I saw ten thousand talkers whose tongues were all broken

I saw guns and sharp swords in the hands of young children

And it’s a hard, and it’s a hard, it’s a hard, it’s a hard

And it’s a hard rain’s a-gonna fall

-Bob Dylan A Hard Rain’s a-Gonna Fall

We had our annual planning meeting last week, and it reinforced for me, yet again, that the one thing I do know is that there’s a lot I don’t know. Of course, it’s important to have a point of view when making an investment, a hypothesis as to why you’re making the investment. What I have learned, though, is that the more things that have to go right, the less chance the investment will pan out. The more one has to tweak one’s assumptions to generate the “required” rate of return, the more nervous you should be about making the investment. The more of a story you have to spin to justify the investment, the more risk is associated with it.

I have also learned through the school of hard knocks that, at some point, in the famous words of Bob Dylan, a hard rain’s a-gonna fall. A subprime problem that creates financial and economic contagion, Covid, banking problems, the war in Ukraine, etc. I’ve always found George Soros’ investment approach quite fascinating, not only because of his incredible success but because of the philosophy behind it. I’ve written about him a number of times, but in this context, I have found myself thinking a lot about his false premise theory.

Economic history is a never-ending series of episodes based on falsehoods and lies, not truths. It represents the path to big money. The object is to recognize the trend whose premise is false, ride that trend, and step off before it is discredited.

~ George Soros

This is a good summary of his philosophy, along with quite extensive excerpts of a Soros speech articulating his philosophy. In some ways, one could say that I fell victim to a false premise that the trend of lower highs and lower lows in interest rates would hold because of how financialized the economy had become, the Fed was more worried about deflation than inflation, and the trends of disinflation were too powerfully entrenched to be reversed in any long-term, meaningful way. In other words, although rates would inevitably go up after we got through Covid, they would not exceed 2.50% by any material amount.

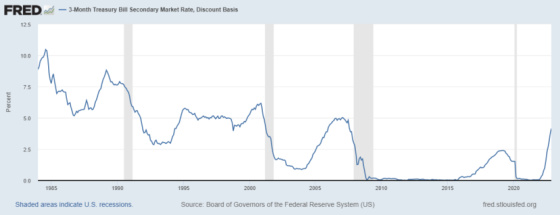

This is a chart of the 3-month Treasury bill yield between 1984 and 2021.

One can see why betting on rates remaining low seemed pretty reasonable. We had the added benefit of having prospered from doing this by having bet on it in a meaningful way from 2010 forward. The chart shows pretty clearly how each cycle had a lower peak and lower trough rates. Add to this that I also took Fed chairman Jay Powell at his word when he reiterated over and over during 2020 and 2021 that the Fed wouldn’t raise short-term rates until the end of 2023 at the earliest.

In spite of the above factors, it should also be pointed out that once rates reached 0%, they weren’t going to drop anymore since it was clear that the Fed was not going to allow rates to go negative. So there was all risk in that rates could only go higher and no reward for them going lower. So we had to believe the risk-reward of staying variable was in our favor for other reasons. These were the prepayment flexibility associated with variable rate loans and the starting rate advantage that we thought would offer us an average interest rate that would either be less than prevailing fixed rate loans at the time of origination or not exceed them materially during the life of the loan.

We have always found great value in prepayment flexibility, so that is not something we were inclined to give up by converting to fixed-rate loans. In addition, with a few rare exceptions, the spread between fixed-rate loans at the time of origination and the starting rate for floating was typically 1% to 2%, so we felt like that was an important advantage, especially since we believed that short-term rates would probably not breach the previous peak of 2.50%. Well reasoned with the support of over a decade of having prospered from this strategy but also wrong.

“Never did that before.”

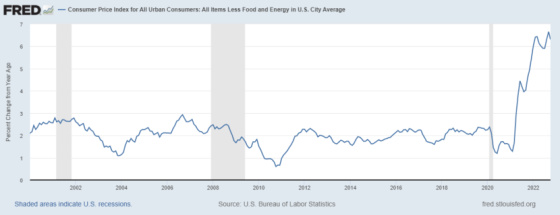

What did the farmer say when his horse dropped dead? “Never did that before.” The response to Covid set the stage for the “never did that before” Fed reaction function. Well, to be fair, the Fed had done that under Volcker, but during my 35+ years at CWS, Covid led to a lot of “never did that before” situations, including the Fed’s rapid reversal. Covid unleashed massive fiscal and monetary stimulus along with frayed supply chains that were exacerbated by the shift to goods from services because of lockdowns and much less of a desire to congregate. It also shifted housing preference in a powerful way that would also set the stage for unprecedented rent inflation that perhaps we should have seen as a precursor to inflation going much higher than the historical range it had been, as this chart shows. A perfect pictorial example of “never did that before.”

