Given China’s importance to the world economy, I wanted to focus this week’s post on some of the challenges China is facing in the short and long term.

China’s Economy

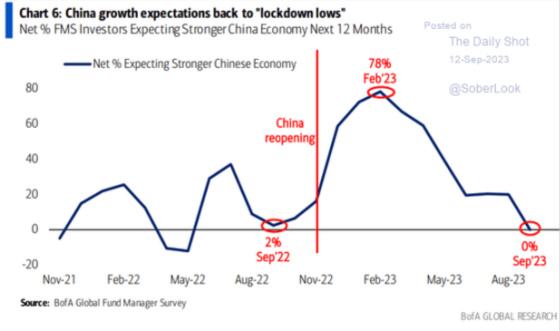

From an investor perspective, there is very little optimism that China’s economy will experience stronger growth after severely disappointing in the wake of its Covid reopening.

The Chinese currency has dropped quite significantly since early 2022 and is below the levels that it was at pre-Covid.

China’s Auto Industry

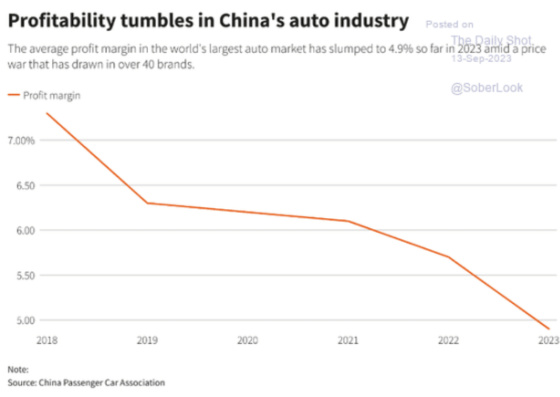

One bright spot for the Chinese economy is its auto sector and how strong its exports are, particularly EVs. This puts a lot of pressure on European car manufacturers and creates tension with Europe, especially Germany.

Like other industries (e.g., steel), China is using subsidies of its state-owned companies and favored industries to increase global market share at the expense of profitability, as this chart shows.

China’s Real Estate Collapse

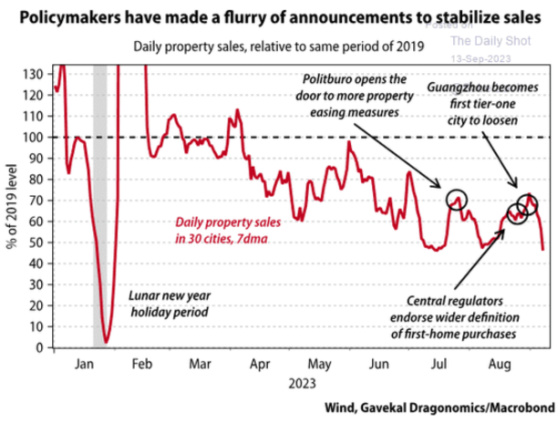

The biggest issue the Chinese economy (and society) faces is the collapse of real estate demand and prices and the financial distress of major developers, leading to massive defaults on their bonds. This puts financial pressure on Chinese households and consumers as their biggest financial asset depreciates in value. In addition, Chinese developers are forced to cut back, leading to layoffs in the construction center and putting more pressure on Chinese consumers, with weaker employment conditions hurting income growth and consumer confidence.

Except for the first half of 2023, home prices have declined since mid-2021, with the prospects of this reversing soon not looking very positive.

One can see how the market value of non-defaulted developer bonds has dropped significantly, with so many bonds having gone into default. This is a vivid depiction of the extraordinary financial distress Chinese developers have been experiencing.

And while the government has announced policies to help stimulate demand, one can see that the home sales volume still needs to reach 2019 levels.

