I was definitely in the camp that once the yield curve inverted, we were headed for a recession within a year or so. The spread between the 10-year Treasury and 2-year Treasury yields went negative (inverted) in early July 2022. We are 15 months into an inverted yield curve, and so far, no recession.

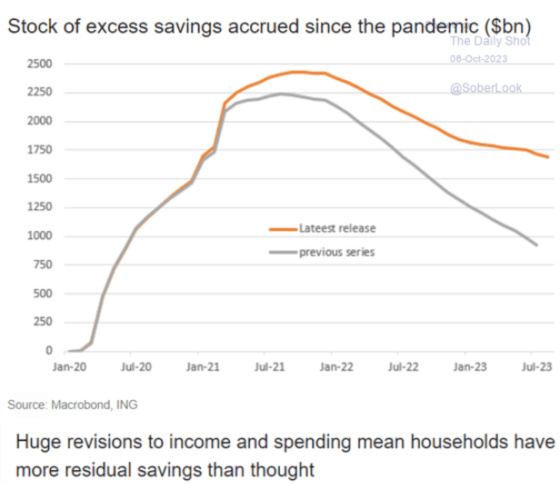

This chart shows one of the reasons why the recession has taken longer than what many expected. There was a massive revision to savings, which helps explain the strength of consumer spending. This is in addition to a large percentage of homeowners who have locked in low-interest rate loans and many corporations. This has somewhat shielded them from the impact of higher interest rates. In fact, for households and corporations with locked-in loans and savings, higher rates have resulted in much higher passive income, which provides fuel for spending.

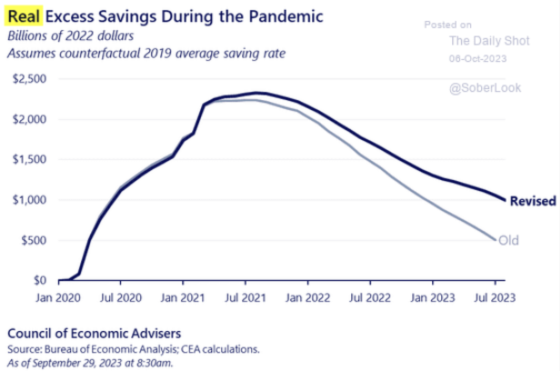

Here is the inflation-adjusted savings, which also increased significantly as well.

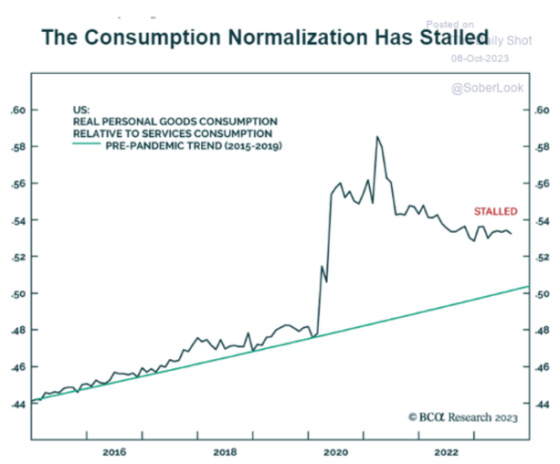

Goods consumption has remained quite elevated even after the Covid binge.

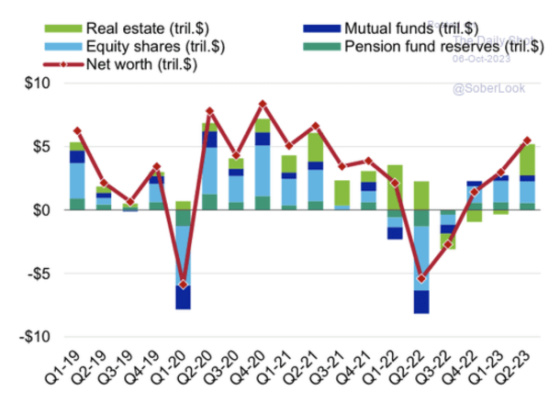

The growth in net worth of households has grown nicely as home prices have continued to appreciate despite much higher mortgage rates.

