I many times thought Peace had come

When Peace was far away—

As Wrecked Men—deem they sight the Land—

At Centre of the Sea—

And struggle slacker—but to prove

As hopelessly as I—

How many the fictitious Shores—

Before the Harbor be—

-Emily Dickinson

Every so often I will read poetry to tap into timeless thoughts and wisdom. Admittedly, much of what I read is beyond my comprehension or it just doesn’t resonate with me. Every so often, however, I will read a poem that really strikes a chord and resonates deeply. Sometimes they may be profoundly moving while other times they may generate an insight that provides me with clarity.

The poem cited above by Emily Dickinson is one that really hit home, as I think it has summed up the feelings of many apartment owners, particularly in 2025. While I have been in the camp that conditions would remain challenging through 2025, there was a side of me that felt like we would have turned the corner by now, which has not been the case. The poem is quite short but so succinct and effective at conveying the disappointment from misplaced hopes that keep getting dashed.

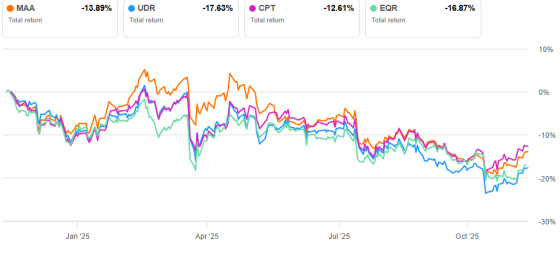

The following chart from Seeking Alpha shows the total return for four apartment REIT over the past year. One can see that investors have not been enamored by the apartment sector.

This contraction in values has taken place despite a more favorable interest rate environment as the 10-year Treasury yield has fallen by nearly 0.75% from its 2025 peak. This significant drop in long-term rates would usually lead to a pretty powerful rally in apartment REITs as this would lower their cost of capital and tend to lead to a drop in capitalization rates, which would push up values. And yet, this has not been the case, which suggests that investors are more concerned about operating cash flow weakening.

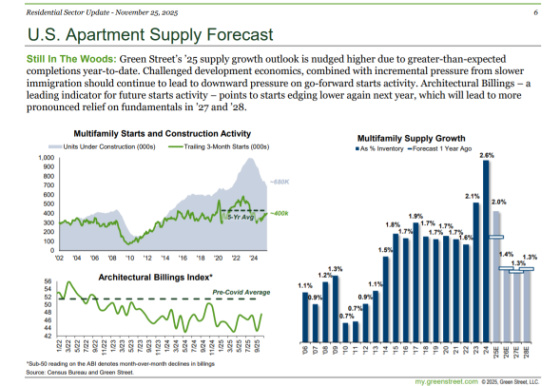

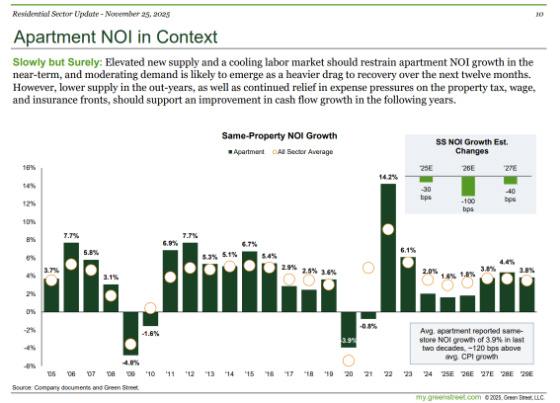

Green Street does a very good job of covering publicly traded real estate companies. Last week they released an update on the residential sector and they have trimmed their forecasts for apartment REITs. Here is a summary of their thoughts about apartment fundamentals.

It’s been clear to people who follow the apartment industry that new supply is contracting, which should set the stage for healthy apartment growth down the road. Unfortunately, similar to Emily Dickinson’s poem, the road seems to be extending and is taking longer and longer to get there.

One can see that after a huge increase in the number of units under construction, we’re seeing apartment starts come down to its historical level of around 400,000 units. And while this is a positive trend, my concern is that we may not be dropping fast enough and far enough.

Before I embark upon my back of the envelope analysis it’s important to remember that real estate investing is a local endeavor so these numbers can’t be applied to individual markets as they all have their own supply and demand relationships and initial conditions. On the other hand, by looking at these macro numbers it may help explain the weakness in apartment REITs and some of what we’re experiencing in our portfolio.

Real estate development is cyclical. It ebbs and flows based on the availability of capital, the perceived profitability of developing new communities, and interest rates. Of course there are other variables but generally if developers can convince equity capital that they can generate development returns that adequately compensate them for the risk and lenders are willing to extend construction financing, then builders will build because that is what they do. This leads to periods of over-building followed by a contraction in new starts, which then leads to not enough new supply to satisfy demand, which then restarts the development cycle.

When I eyeball the supply chart expressed as a percentage of the current apartment stock, it appears to me that a 1.5% annual growth rate is a decent approximation for equilibrium. Unfortunately, between 2023-25 we have overshot equilibrium by a cumulative 2.2%, which means we have to undershoot by this amount to regain balance. If we accept Green Street’s forecast for 2026-28 the cumulative undershoot is 0.5%, which still leaves a lot of excess supply to burn off.

