Fed Chairman Jay Powell spoke last Friday at the Jackson Hole conference for Central Bankers. He was pretty clear that the Fed would remain vigilant in its fight against inflation.

The economy is doing better than the Fed expected, so he is concerned that this could make the Fed’s efforts to bring down inflation to its 2% target and keep it there more difficult. The market seemed to take Powell at his word as the 2-year Treasury, considered to be the most sensitive bond to Fed policy, moved higher and, like the 10-year did last week, breached this cycle’s high.

Part of the reason rates may have moved higher is that Powell showed no willingness to raise the inflation target above 2%.

There is definitely a tug-of-war between the restricting effects of higher rates and continued strong fiscal stimulus and investments related to the reshoring of manufacturing and clean energy investments.

One can see that, even prior to revisions, job growth has been trending down, and it’s now even more so after the jobs numbers were revised last week, although not materially different.

The labor market looks like it might be on the precipice of softness as continuing claims for unemployment benefits are higher than the Covid-excluded averages.

In addition, more states are reporting a sharp rise in unemployment claims, and the trend seems to follow past cycles that were precursors to recessions.

An index of active jobs has been dropping quite significantly, and this will most likely result in fewer job openings as tracked by the government, which will most likely result in softer employment growth.

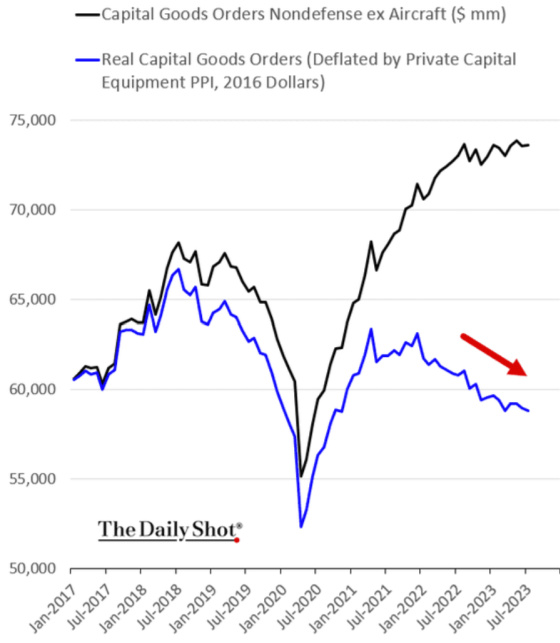

Inflation-adjusted capital goods investment has been falling as well, which is consistent with weakening conditions in the manufacturing sector, excluding investment in new plants.