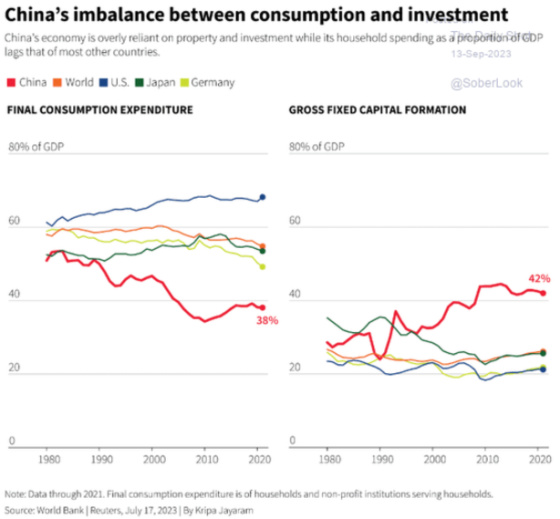

These charts show how reliant China’s economy is on investment compared to other major economies and how its share of consumption is so much lower than the rest of the world in general and the developed world specifically.

Beijing Based Economist – Michael Pettis

Michael Pettis is an economist based in Beijing who is one of the most thoughtful and insightful people when it comes to truly understanding the mechanics of the Chinese economy and its prospects. In a recent article he said that early on, when China started to open its economy after the reforms implemented by Deng Xiaoping and carried on by most of his successors, it made sense for China to focus on a development model by taking advantage of its huge labor force to become the factory to the world by heavily investing in infrastructure and export capacity. This was the fastest and most logical way for China to grow rapidly and improve its living standards.

To execute on this development model required suppressing consumer demand by focusing much more on exports than imports and domestic consumption, providing very little in terms of a social safety net for its citizens, keeping manufacturing wages low by incentivizing the movement of labor from rural areas to cities, directing subsidies to state-owned firms and targeted industries by providing preferential access to credit, underpricing loans, and keeping its exchange rate low to make its exports more cost competitive. The overarching goal was to create mammoth industries with extraordinarily cost-competitive export capacity benefiting from very little requirement for profitability and incredible infrastructure and logistics paid for by subsidies that no other economy in the world could match.

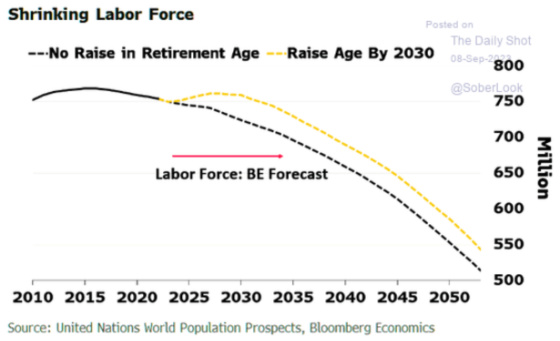

China is now in a very different position from where it was in 1985 when it first opened up and had been severely underinvested. China is no longer a developing economy.Click To TweetIt is a rapidly aging society with a labor force that will shrink significantly unless the retirement age is lifted. And even this will only delay the inevitable, as the following graph shows. The one-child policy did its job to stop China’s rapid population growth, but now it has created an irreversible population drop (collapse?) without a significant increase in immigration.

The last thing China needs is to build more high-speed rail capacity or housing. Xi has said that housing is not for speculation, and he has so far shown the will to cause significant pain in areas of the economy that he thinks have become too unbalanced and risk cutting into the Communist Party’s power and control or are sources of destabilizing inequality. This has also spooked investors and made China a much more risky place to invest, particularly when factoring in its saber-rattling regarding Taiwan.

Returning to Pettis is the conundrum created by China’s extraordinary reliance on investment.

China accounts for roughly 17 percent of the global economy but only about 12 percent of global consumption, with Chinese investment estimated to make up an astonishing 30 percent of the global total.

This clearly isn’t sustainable. As part of its gross domestic product, China’s investment level is already very high. If it wants to maintain this while still growing by 4-5 percent for the next decade, its share of global investment would have to rise to nearly 40 percent. In that case, to prevent a global demand crisis, the rest of the world would have to reduce their investment share to well under half of the Chinese level.

This is highly unlikely. The United States, Europe and India (along with many smaller economies) are all determined to implement policies that boost domestic investment and support domestic manufacturing. The world simply cannot sustain such high investment levels relative to demand.

With so much capital being directed to non-productive investments, the result has been a huge increase in debt, particularly by local governments that have had huge incentives to reach growth and investment targets set forth by Beijing, and the last thing local politicians want to do is fall short and upset the powers that be. In addition, investment spending provides a much greater opportunity for local politicians to profit from such spending through kickbacks and bribes, so shifting from a development model to a consumption-oriented one will be highly disruptive and less lucrative for an economy with so much graft.

