I’m going to breeze through a number of tweets and charts as I’m headed to watch the semi-finals and finals of the tennis matches at Indian Wells. The weather is going to be outstanding, and the matches have a similar promise.

The collapse of Silicon Valley Bank, Republic Bank, and the $30 billion infusion of deposits by major banks into First Republic were clearly huge events. The natural question is whether these were isolated, containable problems, or if they were just the canary in the coal mine and they were the first ones exposed or their rescues will unleash more problems.

Nassim Taleb is a famous author, philosopher, and investor who wrote The Black Swan, Skin in the Game, and Antifragile, three very influential and successful books. This is what he tweeted about past financial crises to put what we’re going through in perspective.

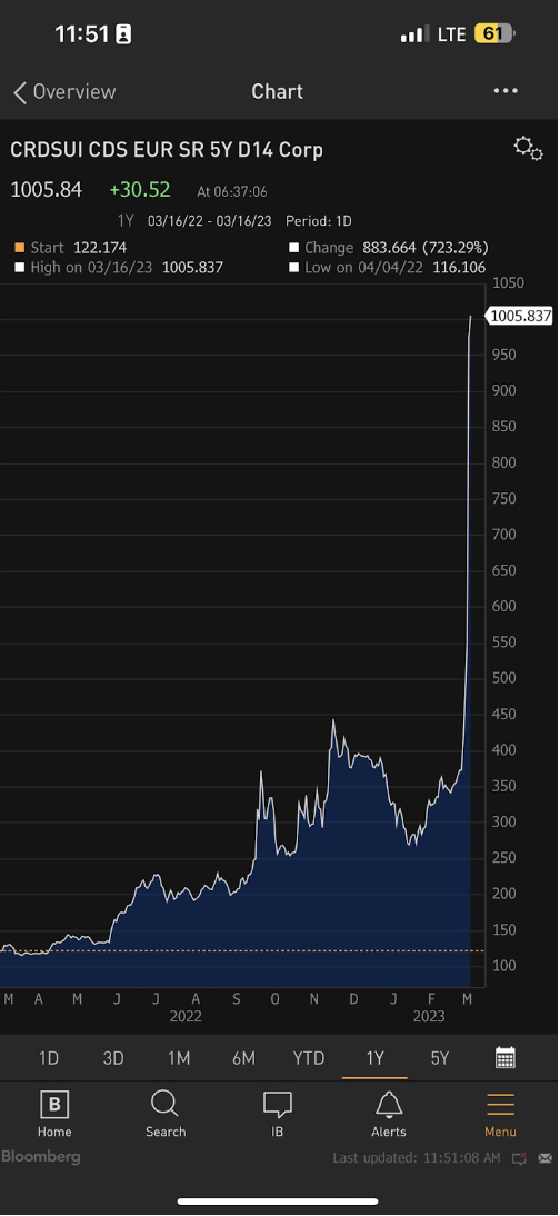

Banking problems are not confined to the United States as Credit Suisse’s problems finally came to a head such that it had to borrow over $50 billion from the Swiss central bank. Despite this lifeline, the cost to insure against Credit Suisse defaulting on its bonds has skyrocketed.

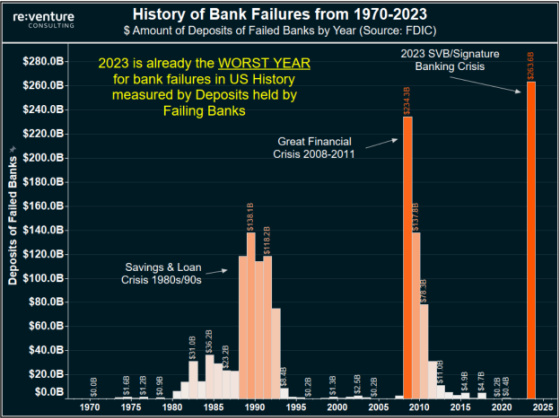

This chart puts the most recent bank failures in perspective. Similar to another chart I’m going to show later, the banking system is much bigger today, so as a percentage of deposits, it’s not at previous levels.

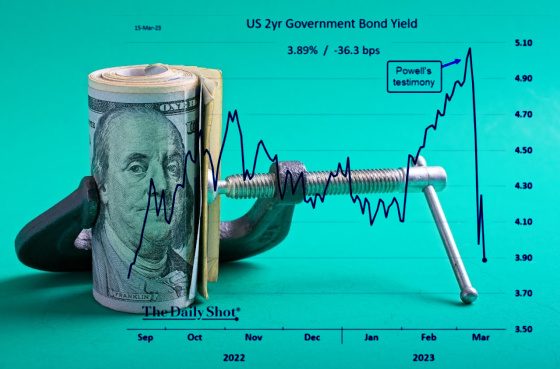

If the 2-year Treasury yield is any indication, then the market is pricing in the end of Fed tightening.

Ok, so the 2-year dropped a lot. Is this drop and overall movement in 2-year yields really that much out of the norm? According to this tweet, it should have been statistically impossible.

