Last week may have finally been the week when the Fed aligned with markets that the peak in rates may be in for this cycle. The Fed held rates in what was initially categorized as a “hawkish pause.” It was during the Jay Powell press conference that the market started to believe that maybe the Fed was done raising rates. The perception is that the Fed is now more focused on risk management versus fighting inflation. With both short and long-term rates having risen so much over a relatively short period of time and the Fed has been contracting its balance sheet since May 2022 by approximately $1 trillion (with a lot more to go), Powell acknowledged that monetary policy acts with a lag and that financial conditions had tightened quite a bit and could pose some risk going forward.

“Financial conditions have tightened significantly in recent months, driven by higher longer-term bond yields, among other factors. Because persistent changes in financial conditions can have implications for the path of monetary policy, we monitor financial developments closely.”

“… the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.”

“Slowing down is giving us, I think, a better sense of how much more we need to do, if we need to do more ….”

In addition to the distinct possibility that we are in the process of a Fed reaction function change from inflation to risk management, another favorable factor for the bond market was less supply hitting the market.

The third important factor that led to significant bond buying was a soft ADP private sector payroll report.

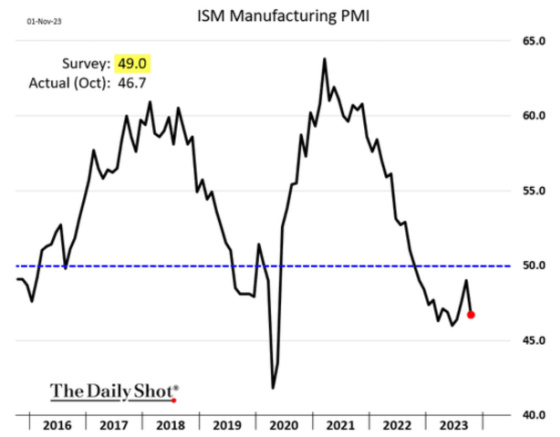

Finally, the ISM Manufacturing PMI came in weaker than projected and is in contraction territory.

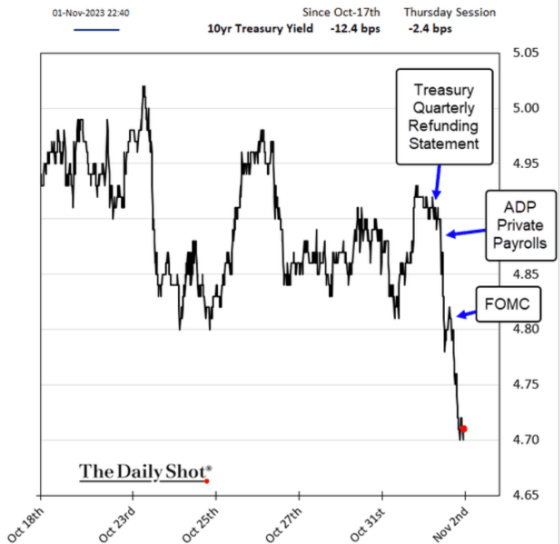

The combination of a more dovish Fed, less Treasury supply, and subdued economic reports led to a big rally in long-term rates, with the 10-year Treasury yield dropping comfortably below 5.00%.

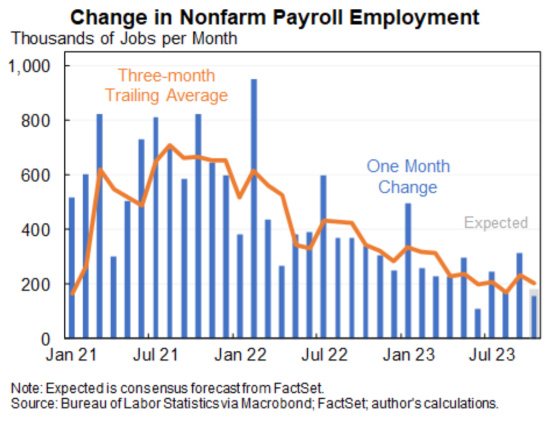

All of this happened prior to last Friday’s Non-farm Employment report, which came in lower than projected and led to an even bigger rally in bonds.

Employment growth has been on a consistent downtrend over the past two years, which is unsurprising given how significant job growth was to regain the jobs lost due to Covid.

