Last week the CPI report was released. One can see that shelter is now by far the biggest component of inflation. Non-Housing Services are growing at a moderate rate while Core Goods prices are declining.

This chart shows how CPI excluding shelter has been moderating quite significantly, although July’s reading was slightly higher than June, representing the first increase in 12 months.

Given how CPI tracks rents based on the changes in the average leases in place versus new leases signed, rent movement, up and down, is captured more slowly than what current leasing activity would convey. This chart shows how the housing components of CPI are projected to slow quite meaningfully in the months ahead, which should help lower the inflation rate, although there are pressures being felt in the energy arena with higher oil and gas prices which may offset some of this benefit.

This chart shows what is happening to those categories that the Fed classifies as sticky, meaning their prices don’t change nearly as much as other components. This also excludes shelter, and it too is dropping quite precipitously and is now below 2%.

Last week I mentioned how it felt like the 10-year Treasury yield wanted to stay above 4.00%, and I think last week’s action corroborated this, at least in the short run. In spite of fairly favorable CPI news, the 10-year breached the 4.00% threshold for just a very short period of time to 3.98% but couldn’t hold it there and on Friday went materially higher in the wake of a less favorable wholesale inflation report (Producer Price Index) and continued hawkish speak from a Fed Regional President.

San Francisco Fed President Mary Daly said that it was too soon to determine if the Fed is done raising rates which was not music to the ears of bond investors.

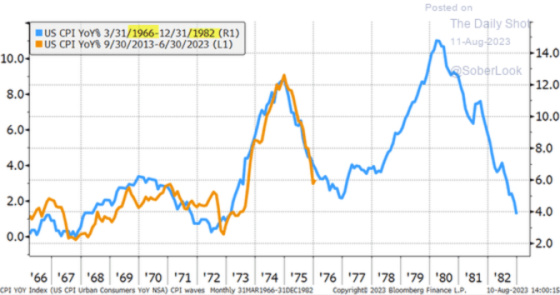

This is the Fed’s worst nightmare, a repeat of the acceleration of inflation that occurred in the 1970s and early 1980s.

Wage growth is holding strong, which adds concern to those in the acceleration camp.

![]()

Here is last week’s chart of the 10-year Treasury yield.

As this longer-term chart shows, it’s still holding below its cycle high of approximately 4.25% but keeps trying to bump up against it.

Clearly, the Fed is making progress on the inflation front, and it’s finally filtering down to consumer expectations, with the outlook for inflation over the next year dropping fairly significantly.

In addition to declining inflation expectations, there are clearly pockets of weakness in the economy, as this chart shows that business demand for bank loans in the United States and Europe is dropping precipitously.

Finally, here is what ZipRecruiter management said on its conference call last week after releasing its earnings. They withdrew guidance because the environment for staffing for small and medium-sized businesses has really weakened and has become much less predictable.

Quarterly paid employers were 102,000 representing a 35% decrease versus Q2 ‘22 and a 4% decrease versus Q1 ‘23. This is primarily reflective of weakness among small and medium-sized businesses, which make up the vast majority of our paid employers. Revenue per paid employer was $1,677, an increase of 9% every year, with sequential decrease of 3%. The sequential decrease was driven by employers’ willingness to pay being unfavorably impacted by overall macroeconomic conditions.

Moving on to guidance, as Ian mentioned earlier, employers have continued to pull back and hiring in light of an uncertain macroeconomic backdrop, the speed of this deceleration is particularly noteworthy, the July’s revenue being down approximately 31% year-over-year. This informs our Q3 ‘23 revenue guidance of $150 million at the midpoint representing a 34% decline year-over-year. The atypical hiring patterns observed year-to-date give us limited visibility beyond Q3. Q4 has typically been a seasonally softer period for hiring. And we do not yet have a clear view of when employers confidence will recover.

Despite a clear slowdown in inflation and some weak economic signals, the market seems to be increasingly taking the Fed at its word that rates will not be reduced in 2023. The 10-year is hanging above 4.00% and the 2-year has not dropped much either which is more sensitive to zFed policy. And while ZipRecruiter is seeing Zip in terms of business growth, investors are pricing in zip in terms of interest rate cuts for the remainder of the year.

{kind=link}

Leave a Reply