Does the move in the 2-year yield signal a regime change in monetary policy? History suggests it does.

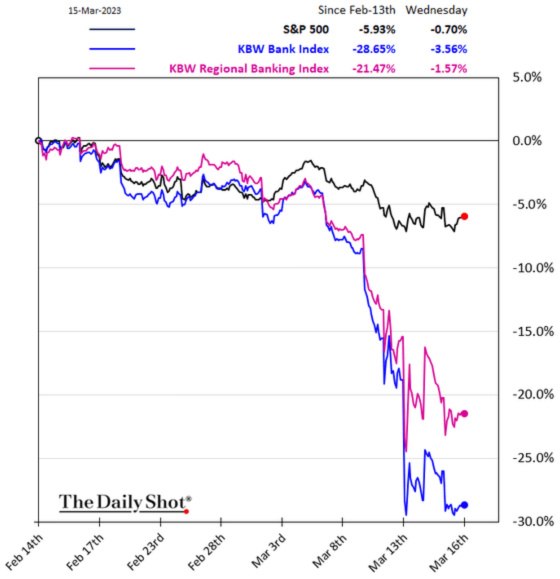

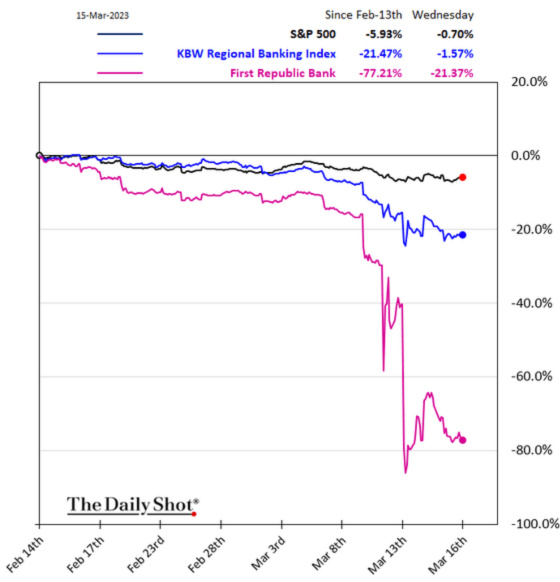

It’s never good when the banking sector underperforms very badly as it can be an indicator of financial stress and tighter credit, neither of which are good for economic growth. These charts show how banking stocks have greatly underperformed the market, especially First Republic Bank, which investors had been pricing in a meaningful chance of it having to recapitalize with significant dilution to shareholders.

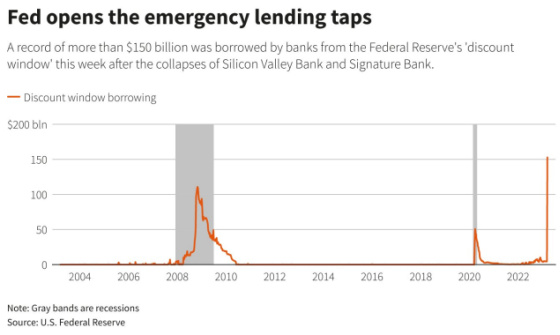

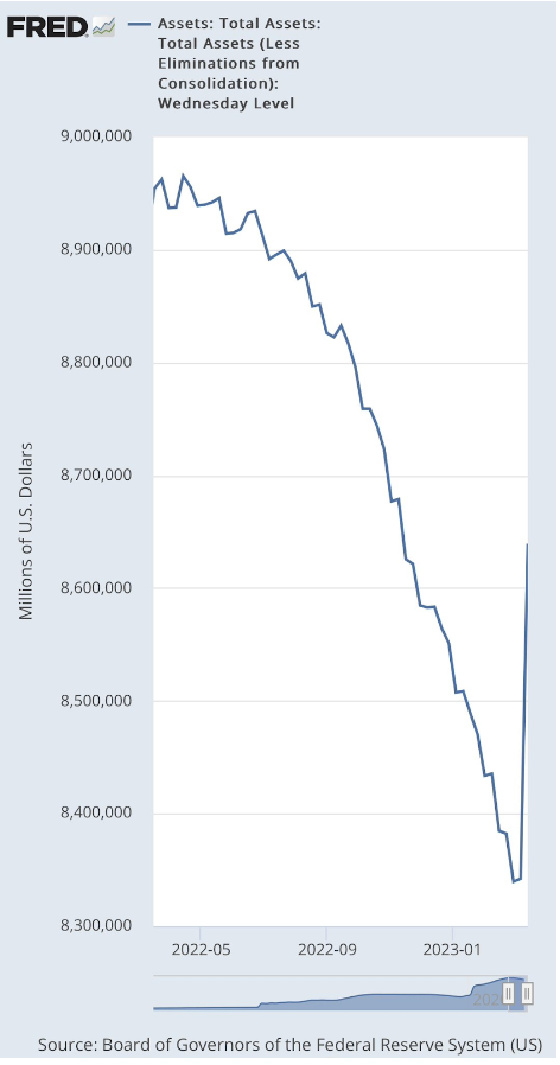

Banks facing huge outflows of deposits had to turn to the Federal Reserve’s discount window to make up for reserve shortfall. Similar to the earlier chart, this one shows that the amount borrowed exceeded 2008, although deposits are much higher today than they were then.

