The bond market detests Donald Trump’s approach to tariffs.

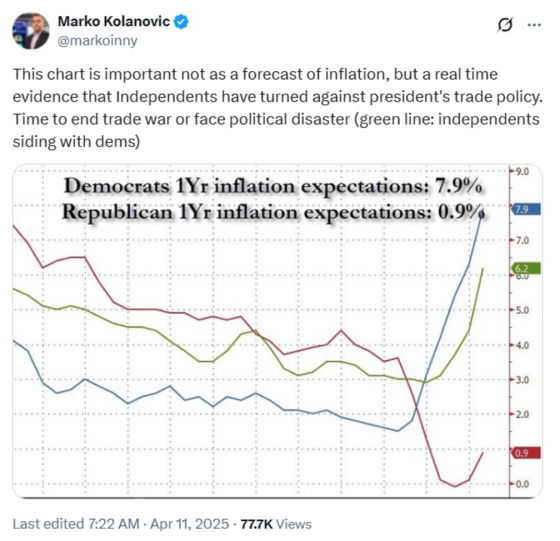

Equally importantly, it appears that much of the American public does as well. This chart should scare Donald Trump as independent voters are now very concerned about inflation spiking in the near future. It’s no longer the ideologues on both sides either ignoring it or worried about it because it hurts Trump. It’s middle of the road voters.

As much as people want to attribute his backtracking on tariff implementation to being a master negotiator and Trump playing 5D chess, I think it’s clear he got spooked by the market’s reaction, especially the bond market, and he needed an offramp. Unfortunately so much damage has been done to U.S. credibility that we can no longer be trusted, which is a shame, because with the dollar at the center of the global economy as the reserve currency trust in the United States is paramount to keep the system functioning effectively.

I agree with what Jamie Dimon said in his annual shareholder letter.

“America First is fine,” Dimon writes, “as long as it doesn’t end up being America alone.”

As for Europe, he says members of the European Union need to reform their economies and increase their military spending and preparedness. “This is going to be hard, but our country’s goal should be to help make European nations stronger and keep them close.”

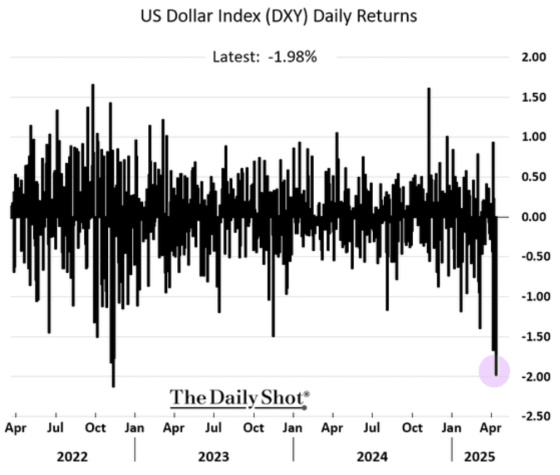

The dollar got hit very hard last week. Part of it could be the unwinding of leveraged carry trades while I’m sure it’s also attributable to global investors wanting less dollar exposure because the administration’s policies are perceived to be less investor friendly and more unpredictable.

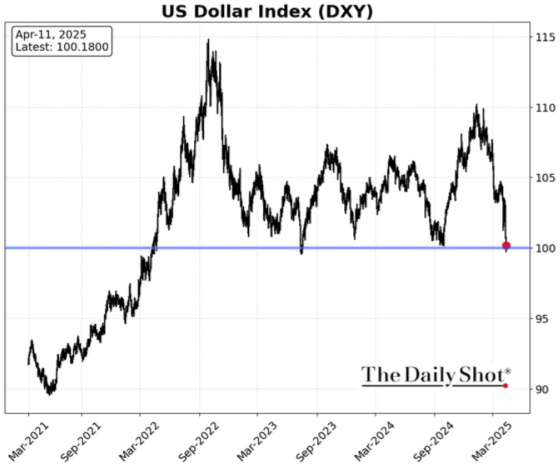

The dollar is testing support at 100. If it goes below that level it could drop materially more.

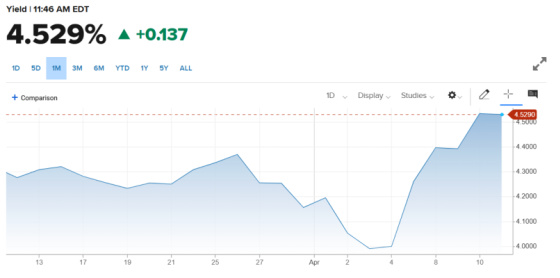

The 10-year Treasury yield was up over 0.50% last week. Part of this may be attributable to a very popular and crowded trade carried out by hedge funds called the basis trade. Hedge funds use highly levered amounts of money to go long Treasuries and short swap spreads as a result of perceived mispricing. This trade has worked well during times of orderly Treasury market action. When conditions become disorderly, however, and investors need to sell Treasuries to raise money, then prices drop (interest rates rise) which hurts the long end of the trade and, at the same time, there becomes a lot of buying of SOFR swaps which pushes their prices up as the basis trade gets closed out. Hedge funds end up losing money on their long Treasury positions as well as on their short swap positions. Treasury selling leads to more selling which can lead to a very rapid rise in long-term interest rates in a short period of time which happened last week.

