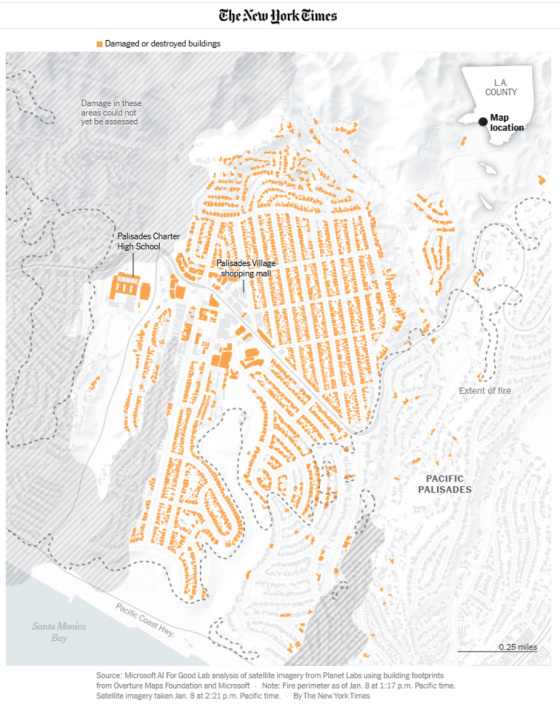

Last week was so devastating for those who lost their homes in the LA fires. This satellite image and analysis done by Microsoft of an area of Pacific Palisades shows over 2,000 buildings that were damaged or destroyed, with the vast majority being residential. As of January 12, 2025 – The Pacific Palisades fire led to the destruction of over 12,000 structures, including residential homes, historic buildings, schools, and places of worship.

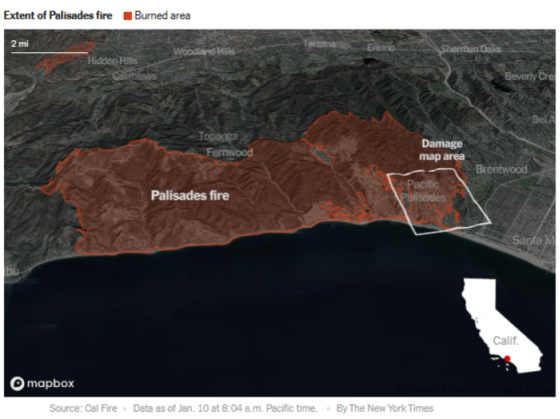

And to put the above image in perspective, it only represents a small percentage of the area impacted by the Palisades fire as this next map shows.

I’m in Orange County where we were fortunate to not have any fires but the winds we experienced were like nothing I can remember in terms of how high they got and for how long they were sustained. I’m also very cognizant of Daniel Kahneman’s warning that there can be a very wide gulf between one’s experience and memory. I know what I just experienced but all I have are my memories about what transpired before. With that being said, we’ve never seen such destruction like what took place in LA and, from a personal perspective, I have never had an event at my home shown below take place during my 23+ years there.

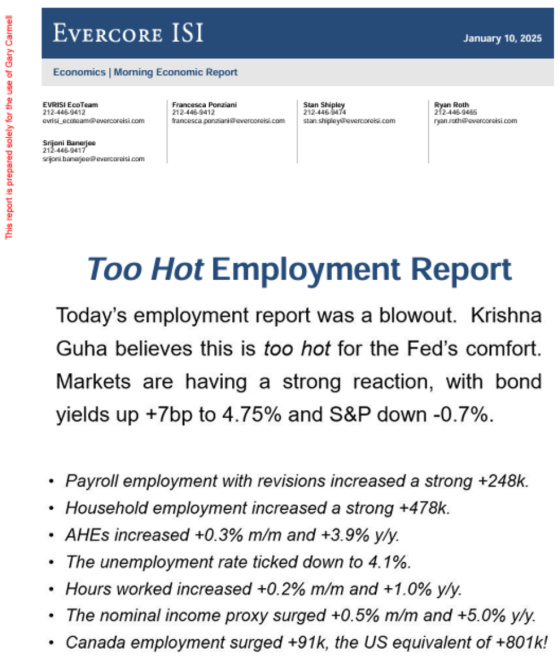

Obviously this pales in comparison to what other people lost but I wanted to share it because it serves as a journal entry into the diary of my life so that I can better align my future memory self with my current experiencing self. It’s also a good pictorial metaphor for the impact last Friday’s jobs report had on real estate borrowers and investors as the report was white hot and is resounding support for the Treasury market’s meteoric rise in yields that has taken place since the Fed first cut rates September 19th. It’s also going to cause some collateral damage to borrowers who need to refinance their maturing loans.

The 10-year Treasury yield is up approximately 1.10% since the September lows. Before discussing some of the ramifications of this, here is Evercore ISI’s summary of why this report was so hot.

