In The Lion King there comes a pivotal moment when Simba has to claim his rightful place on the throne and confront Scar. His mentor/guardian Rafiki reacts to this crossing of the threshold by Simba with the line “It is time!”. This is how I feel about Jay Powell and the Fed in terms of cutting interest rates. It is time and I think the Fed is starting to recognize this as well.

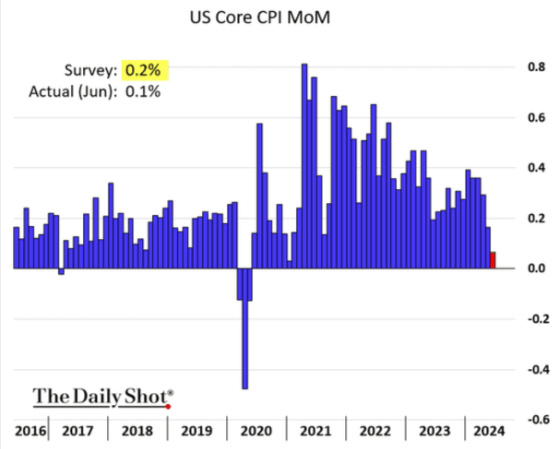

Last week’s CPI report was important for a few reasons. It’s the first one to show a drop on a monthly basis in four years as this headline shows.

This chart shows the significant drop in core inflation on a month over month basis.

On an annual basis core CPI is dropping nicely but still in the 3% range. There is more ground to be gained but the trend is encouraging.

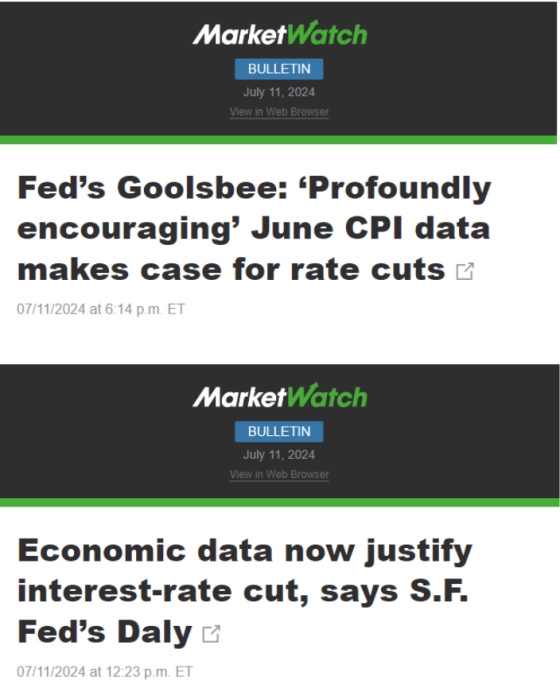

The inflation data is positive enough that we are finally having Fed Governors speaking about the inevitability of rate cuts as these next two headlines show.

The market is pricing in two rate cuts for 2024, albeit down from six at the beginning of the year.

Chairman Jerome Powell hasn’t quite jumped on the rate cut bandwagon as others have and this next chart may be the reason why. We have had other benign CPI readings only to see it rear its ugly head again multiple times. Powell is not willing to declare victory over inflation quite yet.

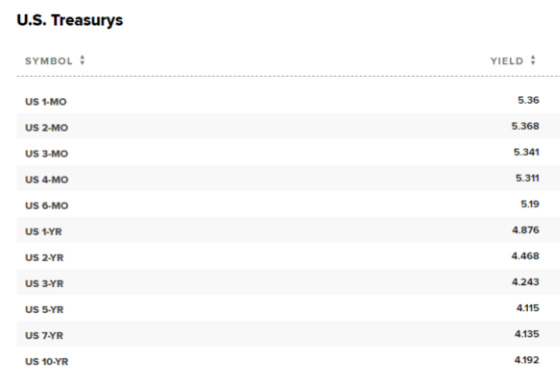

One of the signs I’ve been paying attention to in terms of a recession indicator is when the curve de-inverts. One can see that recessions have not started until the inversion of the yield curve in which the 3-month Treasury yield is higher than the 10-year Treasury yield is reversed. Absent a material move in the 10-year Treasury yield, this would require approximately 1.25% of rate cuts to de-invert this part of the curve.

We are finally reverting back to longer rates being higher than some shorter maturities as this table shows.

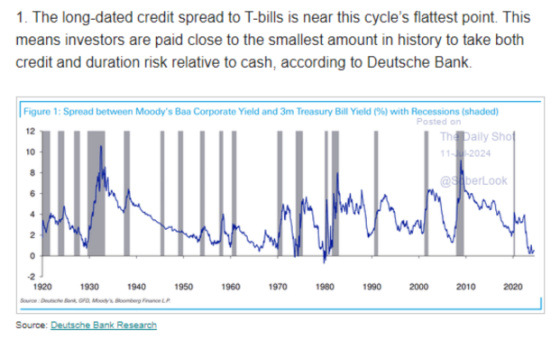

Here is another indicator that suggests a recession could be on the horizon. This chart shows the spread between Baa corporate bonds and 3-month Treasury yields. When it is very compressed, like it is now, it has been a precursor to a recession. This is probably because the 3-month T-Bill is too high relative to economic growth and needs to come down and this rate dropping materially is usually in response to recessionary conditions.

Finally, in light of the better CPI numbers, the 10-year yield has dropped by approximately 0.25%. It will be interesting to see if it can test the 4.00% level over the next few months.

I will sign off by channeling my inner Rafiki and tell Chairman Powell that you have done a great job and I understand your concern about inflation reigniting but I think it’s time to take a little pressure off of the system and start to lower rates. It is time.

I have to question the basic approach that has been applied by the Fed. The initial surge of price increases was driven by a shortage of supply that resulted from the COVID pandemic. It was compounded by the massive Federal infusion of funds to the public to aid COVID victims. this was followed by massive new spending legislation under the heading of “anti-inflationary” or attempts to deal with global warming and “make it in the USA” —- which fortunately could not get spent immediately.

One reality is that excessive spending by the federal government will cause inflation. So, to the extent that the excess in spending is being primarily caused by the USG how does raising interest rates cure that? This inflation period does NOT seem to be caused by excess private sector spending.

And then, massive USG spending is creating an unsustainable level of national debt.

This is madness!