So what is the unassailable math, according to Pettis? Advanced economies typically invest 23% to 24% of their GDP, while high-investment economies invest 30% to 33%. China currently invests an incredible and unsustainable 44%. Reducing its investment share to 30% to 33% (which still could be too high given its rapidly aging society) requires GDP growth to outpace investment growth by 2% to 3% per year over the next 10 years. This requires consumption growth to do all the heavy lifting, which would necessitate massive changes to government policies and culture to implement the changes necessary to make this happen. Consumption would need to increase from 4% growth per year to 6% to 7% to maintain GDP growth in the 4% to 5% range.

Reduced investment growth will result in lower demand for labor to build bridges, roads, rails, airports, etc. And transitioning to more of a consumer society cannot happen overnight. So what is the answer? According to Pettis, there is no way around government transfers.

If investment growth decelerates, Chinese consumption cannot accelerate without implicit or explicit transfers from elsewhere in the economy.

Businesses, for example, can be forced to fund these transfers by paying substantially higher wages, but with China’s manufacturing competitiveness based primarily on the very low share Chinese workers retain of total production, this would almost certainly undermine manufacturing exports, and would lead, in the short term, to a rise in unemployment which, paradoxically, would reduce consumption growth.

The only other way to fund the transfers is if Beijing and local governments were to partially liquidate their considerable assets in favour of Chinese households.

By my calculations, if the government could directly or indirectly transfer roughly 1.5 per cent of GDP every year to households, it could drive growth in household income – and with it, household consumption – to around 7 per cent annually. This, in turn, could generate GDP growth of 4-5 per cent even as investment growth dropped sharply.

But however difficult it might be, the arithmetic of rebalancing is unassailable. Given its status as the world’s second largest economy, and by far the world’s largest investor, China simply cannot maintain its current investment share of GDP while continuing to grow relative to the rest of the world.

That is why the growth rate of Chinese investment must decline, and by definition, this means that either consumption growth must rise sharply or GDP growth must drop sharply. The only way the former can happen requires major, and politically contentious, transfers from government to households. This won’t be easy, but the arithmetic of rebalancing allows no other option.

There’s a bit of a yin and yang associated with China’s rebalancing that, on balance, I think creates more global inflationary pressures. Its shrinking labor force and the tensions building between China and the West will presumably heighten inflationary pressures resulting from China not being nearly as cost-competitive as it was from a manufacturing standpoint. In addition, the reshoring of manufacturing that is taking place because of tensions with China will most likely amplify cost pressures as the U.S. economy, as well as European ones, will be challenged to find large numbers of quality, productive workers to fill these jobs while facing their own labor growth challenges as well as not having the infrastructure capacity and quality that China possesses to compete as effectively. Said differently, onshoring will probably create less productive manufacturing output than would be the case if it remained in China, and this will be more costly.

And if China does cut back on its investment growth, it could put downward pressure on commodity prices and lessen the cost of inputs for manufacturers and consumers. And yet, while China’s growing dominance in electric vehicles could lead to the adoption of EVs much more rapidly around the world (including China itself) and presumably reduce gasoline demand, it will also put pressure on electricity grids to keep this multitude of vehicles charged, even if they are plug-in hybrids. And since there is very little chance that renewables will sufficiently cover this enhanced demand for electricity because wind and solar don’t have the reliability that fossil fuels do, there could be upward pressure on natural gas and coal because they are highly reliable and exist in huge quantities.

Let’s also not forget that the cost to find, mine, and extract rare earth minerals for EVs is quite energy intensive, so this will offset some of the savings from lower oil and gas consumption. Finally, the massive manufacturing investments to power and supply semiconductor and EV batteries and other components with fully reliable 24/7 energy will also be massive.

There’s a lot to unpack here, and I won’t even pretend to know how this will play out. With that being said, China’s rebalancing requirement will be a material issue that will affect the global economy for the next decade and will be something I will be watching closely and thinking about in much greater depth, particularly as it applies to energy demand.

{kind=link}

Leave a Reply