The U.S. apartment market has gone through a very intense swing from the greatest market in my life in 2021 and early 2022 to a far more challenging one from 2023 through today. The pendulum swung far to the left in the wake of low interest rates, the huge demand for apartments, rent spikes as supply chain disruptions resulted in insufficient supply, and a corresponding explosion in values as net operating income skyrocketed and cap rates fell.

What God giveth he can take away as developers will put shovels in the ground as fast as they can to capture any development arbitrage, which is what happened as supply exploded in 2023-2025. As a result, the pendulum started to reverse with rates rising, supply increasing dramatically, operating costs spiking, rents dropping, and values contracting by nearly 20% from peak to trough according to Green Street. Add to the mix more government intervention and the end result is a much more challenging environment for apartment owners.

One of the thoughts I’m wrestling with is that the pendulum reversal seems to have been unnaturally and temporarily interrupted via huge absorption of newly built apartments as a result of massive developer rent discounts. It’s quite possible that this has pushed forward demand by stealing household formations from the future. In addition, the proliferation of private credit via real estate debt funds has given a lifeline to developers whose projects wouldn’t normally be able to refinance their construction loans without having to bring in additional equity. These debt funds are often willing to provide new financing such that no additional equity is needed because they believe the collateral supporting their loan provides them with a margin of safety, even if the market doesn’t recover as anticipated, and they ultimately end up owning these newly constructed communities. And while these developers will still face operational challenges given all of the competition they are facing and very little positive cash flow, it’s still better than having to come up with a lot of money to pay down their maturing construction loans or have to sell at what could potentially be a material loss. This pendulum counterweight has led to less distressed sales of apartment communities than would otherwise be the case..

When looking in the rearview mirror, apartment demand has been extraordinary and has been able to exceed the huge amount of new deliveries over the last year. Unfortunately, we may have reached the point where there may be demand exhaustion, as the following table could show if third-quarter absorption is not an anomaly.

The third quarter is typically strong for leasing activity, and yet, every market, except Philadelphia, has seen absorption drop such that it is now less than completions. Apartment bulls have pointed to supply dropping as a ray of light, but the concern materializing is that it may not be dropping fast enough to make up for softening demand. Have we stimulated far more demand than economic activity would have naturally produced? Supply has clearly catalyzed demand as lower rents entice more people to form new households. This is evident by the rolling four-quarter numbers, which show that demand exceeded supply in every market except Denver and Miami. With the significant reversal in the third quarter, the question weighing on me is how much gas is left in the tank for apartment demand, especially if rents start rising materially or the economy contracts from its slower current state.

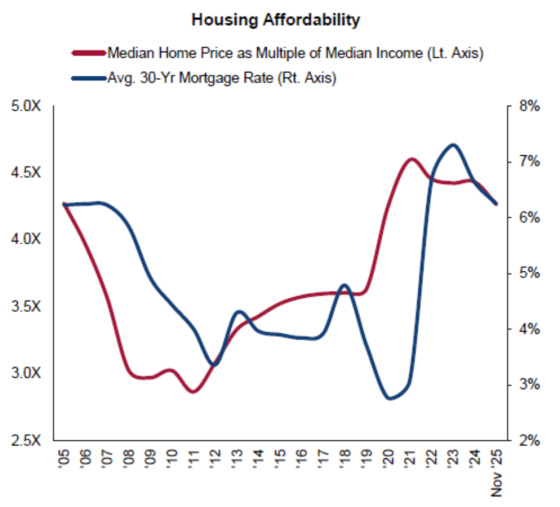

One of the factors holding up apartment occupancies higher than they would normally be is the significant premium to purchase and own a home versus renting. This has led to less turnover at apartment communities, which takes some of the leasing pressures off apartment communities. The following chart shows how home prices relative to incomes are higher than they were during the housing bubble of 2005-7, despite the tremendous run-up in mortgage rates. If mortgage rates drop materially, which I’m not banking on, then this could result in more move-outs by renters purchasing homes.

Source: Green Street

Another source of demand for apartments has been the large number of young adults living at home. We’re finally starting to see the percentage of 25 to 34-year-olds living with their parents dropping after steadily increasing for 50 years. I have to believe that this percentage, having finally started to drop, is largely due to the abundance of highly discounted rents offered by developers to expedite their leaseups or just to remain competitive in the marketplace.

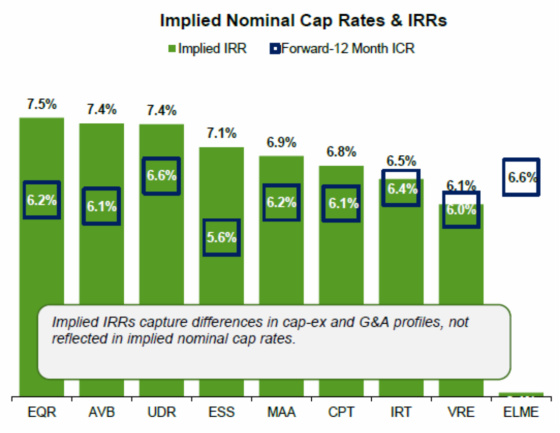

This chart from Green Street shows the implied capitalization rates of publicly traded apartment REITs. With many of them trading at cap rates of 6.0% or higher, they are clearly discounted relative to private market values (4.75% to 5.50%), which is why we have seen some smaller REITs being taken private. With that being said, operating fundamentals remain difficult with more of them cutting their forward guidance. Perhaps REIT investors are pricing in the pendulum returning its momentum to the right after being interrupted by pulling forward future demand via heavily discounted rents and the preponderance of debt fund and other forms of rescue capital putting off the day of reckoning for developers and those who bought at the top of the market in 2021 and early 2022.

Source: Green Street

I will be eager to see absorption numbers for the fourth quarter, which I expect to remain soft as it is a seasonally slow time of year. Given this, all eyes will be on the first quarter, which is typically stronger. That will be incredibly important to see if the pendulum’s momentum starts shifting back to the right as demand exhaustion is real or whether it regains its concession-induced strength.

As I often like to end my posts, only time will tell.

{kind=link}

Leave a Reply