Tapping the Fed has resulted in the first reversal of quantitative tightening.

Morgan Stanley sees the ripple effects of these problems as being negative for the economy as it believes that banks will be faced with higher funding costs which will tighten lending standards and slow down credit creation.

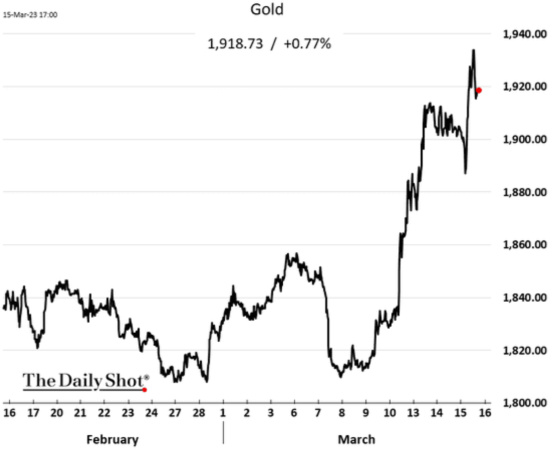

Gold has served as a port in the storm during this volatile period.

Morgan Stanley’s concerns about economic growth slowing due to the banking problems seem to only be corroborating what other indicators have already been showing.

The Philly Fed Manufacturing Business Outlook has historically been a good barometer of future economic conditions. Unfortunately, like the U.S. Leading Economic Index, it, too, is signaling the potential for an economic downturn.

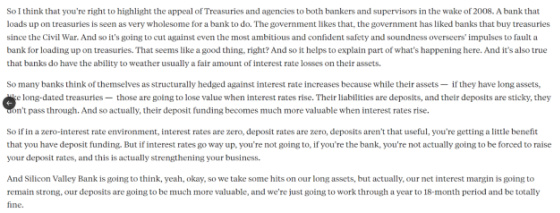

The following excerpt from an interview with a Columbia University professor is a perfect example of the law of unintended consequences. In the aftermath of the Great Financial Crisis, Congress and banking regulators understandably wanted to penalize banks for making risky loans and securities purchases and incentivize owning ultra-safe Treasuries and mortgage-backed securities guaranteed by Fannie Mae and Freddie Mac. As banks became flooded with deposits after huge fiscal and monetary stimulus in the wake of Covid, banks had to find a home for this money. Given the uncertainty during Covid, most people were happy just to keep their money safe even if they weren’t earning any interest. Believing that these deposits would remain in their banks for a long time, management teams felt comfortable investing in long-duration, risk-free Treasuries and mortgage-backed securities. Yes, they might lose value if interest rates rose, but as long as they hold them to maturity, they will get all of their money back. All of this is fine as long as deposits are sticky and growing, and they can reinvest growing deposits at the higher rates in the market while waiting for their long-dated securities to mature.

Finally, even prior to the banking problems arising, higher interest rates were already slowing down real estate transactions quite dramatically. One has to think that with community and regional banks at risk of deposit outflows that these banks, many of whom fund apartment developers, will be much more conservative when underwriting construction loans. As a result, development projects, which were already more difficult to get financed, will now be even more challenging to make the numbers work without a significant reduction in land and construction costs.

The last six months or so have been very painful being a variable rate borrower, especially given how the cost of interest rate caps has exploded. I was in the camp that the Fed would keep raising until they broke something, and then we would gain relief with rates having to come down. While many parts of the economy were slowing, the labor market was hanging in there, so that’s where I was looking for cracks to appear since, overall, the edifice seemed to be on solid footing. I have to admit that I didn’t think that what has transpired over the last couple of weeks would be the catalyst for a Fed pivot. Nor do I believe the Fed thought so, either. None of the Fed minutes have voiced any concern that the banking system was at risk by owning large amounts of no-default risk Treasuries and mortgage-backed securities. They completely missed the risk of banks having an unstable deposit base causing a run that might require them to sell those securities at a loss to cover the deposit outflow. They had the most liquid securities to help them cover the outflow, but no one expected such outflows, and they would actually have to sell these securities.

Hyman Minsky famously postulated that stability breeds instability. Things become so predictable that people don’t see risks building up in the system as they take on more of it, believing the stability would continue. Why would banks think that owning Treasuries and mortgage-backed securities with no credit risk be the cause of problems that could blow up the banking system? Usually, it’s risky loans and problems on the asset side of the equation. It’s rarely on the liability side with runs on the bank. That’s so 1930s. We’ve been long past that. Apparently not.

If Nassim Taleb is right, then we could be facing a volatile relationship in the realm of Elizabeth Taylor and Richard Burton. If you really want to help prepare mentally and emotionally for what may lay ahead, then I suggest you watch Who’s Afraid of Virginia Woolf?

{kind=link}

Leave a Reply