It’s been awhile since I have had a blog post with a lot of charts and graphs. This is largely because my typical source for these, www.thedailyshot, had been off line for a long period of time. Unfortunately, the person who created it and kept it going had a severe medical issue that almost cost him his life. Thankfully, he has seemingly made it through the worst part and is on the mend. It turns out that he was planning on retiring within a year and was working with a group to take it over. With his medical issues, however, he was unable to keep the Daily Shot going so there was a pause and it also expedited the sale to the new owners that had been in the works. In the interim, his wife kept subscribers up to date about his condition and the transition to the new owners, which has now taken place. I now have a potpourri of graphs to access for future posts, as well as this one.

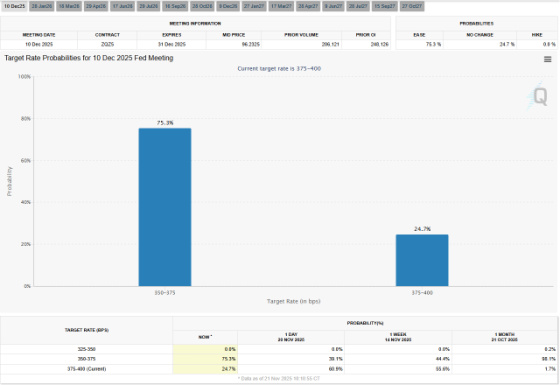

It’s fascinating how one comment from a Federal Reserve member can dramatically change the percentage chances of a rate cut at the December meeting. One can see how one month ago, there was a 98% chance that the Fed would cut in December. And then after the Fed cut rates by 0.25% at its last meeting, Chairman Jerome Powell said during his press conference that a December rate cut “was not a foregone conclusion.” The market then dramatically lowered the chances of a rate cut to only 39% as of last Thursday.

Everything changed on Friday when New York Federal Reserve Bank President John Williams said he saw room to lower rates again “in the near term” as the labor market softens.

Williams’ comments were particularly influential because:

- His position matters: Williams is vice-chair of the Fed’s rate-setting committee Axios, making him part of the Fed’s leadership alongside Chair Jerome Powell.

- He emphasized labor market concerns: Williams said downside risks to employment have increased while upside risks to inflation have eased Bloomberg, signaling he’s more worried about job market weakness than persistent inflation.

- He sees policy as still restrictive: Williams described monetary policy as “modestly restrictive, although somewhat less so than before our recent actions” Yahoo Finance, suggesting room for further cuts without overheating the economy.

This marks a sharp turnaround from just days ago, when Fed meeting minutes released Wednesday showed several officials were against lowering rates, and expectations for a December cut had fallen dramatically. Williams’ dovish stance has essentially put a December rate cut back on the table with the market now pricing in a 75% chance of a rate cut.

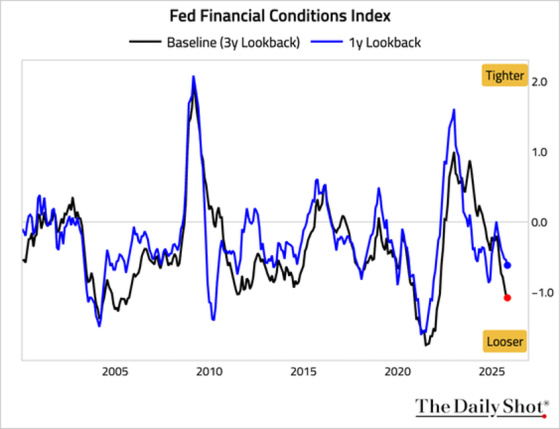

There is a cohort who believes that the Fed risks reigniting inflation as it’s cutting when inflationary conditions are still challenging and financial conditions are quite loose, as this chart shows.

