Fed Chairman Jerome Powell gave his annual Jackson Hole address last week. It’s almost assuredly his last one and is a fitting end to his tenure as it remained consistent with his personality and approach which is to be measured and flexible versus narcissistic and dogmatic.

Here is my Copilot prompt for this week’s blog post:

I want to write a blog post that highlights the most market moving parts of Fed Chairman Jerome Powell’s speech today at the Jackson Hole conference. Can you also incorporate an analysis about what key indicators investors should be focused on in terms of forecasting future short term rates and how the market is now pricing in future rate cuts after his speech?

Powell’s Final Jackson Hole Speech: What Moved the Markets and What Comes Next

In what was likely his final appearance as Fed Chair at the Jackson Hole Economic Symposium, Jerome Powell delivered a speech that was both measured and revealing. While he avoided dramatic shifts in tone, several key takeaways sent ripples through financial markets and reshaped expectations for the path of short-term interest rates.

🔑 Key Market-Moving Highlights

- Hints at Policy Adjustments

Powell signaled that the Fed may consider “policy adjustments” in the coming months, a subtle but meaningful shift from prior language that emphasized patience and data-dependence [1]. - Inflation Risks from Structural Forces

He warned that U.S. tariffs and tighter immigration policies could contribute to persistent inflation by slowing labor force growth. This was a notable acknowledgment of supply-side constraints that may keep inflation elevated even as demand cools [1]. - Framework Shift: Goodbye to the ‘Makeup’ Strategy

Powell announced the Fed would abandon its “makeup” strategy—where it allowed inflation to run above 2% to compensate for past shortfalls. Instead, the Fed will adopt a more flexible inflation-targeting framework, aiming for a balanced approach when its dual mandates (employment and price stability) are in tension [2].

📉 Market Reaction: Futures Reprice the Path of Rates

Markets responded swiftly as the immediate drop in 2-year Treasury yields shows.

Fed Funds futures began pricing in a higher probability of rate cuts beginning in Q2 2026, with the implied terminal rate now seen peaking slightly lower than before the speech. The yield curve steepened modestly, and the dollar weakened against major currencies, reflecting expectations of a more dovish tilt.

🔍 What Investors Should Watch Next

To forecast the Fed’s next moves, investors should focus on the following indicators:

- Core PCE Inflation: Still the Fed’s preferred gauge. A sustained move below 2.5% could open the door to cuts.

- Labor Market Participation: Powell’s concern about immigration and labor supply suggests the Fed is watching participation rates closely.

- Wage Growth vs. Productivity: If wage gains outpace productivity, inflationary pressures may persist.

- Global Supply Chain Metrics: Tariff-related disruptions could feed into inflation expectations.

- FedSpeak and Dot Plot Updates: Any shift in tone from other FOMC members or changes in the Summary of Economic Projections will be critical.

🧠 Final Thoughts

Powell’s speech was a masterclass in central bank signaling—subtle, data-aware, and forward-looking. While he didn’t declare victory over inflation, he laid the groundwork for a more flexible and responsive Fed. For investors, the message was clear: the path to rate cuts is open, but it will be paved by data, not declarations.

References

[1] Jerome Powell Jackson Hole Speech 2025: Key takeaways from Fed … – Mint

[2] Powell speech at Jackson Hole Symposium, key takeaways

As I stated last week, a 25 basis point cut is fully baked in for the September 17th meeting with an 84% probability, while the chances of a second rate cut for October 29th is now only at 43%. This can turn on a dime, however, particularly if the next employment report comes in materially weaker than expected. It does seem clear that the Fed is now weighing the risks to the labor market more highly than the inflationary impact of tariffs, although the latter still makes the Fed quite uncomfortable.

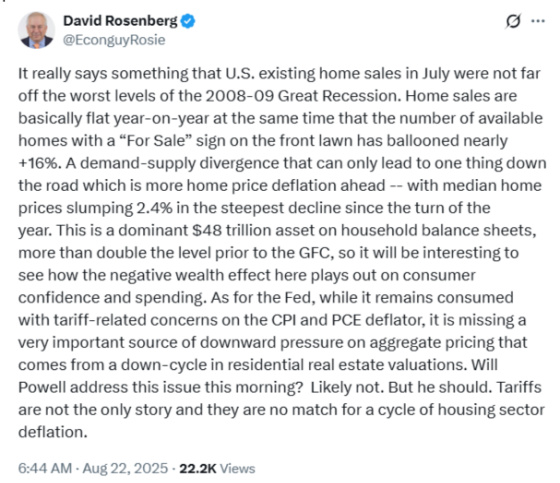

I do think the Fed is also underestimating the impact that a weakening housing market can have on the economy and jobs as this post from David Rosenberg on X highlights.

I’m off to NYC this week to attend the U.S. Open and to see a new play my daughter has written that she is also directing and acting in. I’m really proud of her and I can’t wait to see her latest creation.

{kind=link}

I seriously question the decisions made by Powell et al. The most recent inflation cycle was driven by a dramatic decrease in the goods and services available in the economy as opposed to a sudden increase in demand. Producers and logistic suppliers suddenly lost the manpower required to sustain the pre-covid level. Consumers did decrease their overall demand but were also provided an enormous amount of relief assistance cash — much of which went to families that didn’t need it. When consumers returned to their more normal spending habits the providers weren’t ready to provide it.

Raising interest rates was not an appropriate tool to deal with this inflation cycle. It’s likely that the best Fed policy would have been to refrain from doing anything. As workers got healthy and returned to work, the production and logistic issues started to recede. The recovery didn’t require added capital. The infrastructure was adequate.

The most significant impact of the increased interest rates was on the housing market. The rise in interest rates has led to a lot of unnecessary turmoil.

I am not going to applaud Powell. Let’s not be fooled! The administration and Fed combined to follow a set of policies based on false assumptions.

I do suspect that Powell is correct in his pronouncements regarding an adverse impact of the Trump tariff policies. But I am reasonably certain that the actual tariff’s applied will be less than often asserted. Some tariff’s are often not actually applied and there are also many routes to avoid them.

The Fed’s hard target of reaching 2% inflation was probably not warranted. The U.S. economy did just fine for many previous years with an inflation rate of 2.5% to 3%

Chuck Bohle

Rancho Bernardo