Now, perhaps I’m being too conservative as the premium to buy a home is so significant that it is keeping people renting longer such that we may need more supply given that less people are leaving renting. Perhaps the 2015-22 numbers may be better to base our future projections on. If we take the higher end of that range then we’re at 1.8%. Let’s move it to 2.0% just for kicks. If this is the new equilibrium, which is a bit of a leap of faith, then we are only overbuilt by 0.7%, which would be close to being overcome over the next three years if Green Street’s supply forecast holds.

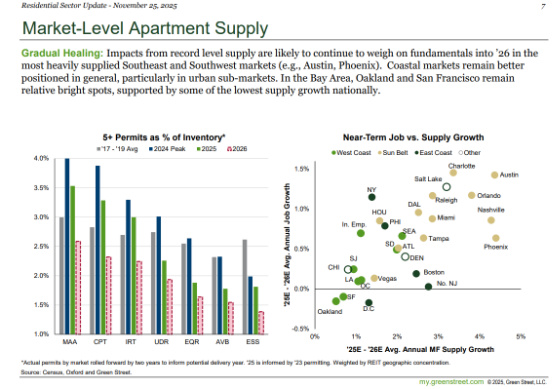

As I mentioned earlier, all real estate is local so I found this information quite interesting to show how some of the REITs Green Street covers is contending with supply in their portfolio as well as how each of the major MSAs are faring relative to their forecasted job growth.

Many of these REITs operate in faster-growing areas, so it would be expected to see their supply growth exceed 1.5%. If we peg equilibrium for these markets at 2.5% then they start to approach that level and below in 2026 but they still have more ground to be gained to make up for the significant supply growth that took place between 2023 and 2025. In general it looks like that 2027 will be the year when their pricing power should start to pick up and gain strength in 2028 as this chart shows.

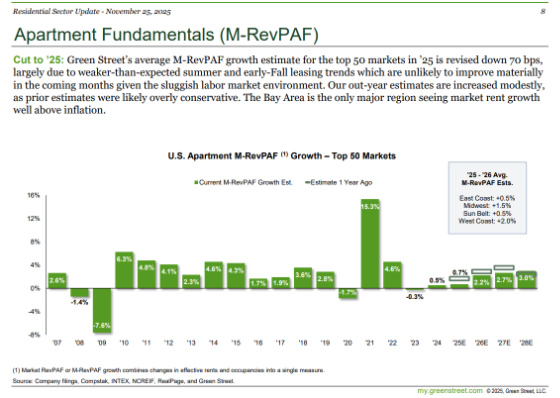

Between 2007 and 2020 average revenue growth was 2.00%. With Covid, however, apartment rents spiked at an unprecedented level such that revenue growth between 2021-22 averaged nearly 10% which was clearly unsustainable based on historical trends and led to the massive supply response from developers. If we pull out the Great Financial Crisis as a once in a lifetime outlier then the rate of growth moves up to 2.66%, which feels more realistic for our back of the envelope approach.

Simplistically, the growth between 2021 and 2022 represented approximately five years of excess revenue growth. If one believes in regression to the mean to get back to the 2.66% trend between 2025 and 2030 then revenue growth would need to drop to an average of 1.17% per year, which is quite a bit less than Green Street’s forecast. This is probably too conservative as it looks like we should have apartment markets be much more in balance in 2027 and 2028.

And while I may be too conservative in this approach I think it’s important to have a framework to put where we are in some sort of historical context so that we can have some perspective when underwriting new investments as well as budgeting for the properties we own.

If one is contending with negative cash flow, loans maturing over the next two years, or a combination of both, an owner without financial and emotional staying power will be very challenged to hang on to their properties if my back of the envelope numbers are in the range of what happens. We are already seeing some forced sales in the marketplace but my sense is that we are going to see a lot more in 2026 as sponsors reach the end of their rope and can no longer support their properties or fully repay their loans when they come due.

Green Street believes that apartment owners will be able to bring more of their revenue growth to the bottom line as cost pressures subside over the next few years.

I think that if one has access to capital, remains ruthlessly disciplined in the parameters one uses to underwrite properties (e.g. significant discount to replace cost, positive leverage, muted revenue growth for the first couple of years, well capitalized, etc.) and the locations where one purchases, then the opportunities to deploy capital in selective multifamily investments over the next couple of years may be very rewarding.

One never wants to rely on hope as a strategy. Rather, one should endeavor to have the wherewithal to ride out a difficult cycle and prosper from those who have nothing but hope as their strategy. As they find themselves short of capital to support their properties, and reality trumps hope, they will be forced to relinquish their apartment communities, either to the market at compelling prices or to their lenders who may ultimately do the same.

And while at CWS we are not immune to our own set of challenges, they are less numerous than those sponsors who loaded up on very high priced acquisitions in 2021 and 2022 with high leverage as well as developers who are completing their lease ups at rents and yields on cost far less than projected. We are working intently on putting ourselves in a position to effectively deploy capital to acquire apartment communities at compelling prices and a margin of safety, such that if my back of the envelope numbers pan out, we should still be in good shape from a capital preservation perspective. And if my approach is too conservative then we should be well compensated.

In the end my goal is that if Emily Dickinson’s shores remain fictitious, we can still succeed, and if they are truly in sight, then we can reach them safely and prosperously.

{kind=link}

Leave a Reply