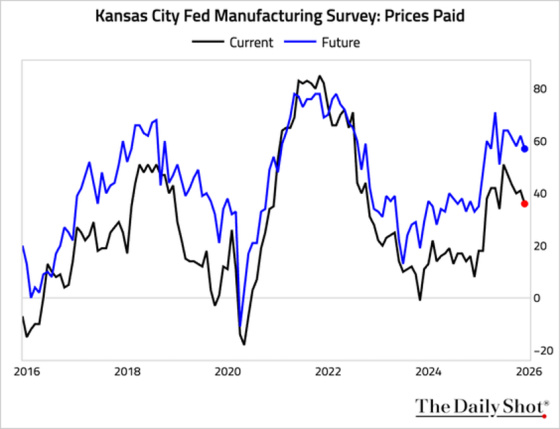

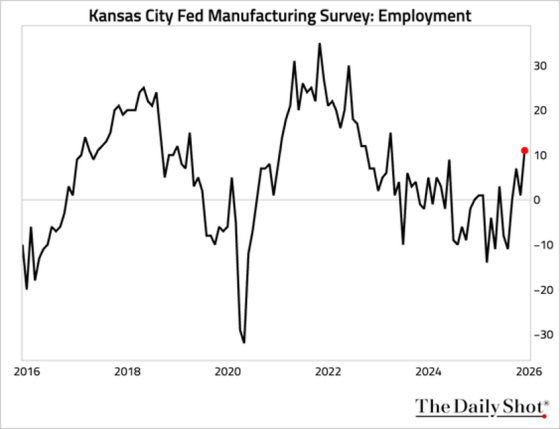

To highlight some of the inflation pressures still present in the economy, what follows are two charts showing the Prices Paid indices for the Philadelphia and Kansas City Fed Manufacturing Indexes. The Philadelphia index is still elevated and may be reaccelerating, whereas the Kansas City Prices Paid Index is less elevated and rolling over. From Williams’ comments, he is seemingly in the camp that the Kansas City Fed’s index is more representative of the inflationary trends in the economy.

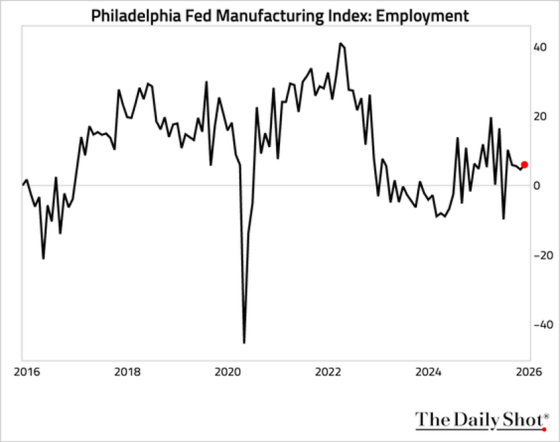

And yet, contrary to Williams’ concerns about the weakening labor market, the Employment Index for both Philadelphia and Kansas City are positive, with the latter accelerating.

Philadelphia looks like stagflation, while Kansas City is goldilocks.

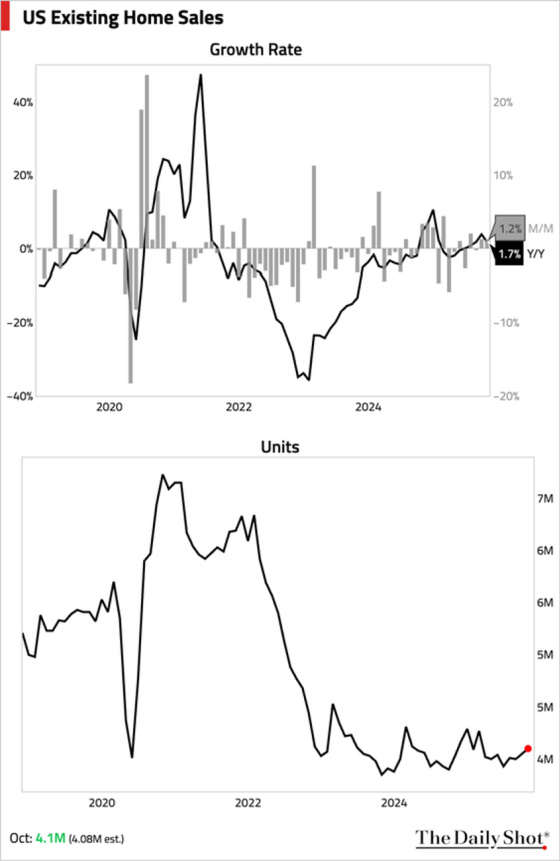

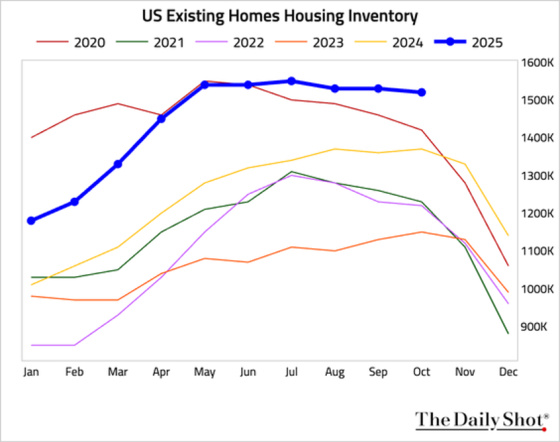

One of the overall challenges to the economy is the very soft housing market. One can see that existing home sales are quite anemic.

We are now at the point where there is more inventory as homes take longer to sell, and the lock-in effect of people not wanting to give up their low-interest-rate mortgages is becoming a little less pronounced as time goes by.

Home Depot’s earnings report from last week highlighted the weak state of the housing market and consumer confidence.

The stock fell by approximately 8% after the earnings were announced, knocking approximately $25 billion off of its market capitalization.

