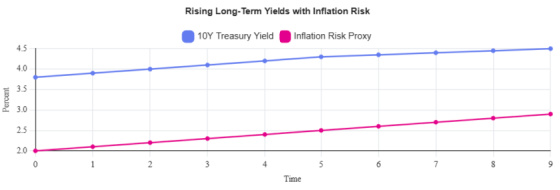

Contagion Phase Two: Inflation Re‑Prices the Bond Market

The most telling signal did not come from equities. It came from bonds.

Historically, geopolitical conflict produces a flight to safety, pushing long‑term yields lower. This time, long‑term Treasury yields rose.

The reason is central to the China Syndrome. Markets are no longer focused on recession risk; they are focused on persistent inflation risk driven by supply‑side stress.

Higher energy prices feed directly into:

- Transportation costs

- Industrial input prices

- Inflation expectations

Research from the Federal Reserve shows that recent increases in long‑term yields reflect higher perceived risk of future supply shocks and a rising term premium, not a loss of confidence in central banks. The Iran shock simply accelerated this repricing.

In other words, the bond market is signaling that energy‑driven inflation is no longer a transitory risk.

Chart 2: Long‑Term Yields and Inflation Risk (Illustrative)

Why Markets Are Uncomfortable—and Should Be

The China Syndrome is unsettling because it does not resemble a traditional crisis.

- There is no immediate supply collapse

- There is no single policy mistake

- There is no clear endpoint

Instead, there is a structural recalibration underway:

- Energy is being weaponized strategically

- China’s cost advantages are being challenged

- Inflation risk is being redistributed globally

Energy‑importing economies feel the pain first. Exporters benefit. Capital markets reprice uncertainty rather than fundamentals.

This is why volatility has risen faster than scarcity would justify. Markets are struggling to price intentional friction.

The Bigger Picture: A Market Priced by Strategy, Not Equilibrium

The China Syndrome is not about China alone. It is about what happens when the world’s largest marginal consumer of energy faces a structural shift in access and pricing.

Iran and Venezuela are not isolated events. They are pressure points. Oil is not just a commodity. It is a strategic lever.

Markets are not worried about running out of oil.

They are worried about a world where energy is priced by power rather than equilibrium.

That is a harder world to hedge—and a far more volatile one to invest in.

{kind=link}

Great read and extremely insightful. Our country needs more people who think like you and fewer of the ones actually supposed to be thinking right now.