I must take a step back here and say that from the beginning, my biggest concern about our variable rate strategy was exactly what has been happening. In the past, when I was asked when I would shift to fixed-rate loans, I was often hard-pressed to answer that except under one set of conditions. And that was if there was a regime change in monetary policy that had the Fed shift from fighting the risk of disinflation and deflation in a highly leveraged economy that was dependent on continued debt creation and the refinancing of maturing debt to one that is much more worried about inflation and fighting that aggressively through higher rates and tighter monetary policy and this flowing over to the cost of interest rate caps. Caps are very volatile instruments in how they are priced. For a number of years, they were very cheap insurance but when interest rates are rising, and volatility is high, they can become incredibly expensive in a very short period of time. And this is what has happened as cap costs have exploded. And we are almost always required to purchase interest rate caps which, up until now, had been very cheap.

This “hard rain” scenario was not just a scenario that we assigned a low probability to and essentially ignored. Rather, we recognized that it could happen, so it was important to make our leverage and hedging decisions with this scenario in mind. For example, we purchased an interest rate cap for 58 of our properties in mid-2020 that covered approximately $1.7 billion in debt that would pay our properties if the 30-day LIBOR exceeded 1.25% through December 1, 2022. We paid approximately $1 million for that cap. Now let’s update the chart above and look at T-bill yields for 2022.

One can see how short-term interest rates shot up and breached the previous cycle high. I’m now obviously quite pleased we bought that cap as it has paid out more than $10 million and kept our cost of funds at a very low level for 2022 for most of our properties. Unfortunately, however, the cap has now expired, and we now have much higher rates to contend with going forward as our replacement caps are at much higher LIBOR rates. I would say that not buying a three-year cap (versus the 30-month cap we purchased) is one of my biggest regrets looking back because this would have covered us through mid-2023.

And while I think there still would have been a big spike in our interest payments, by then, it will be clear that inflation will have convincingly been coming down and the economy will have been much weaker, thereby leading the Fed to stop its hikes and begin positioning for lower rates ahead. This would have preserved our prepayment flexibility and given us a hedge in the event a recession ensues, and rates follow lower. This would help us cushion some or all of the impact of potential revenue weakness that may have occurred because of lower household formations and potential excess supply of apartments.

I can’t overemphasize how much importance we assign to our floating rate loans being a good downside hedge in the event of a recession. We are much more focused on downside protection than upside maximization. In fact, this hedge worked wonderfully during Covid when rates dropped significantly, and our revenues were initially under pressure. It then worked even better when the Fed held rates low, and our revenues accelerated beyond our wildest expectations. As an aside, this probably should have been a warning sign to us that the Fed was way behind the curve from an inflation standpoint in that our revenue growth is well correlated to economic activity but this rate of growth seemed so beyond expectations that it definitely had a macro inflationary component to it. Back to our hedge. When rates did start rising, we at least had strong revenue growth to cushion some of the below—another indication of an effective hedge.

Along with the caps we purchased, another way we tried to hedge against the “hard rain” scenario was to be prudent with our leverage levels and focus on securing 10-year loans with full-term interest only at the lowest spreads we could get. We knew this would come at the expense of loan proceeds, but that was not an issue for us as we were playing to stay on the field in perpetuity. The only way to do this was to have leverage levels that could handle much higher interest rates combined with large cash balances to handle the potential for much more expensive interest rate cap purchases when our cheaper ones expired.

We had no desire or inclination to go for the much higher leverage, short-term, higher spread debt fund loans that so many people in the industry used in 2021 and the first half of 2022. A lot had to happen to not run into trouble, given the very high multiples being paid for properties (low cap rates) and high debt levels used to finance them. It required continued unprecedented rent growth, interest rates staying near 0%, and strong liquidity continuing to flow into the industry to provide for profitable exits for their investments.

In hindsight, it appears that multiple false premises were the basis for this investment strategy. The supply/demand imbalance from Covid population shifts and housing preferences due to remote work and lifestyle changes would continue to produce extraordinarily high rent growth when in fact, this was temporary in nature. Even if all of the leases were repriced at these much higher levels over the next 12 months, this would still produce a yield on cost that was only acceptable if properties kept trading at very low cap rates but offered very little margin of safety if rates went higher and cap rates followed suit. And this assumed that there was no execution risk or change in market conditions. And with these loans typically being three years in length with some potential for two one-year extensions if certain performance criteria were met, a lot of things had to go right, and I mean really right. It required continued unprecedented rent growth and low-interest rates, which upon further and deeper reflection, we should have concluded would not be possible for any material length of time. And let’s not forget that these conditions created significant incentives for developers to keep building so a large amount of future supply was inevitable while basing one’s investment on continued unprecedented demand and paying record-high multiples was fraught with peril.