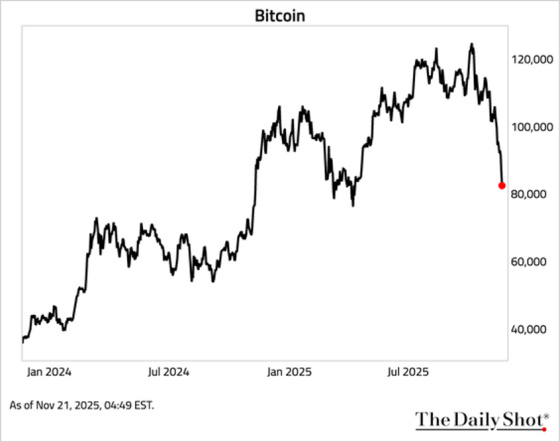

Finally, if we add to the mix the very significant NASDAQ selloff related to concerns that A.I. spending is an unsustainable bubble and that valuations have gotten way out of whack, we may have another catalyst for slower economic growth. Namely, slower spending in the A.I. space as well as a dent in consumer confidence from the significant stock market pullback as well as in bitcoin and the crypto space.

Here is a chart showing the brutal drawdown in Bitcoin, which is a risk-off signal.

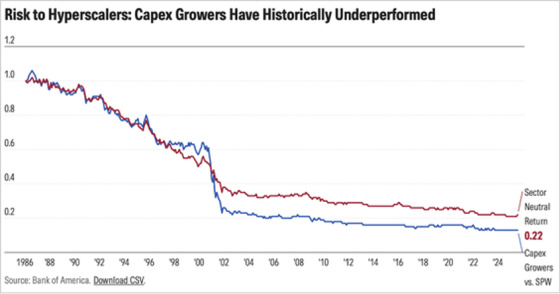

There are a lot of studies that conclude that companies that overinvest in growth via excess capital spending underperform over time as they rarely earn accretive marginal returns on those investment dollars. Investors don’t like empire builders. There is a risk that this will apply to the A.I. hyperscalers which may lead to a pullback in capital spending.

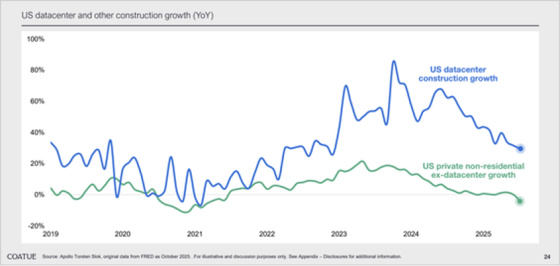

Construction spending related to data centers is still quite high, but its rate of growth is slowing fairly significantly. At the same time, non-datacenter construction spending is showing no growth.

As usual, there are a lot of cross currents in the economy which I still think will result in another rate cut for December.

I will end this post by reposting a Tweet from one of my favorite people on X, EndGame Macro, who I think sums up the Fed’s dilemma in having to manage the various cross-currents with great insight.

The Market Just Told the Fed That They’re Out of Time

The jump from 28% to 71% odds of a December rate cut is the market admitting the slowdown is becoming too obvious to ignore. When cut probabilities move that sharply in a single day, it’s never about one number. It’s about the direction the data is moving…labor softening, cracks in spending, credit tightening, and a tone from the Fed that suddenly feels a little less confident.

Markets don’t behave like this when things are stable. They behave like this when they sense the Fed is losing the luxury of patience.

A Rate Cut Isn’t the Fix People Think It Is

Even if the Fed cuts and the odds now say that’s increasingly likely it won’t solve what’s happening beneath the surface. Cuts this late in the cycle are almost always reactive. They happen because the slowdown is already pressing in, not because the Fed wants to juice growth or save markets.

A 25bp cut doesn’t make banks lend again.

It doesn’t reverse rising delinquencies.

It doesn’t revive margins or undo two years of rate pressure on households and small businesses.

Cuts don’t turn a deteriorating economy into a healthy one. They simply acknowledge that the deterioration is real.

What the Fed Says vs. What the Fed Is Managing

The Fed has to speak in a certain tone. They need to sound measured, in control, focused on inflation, focused on credibility. But anyone who watches them closely knows that the public script is never the full story.

Behind the curtain, they’re juggling things they can’t say out loud…geopolitical pressure, global dollar funding, fiscal stress, the softening in labor, and the slow grind of higher rates filtering through the real economy. Inflation was their headline concern, but forward looking inflation isn’t the constraint anymore…growth is.

That’s why ending QT on December 1st matters. That’s why two straight cuts matter. Those are big moves dressed up in calm language. Ending QT is the balance sheet version of easing. You don’t hit the brakes on tightening unless you’re worried the financial system or the economy is getting brittle.

The Fed may not want to cut in December, but the market is signaling that they may not have the option.

Where This Really Leaves Us

The Fed would love to engineer a clean landing. They’d like inflation to drift gently lower, hiring to stay soft but stable, and the economy to cool without actually slowing. But the data isn’t cooperating. The landing is wobbling. And once the underlying economy weakens enough, cuts aren’t a choice, they’re the path of least regret. A cut won’t save the cycle. It will simply mark the moment the Fed stops pretending the old script still fits.

{kind=link}

Leave a Reply