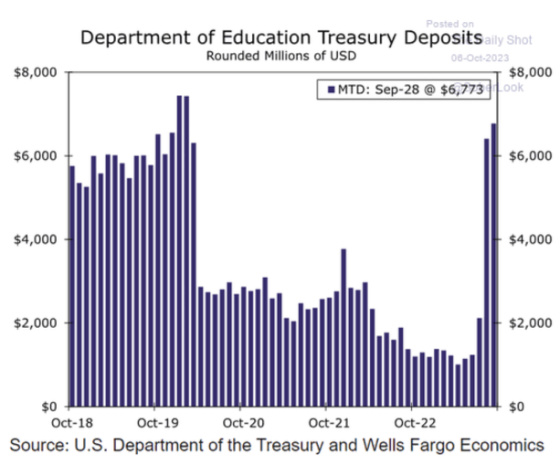

As this chart shows, one headwind is the resumption of student loan payments, which have already started.

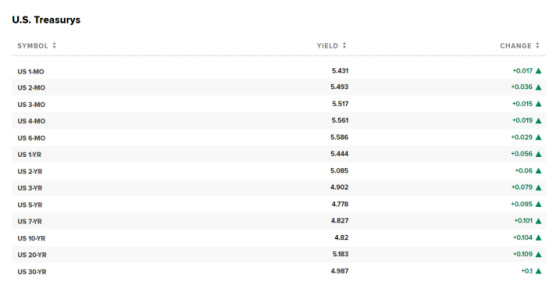

Last week, the employment report came out, and it was very strong. It contradicted the ADP employment report, which was quite weak and led to higher interest rates, reversing the ADP rally.

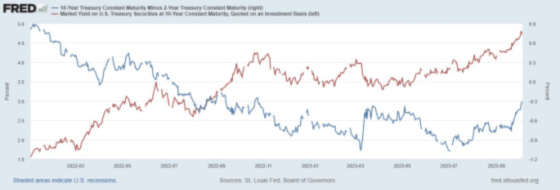

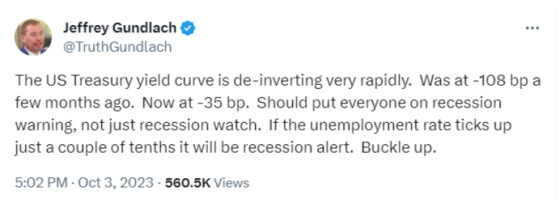

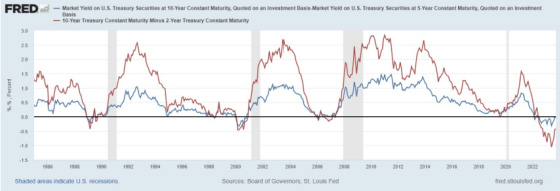

One can see that the de-inversion largely results from the 10-year moving up in yield to catch up to the 2-year versus the other way around. Jeffrey Gundlach is a well-known and successful bond investor who tweeted this last week.

In terms of my initial thoughts that the recession would take place sooner than has actually happened, I realized upon further research that an inverted yield curve in and of itself was not the most important event to start the recession watch/warning clock. The key is when the yield curve de-inverts, meaning long rates are higher than short ones. And this is what is starting to happen, although early on, I thought it would occur more from shorter rates coming down than the 10-year rising. Here is a chart of the 10 minus 2 with the 10-year yield plotted as well.

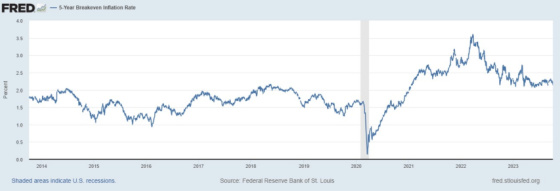

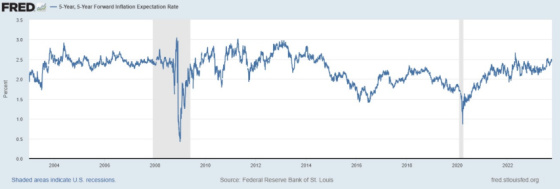

This next chart shows how investors are projecting inflation over the next five years out five years from now. This has actually come up a bit and is at the higher end of the Covid cycle but, unlike the previous chart, right in the middle, or slightly below the pre-Covid levels at 2.5%.