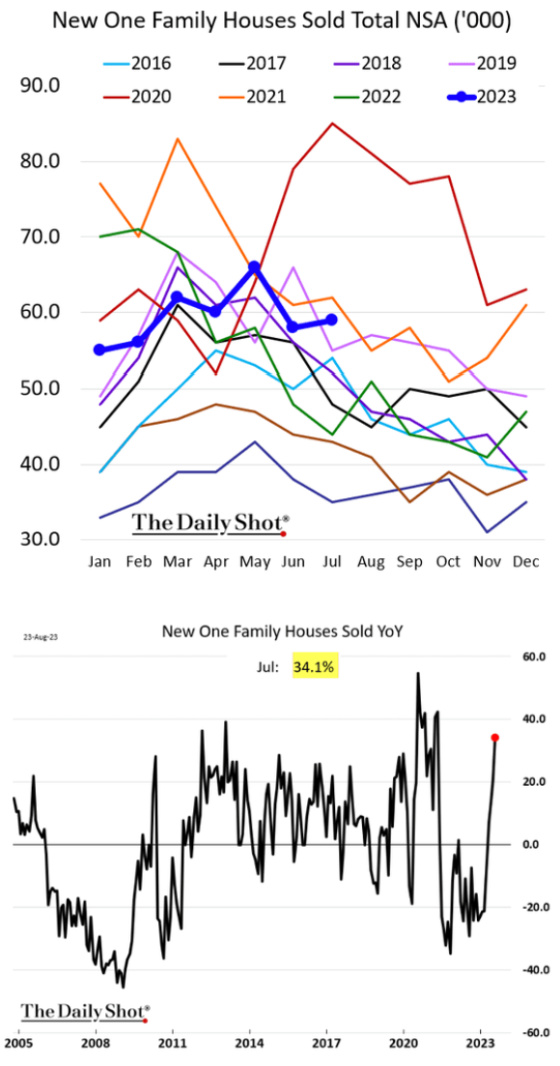

Existing home sales have collapsed as so few buyers are willing or in a position to sell and give up their below-market mortgages to buy homes at prices that have not adjusted for higher rates while then being required to finance their purchases at these higher rates.

Not surprisingly, very few people are locking in rates to access financing to purchase homes.

Because home builders are in the business of selling homes, they can do creative things to make purchasing homes more affordable to move their inventory. That is not the same with individual homeowners in whose home is often their biggest financial asset. Thus, every dollar counts for them, so they can’t be as creative and as financially flexible as builders. From a home builder’s perspective, the most powerful lever is buying down the interest rate to make the monthly payment more affordable. With so few existing homes for sale, new homes are the only meaningful source of supply, and sales of new homes are reflecting this.

And while manufacturing investment is definitely quite strong, as I will show shortly, consumer demand is softening, which is filtering down into the manufacturing sector as well.

The Purchasing Managers Index related to manufacturing remains in contraction territory (any reading under 50).

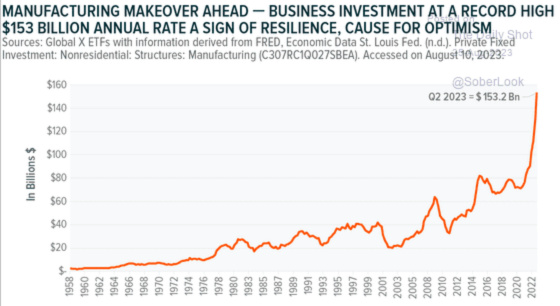

Manufacturing investment, on the other hand, has been growing sharply, with major investments being made related to the EV supply chain and semiconductors.

There is a legitimate question as to the wage/inflationary impact of filling the jobs that come with these investments given the aging labor force and relatively tight labor market. And when you add in other factors I mentioned last week like decoupling from China, China’s weakening economy and shrinking labor force, shrinking populations in Europe, green energy transition, climate impact, etc. there are countervailing forces that are going against the grain of Fed tightening. For these reasons the market has come around to believing Jay Powell that he has no intention of cutting rates any time soon and may leave them at these restrictive levels for a while.

The question is, will the toll that higher rates take on the economy be enough to offset the fiscal spending to bring the slowing, and even contraction, that is necessary to lower rates such that the yield curve becomes positive again much more from lower short-term rates versus long rates increasing much more than short-term rates come down? I’m in the former camp, but the question is, how long will it take? I know that was a mouthful, so I better leave it there.

{kind=link}

Seems very clear there is a housing bubble that will roll-over, just a matter of time, best case scenario is housing prices stay flat for many years, but not probable. When you hear, “it’s different this time,” that’s when you know it’s probably not, same long-term result, housing prices and affordability are scary right now. Example, a Buyer trying to buy a home in OC at $1.3 purchase, 20% down is $260,000, plus required reserves means they would have to manage to save about $300k to take on a house payment that is about $7k a month PITI, that’s not sustainable. Sure you could put 10% down and have even a higher payment with mortgage insurance tacked-on, which will put the payment approaching $8k a month. When the numbers don’t make sense, they don’t make sense.

Pre-Covid that would of required 30% less cash and payment would have been half that because of combination of prices, time to take the money and run. Hang in there Gary.