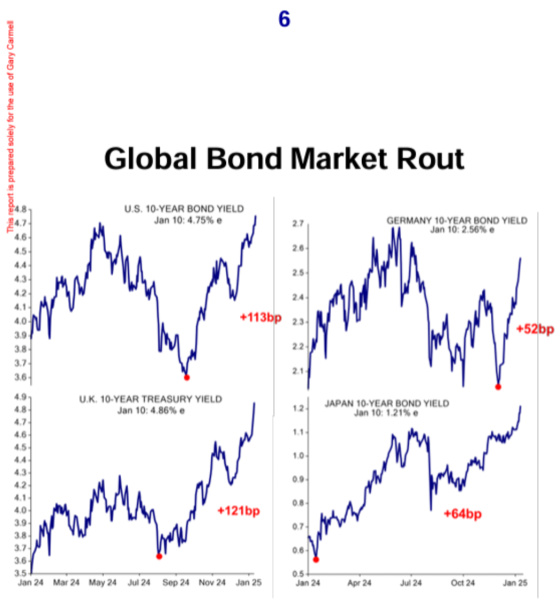

And the rise in yields is not just a U.S. phenomenon as these charts show.

Although there is a lot of detail that goes into loan underwriting and many variables involved, roughly speaking the movement higher in Treasury yields since September cuts borrower proceeds by approximately 11% assuming no change in underwritten Net Operating Income. That is a big deal if, prior to the rate movement, borrowers had loans maturing that did not have a lot of margin of safety in terms of qualifying for excess loan proceeds relative to the debt being repaid.

In addition to the impact of loan proceeds just from the current move in rates, most borrowers with fixed rate loans who have loans maturing will see a material change in the interest rate they are paying absent buying down the rate. A rate buydown allows the borrower to pay an amount up front to the lender in exchange for a lower rate over the term of the loan. For example, today for a 7-year loan for a 1% upfront fee, the rate would be reduced by approximately 0.18% per year.

Setting this option aside, I asked one of our mortgage brokers to tell me what the rates were on loans they did seven and 10-years ago. The range was roughly 4.25% to 4.50%. This compares to rates today in the 6.00% to 6.25% range which is a material jump in debt service assuming the prior loan was interest only.

Returning to today’s underwriting, let’s start by making the unrealistic assumption that property Net Operating Income didn’t change over the last seven to 10 years. Prior to the recent rate move a borrower would have qualified for enough proceeds to repay the maturing loan based on the more conservative assumption that the maturing loan was interest only for the entire term resulting in no principal reduction during the seven to 10-years it was outstanding.

With the recent spike in rates, however, that same loan would be upside down by about 15%, or by $6 million if we assume an original $40 million loan. Fortunately, during this time frame, for most markets and properties, Net Operating Income has risen by more than 15% so most borrowers should be able to weather their maturities without much need to put in additional capital. As time goes by, however, and rates don’t come down materially, then loans maturing in 2026 and beyond will have more challenges as their loans were originated in lower rate environments and generated even higher proceeds that will be more difficult to repay without needing additional capital.

On the one hand, if rates stay elevated then it will continue to make it more difficult for people to purchase homes so they will have to rent longer. It will also continue to put a lid on new projects being built because the rents are still too low relative to the cost of building to generate an attractive enough yield to entice investors to fund new development projects. Both of these serve to position apartment owners with much greater pricing power after the current wave of supply is absorbed. On the other hand, however, continued elevated rates will put more pressure on borrowers with maturing loans which could lead to defaults and foreclosures if they cannot access new capital to make loan paydowns or are unwilling to do so even if they have access to capital.

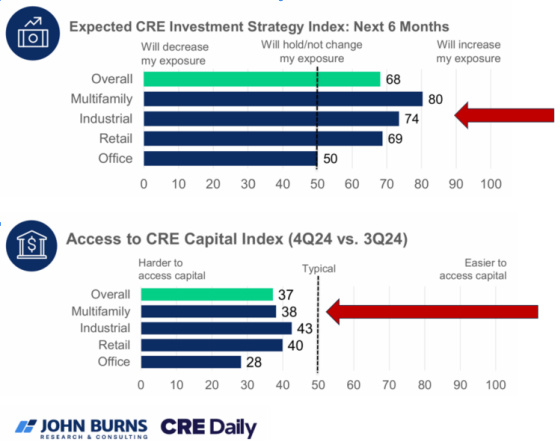

For those who have access to capital and are not playing a lot of defense with portfolio issues should be well positioned to capitalize on some opportunities resulting from borrowers that can’t fully repay maturing loans at a time when the operating environment should improve materially after 2026. The name of the game, however, is having access to capital. As this table shows, there is a very bullish belief about the potential returns apartments can generate but so few have access to capital to take advantage of the opportunities. If only LA firefighters had access to the large quantities of cold water that capital providers are putting on apartment investors, those fires could be put out far more quickly. Unfortunately, apartment investors are in a severe capital drought like LA has been when it comes to rain. Fortunately, without the same devastating consequences.

I started this post off discussing the horrific LA fires. I will leave you with this tweet from John Mayer that I thought was not only quite moving, but very insightful as well.

{kind=link}

Leave a Reply