In the short run, the Fed chose to keep up the inflation fight despite deteriorating financial stability emanating from a wounded banking sector. There is now a lot of market data corroborating that the Fed will have no choice but to start cutting rates soon.

2-Year Treasury yields have dropped more than 1.25% since peaking in early March, and they dropped after the Fed announced that it was raising the Federal Funds Rate target by 0.25%.

Here is a longer-term chart of the 2-Year Treasury yield.

Longer-term rates have dropped as well in the aftermath of the Fed rate hike.

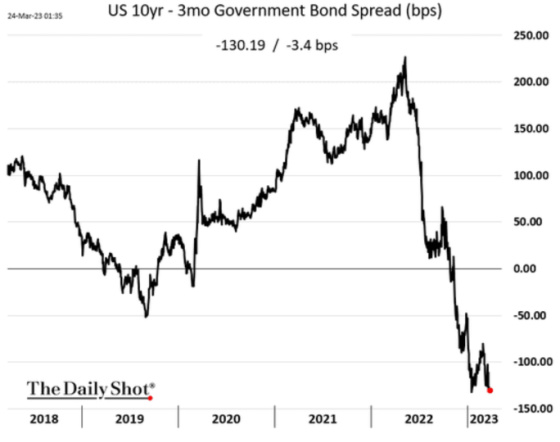

The yield curve has become incredibly inverted, which is foreshadowing weaker economic growth and lower short-term rates in the future.

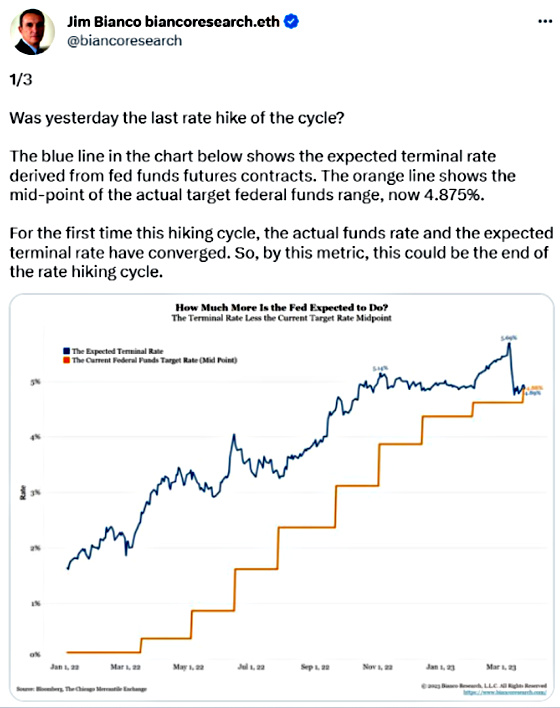

This tweet shows how for the first time during this tightening cycle, the terminal rate being priced in by the market is now less than the Federal Funds Rate.

The market is pricing in rate cuts starting in June and carrying on through at least January 2024.

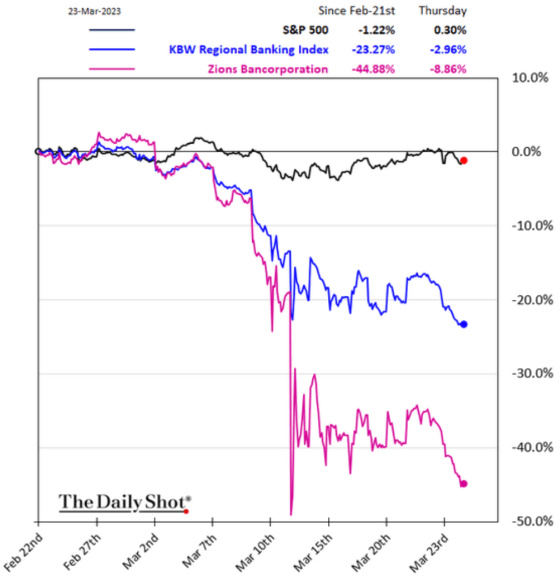

The banking problems cannot be ignored and will push the Fed to cut rates according to market pricing. One can see from these next two charts that equity investors have been punishing bank stocks, particularly regional banks.

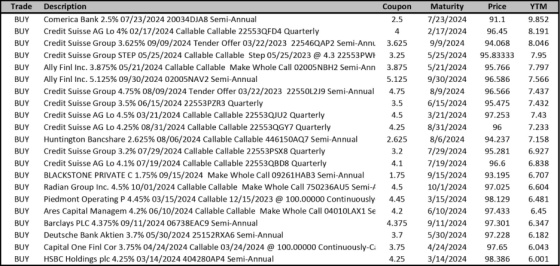

One bank that is looking increasingly fragile is Comerica. It has a bond maturing in 16 months. A Treasury security with a comparable maturity yields approximately 4%. Comerica’s bond yield is 9.85%. This is a very large premium and materially exceeds the yields of other financial firms perceived by the market as having their own set of challenges (e.g., Ally Financial and Capital One).

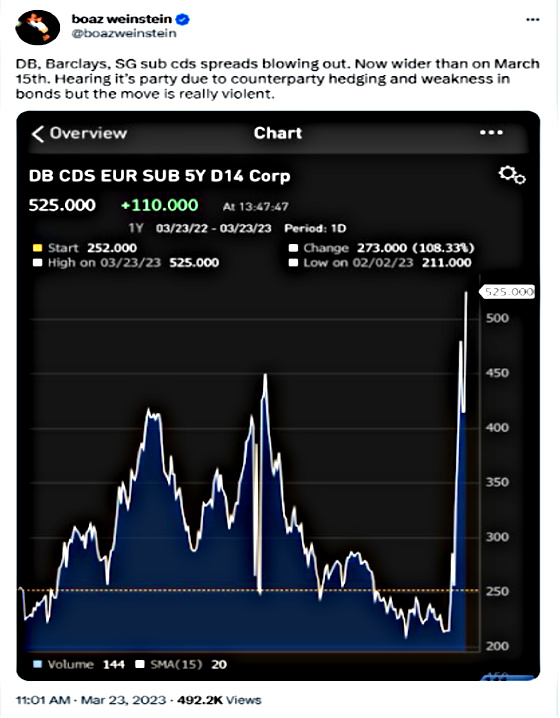

Unfortunately, the problems with Credit Suisse (now being taken over by UBS in a shotgun marriage arranged by the Swiss central bank) are now spilling over to Deutsche Bank. The cost of insuring against default has gone up quite significantly, as this chart shows.