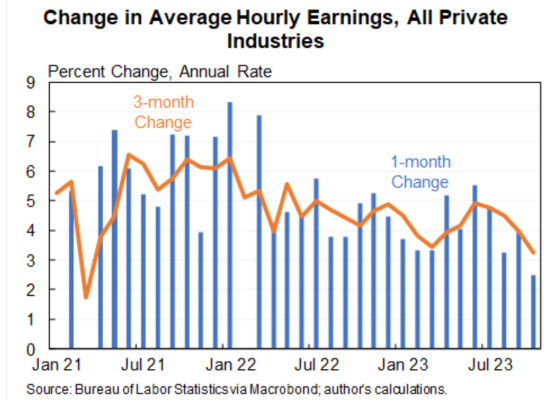

Average hourly earnings are also slowing, although not as rapidly as employment growth.

It will be interesting to see how the UAW strikes impacted the employment numbers. It’s possible this report could be weaker than future ones now that the strikes have come to an end.

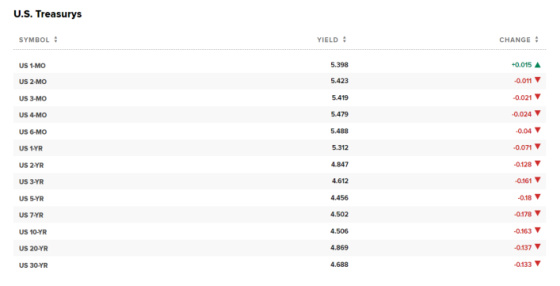

Here is the Treasury curve shortly after the market opened, and one can see that yields dropped across the board, particularly at the long end.

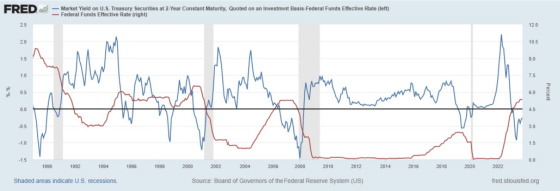

Equally important, the much more Fed policy-sensitive 2-year Treasury yield has now dropped back down below 5.00%, as this chart shows.

There is now approximately a 0.50% differential between the 2-year and short-term rates. As this chart shows, when the spread between the 2-year and Federal Funds rate is negative, this has been at times when the Fed Funds rate has been near a peak and on the cusp of coming down.

The question now is whether this break in rates is a sign of economic weakness and poor corporate earnings ahead, in which case this could be classified as Breaking Good in the sense that it would corroborate the Fed stopping from raising rates further and shifting its bias to risk management in the financial system and overall economy. It will be vitally important to see if economic reports continue to soften and what companies are saying about demand for their goods and services.

If, on the other hand, the bond market is rallying and pushing rates lower, and this serves to loosen financial conditions such that it restimulates animal spirits, and this translates to greater corporate investment and overall consumer demand, then this could lead to shifting its focus back to fighting inflation versus risk management. This could lead to the Fed not being done in this cycle, which would make this Breaking Bad.

I will end this with an excerpt from a brief research report that came out on Friday from www.sentimentrader.com, which looked at the TLT, which is a proxy for 20+ year Treasury bonds. One can see how brutal the last three to five years have been for owners of this ETF and for investors in long-term Treasuries overall.

The researcher wanted to know if the sharp rally in the TLT that took place last week was a sign of future strength or did it represent a form of irrational exuberance? Here is how the report ended, which suggests some caution ahead.

What the research tells us…

Long-term treasury bonds suffered a staggering 50% drawdown from their 2020 high to their recent low. It is only natural to expect a rebound rally of some degree. However, traders were suspiciously quick to leap onto the bullish bandwagon at the first sign of relief. Are they correct? Is the worst over for bonds? We cannot predict. However, we can note that many times in the past, a market that suffered a sharp decline often experienced a great deal of volatility while trying to put in a final bottom. Retests of the initial low – and occasional false breakdowns – are not uncommon. This historical precedence, combined with the short-term weakness that has generally followed the indicator signals above, suggests that bond buyers temper their enthusiasm for long-term bonds in the near term. A bottom may be forming, but there may be some significant volatility ahead.

If the researcher’s caution is warranted, then there is a distinct possibility that this drop in rates could be breaking bad. Only time will tell.

{kind=link}

Leave a Reply