One of the reasons I find writing this blog so helpful is that I don’t always know where they will go or end up when I start, and I can use it to help work things out that I may have felt intuitively but couldn’t quite articulate. Letting it flow can be very helpful for me to gain some clarity. This is a good example of that coming to realize that maybe the ultimate false premise was that rents, which have been a pretty good barometer of economic activity and the direction of interest rates, could become unhinged from Fed policy for an extended period of time, such that we could have our cake and eat it too in terms of rapidly accelerating rents and continued low-interest rates.

And while I feel like we positioned ourselves well for the hard rain scenario resulting from monetary regime change and no longer having our cake and eating it, too, the same cannot be said for highly leveraged buyers of apartments. Investing based on this false premise would have allowed them to be able to turn a profit in a relatively short period of time because higher leverage requires less appreciation because a 10% increase in value with 25% equity represents a 40% return on equity, while someone with 50% equity has 20% appreciation.

Of course, higher leverage, floating rate loans with high spreads and short maturities also introduce much more risk. These buyers needed rates to stay low, rents to continue to increase at unprecedented levels, execute flawlessly on their business plans in the face of increasing supply, and have cap rates stay quite low along with strong liquidity continuing to be available for apartment purchases. All of these had to remain in place with any one of them not occurring, putting the entire investment premise at risk. That’s not a good place to start when making an investment. This is why I think we will see a number of owners being forced to sell or recapitalize their investments in 2023 because the yields they are earning are now much lower than the cost of their debt, thereby creating a collision course with running out of money.

We see 2023 as a year in which some compelling opportunities should materialize for firms like CWS. We think very well-located, quality real estate should be able to be purchased at compelling cap rates offering prudent purchasers and strong operators a margin of safety that should allow for managing through a highly anticipated 2023 economic downturn.

I will wrap this up by turning to some research about catastrophic failure that I have always found to be quite interesting. I think it’s vitally important to always be cognizant of what can lead to ruin, so when I find research about it I’m always interested in diving in to learn more and apply it to my own decision-making. I referenced this in my book.

According to D.D. Woods and R.I. Cook, catastrophic failure can occur when we have great difficulty in synchronizing mindset to goals and priorities in a changing world. This is the part of their research that I found most relevant to missing the regime change related to Fed policy.

One’s mindset may be too hard to interrupt and re-focus – fixating on one view of the problem

- Failure to revise situation assessment as new evidence comes in, evidence that indicates an evolution away from the expected path in the face of opportunities to revise

- Breakdowns in the process of error detection and recovery where PEOPLE DISCOUNT DISCREPANT EVIDENCE and fail to keep up with new evidence or a changing situation

- The immediate problem-solving context has biased the practitioners’ mindset in some direction inappropriately

There you have it. Paul Simon syndrome in which “a man sees what he wants to see and disregards the rest.” I used to think purchasing interest rate caps was a waste of money because I didn’t think rates would go that high and because we manage our cash and distributions conservatively, we are essentially self-hedged.

“a man sees what he wants to see and disregards the rest.” - Paul SimonClick To TweetWhat I didn’t consider, however, although we did end up buying the very cheap cap in mid-2020 that I discussed earlier, was how we could have taken advantage of the cheap insurance and be in a position to have these caps pay off by purchasing lower rate caps versus the much higher rate ones we bought because we were forced to. Caps can be used offensively to allow for them to be purchased when they are cheap, and yes, the chances of them not paying off are high. However, when they do pay off, they can provide an additional, valuable hedge and still allow us to retain prepayment flexibility. In addition, for those properties we have no intention of selling, then be much more open-minded to locking in our rates for longer periods of time, even if that reduces prepayment flexibility.

At CWS, we have been in business for 53 years, and this would not have been possible without acknowledging where we have fallen short and trying to learn from our mistakes and what we would have done differently. Most importantly, we have then tried to incorporate those lessons learned into our decision-making process going forward so that we become even more cognizant of risks to which we are exposing ourselves. 2022 has been quite a learning experience and one that I hope we will learn from and help us become better decision-makers at CWS.

{kind=link}

Leave a Reply