One can see that Deutsche Bank has become a major focus for investors, so this will be something to follow closely in the weeks ahead.

And here are some rather sobering charts related to Lincoln National Corporation. Its stock price has dropped by close to 70% over the last year and 36% in the last month alone. The cost of insuring against LNC defaulting has gone up quite significantly. I don’t normally think about life insurance companies as being at financial risk, given how they are usually conservatively managed. In this case, however, it appears that its real estate exposure could be the culprit, and of course, they are not alone as most life companies have large loan books related to commercial real estate.

Unfortunately, investors are perceiving more overall risk in owning corporate bonds, as this chart shows how spreads have widened quite a bit in a very short period of time. This is especially the case for the lowest-quality credits, particularly in Europe.

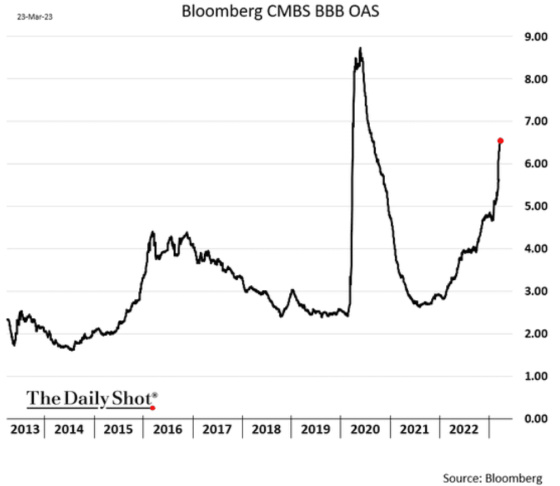

The higher returns required by lenders and debt investors are spilling over to securitized commercial real estate debt as spreads have blown out.

The widening spreads have led to the price of CMBS securities falling quite sharply over the last two months. This will make it even more challenging for borrowers with loans coming due to refinancing them as lenders will now underwrite new financing even more conservatively. This will lead to fewer loan proceeds which may cause even more financial distress as more commercial property loans, particularly office, and retail, go into default.

Despite lower interest rates, the prices for fixed-rate CMBS loans have dropped to levels even lower than they were during Covid and now only surpassed by 2009 when they were even more underwater.

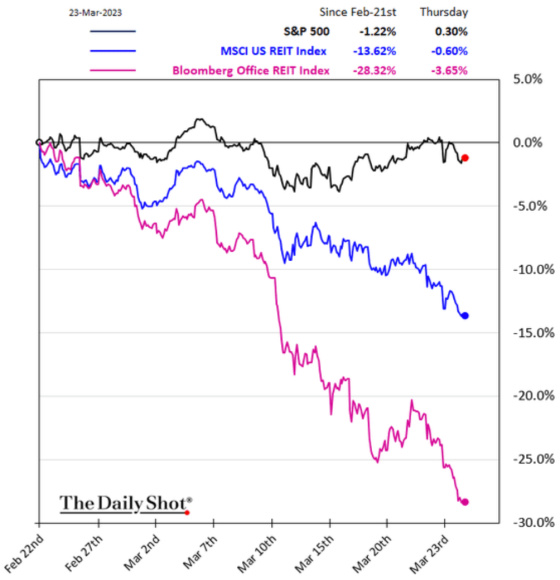

The challenges emerging in the banking sector and higher spreads on commercial real estate loans have hit REITs particularly hard, especially office building companies.

And the trends in office vacancies are not favorable as this chart shows.

One can see how much of the commercial real estate loan exposure is with smaller banks, which is not favorable for future commercial real estate lending as they have to be concerned about their current book of business performance, and they also have to be cognizant of depositors potentially moving their money to larger, healthier banks which may curtail lending.

All of this has come together to tighten financial conditions varying significantly over a short period of time. The Fed is counting on this to help give it cover to not only pause in raising rates but to begin lowering them as well, as this will help in its fight against inflation.

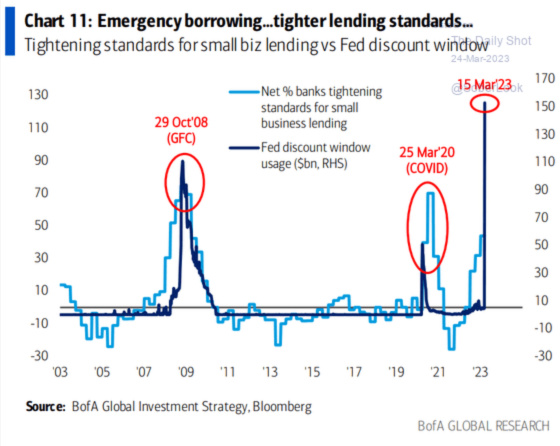

And if history is any guide, when banks borrow from the Fed in large amounts, then tighter credit follows.

So there you have it. I’m banking on the banking problems leading to the Fed finally being able to have the cover to not only pause raising rates but to start cutting them as well.

I think the market finally has it right and that Jay Powell will not fight back.

{kind=link}

Leave a Reply