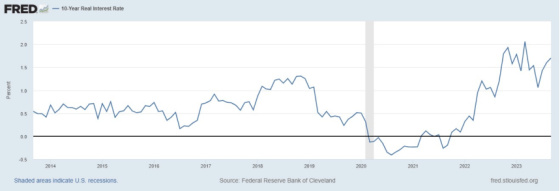

The most influential factor in the movement in long-term rates has been the increase in real interest rates. We are no longer in the emergency period when real rates were negative or hovering around 0%. They are now in the 2% range.

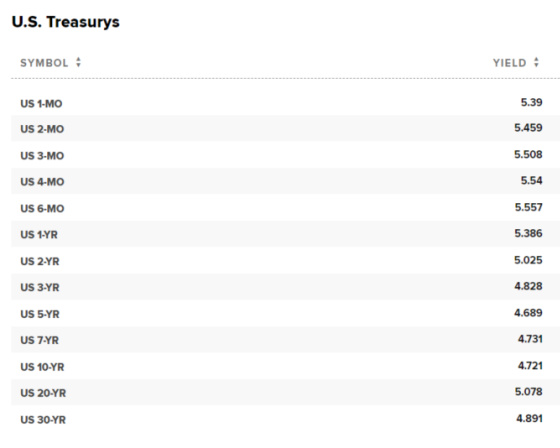

If inflation runs in the 2.50% range and real rates are around 2.00%, then this would simplistically have the equilibrium level for the 10-year be in the 4.50% range. I wrote previously that with previous highs in yield being breached that the next target would be 5.00%. If this were the case and with the 2-year yield being close to 5.00%, then we would be on the precipice of fully de-inverting.

I think last week was extremely important because there was a clear de-inversion between the 10-year and 5-year yields. This table shows what happened in the wake of the ADP report and the de-inversion between the 10 and 5. This was the first time this spread was positive since early July 2022.

In the wake of the very strong jobs report that came out on Friday, the question is whether the de-inversion remained in place. If it didn’t, that would be revealing as it could slightly reverse investor’s pricing in a recession, and if it did, then, in spite of the strong jobs report, we could still be on recession watch.

The de-inversion holds!

In spite of the strong jobs report, I’m now officially on recession watch, and when the 10 and 2 de-inverts, then the watch will shift to a warning.

I was curious to know how long it took for the 10 minus 2 to de-invert after the 10 and 5 did. This chart shows that, with the exception of today, where the spread is still rather wide between the two curves, the time is not very long. However, when the curves are very steep, there is a very wide gap between the two, with the 10 and 2 being much wider. When looking at this chart, one can also see how recessions start after the de-inversions.

It will be very interesting to see the next few jobs report, given the resumption of student loan payments, the UAW strike, and the frozen housing market, just to name some of the bigger headwinds. As I have gotten older, watched financial markets for many years, and learned the folly of making predictions, I have come to love the expression, “Only time will tell.” Only time will tell if this de-inversion is the start of a materially slowing economic growth that will lead to a contraction within the next six to 12 months or yet another head-fake that goes against recent historical trends.

I now need to hit the road for Las Vegas, where I’m seeing U2 at the Sphere. I can’t wait to experience a band that I love and have seen before but never at a venue like the Sphere. It costs $2.3 billion to build (approximately $1 billion over budget) and is supposed to offer the premier immersive concert experience in the world, which there is nothing to compare it to. The person for U2 in charge of their staging said historically, they developed a theme and built the experience around it. This is the first time they have had to build a show around a venue and all of its extraordinary, which created some immense challenges for the band and creative team. I can’t wait to report back on the experience.

{kind=link}

On main street we are in a recession. Budgets are tighter at home food cost and gas prices are insane, we need to new resturant concepts or paying $80 for del taco is going to be the norm and fast food is not worth $80. Wall can try and predict the recession all it wants but main street has been feeling a real recession for over a year.