Just when mortgage rates were seemingly starting to settle down in the low 6% range, they have shot up again with the spike in 10-year Treasury yields.

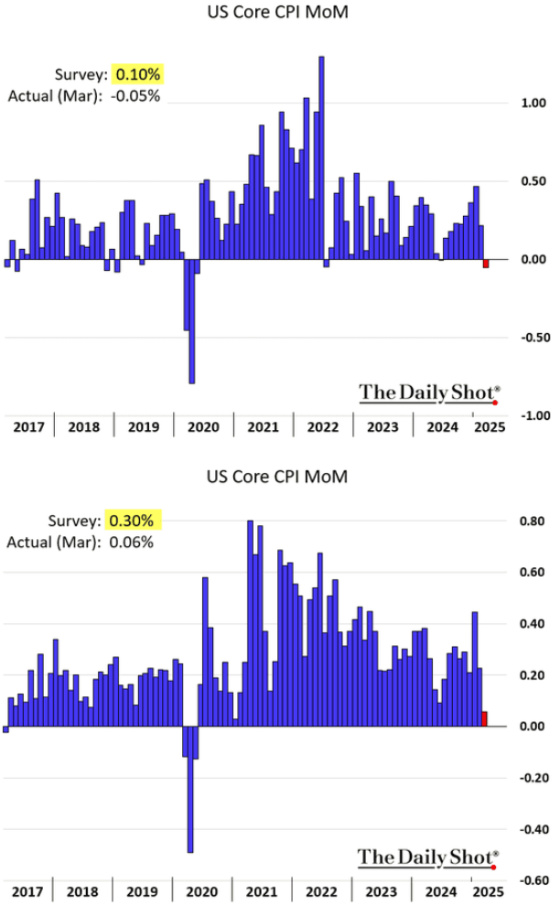

The rise in rates has taken place despite a meaningful moderation in CPI.

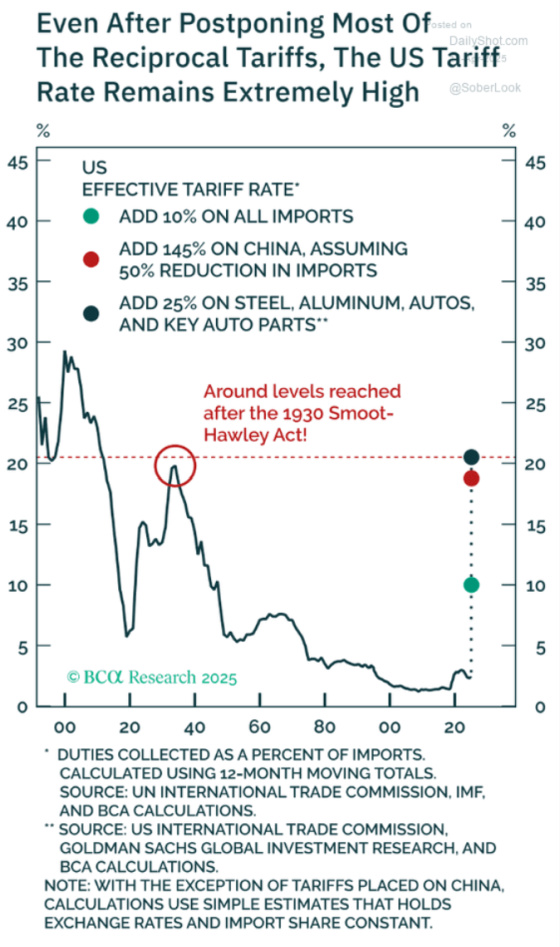

It’s no wonder that inflation expectations are rocketing higher for everyone except Republicans given how high tariffs will be even after the 90 day pause.

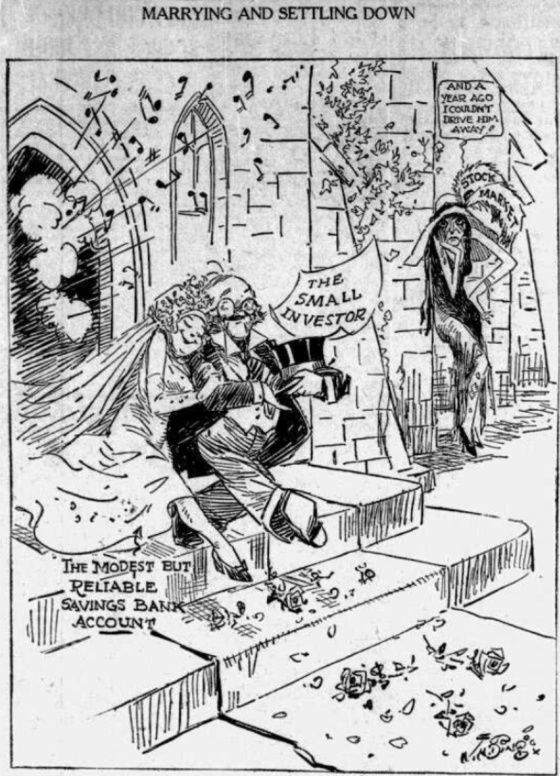

I’m not sure when the name of the 1930 legislation imposing much higher tariffs switched but it was originally known as Hawley-Smoot, and not Smoot-Hawley as it is referred to today. This article is from June 19, 1930 and shows the negative tone towards tariffs even back then.

Even back then there was skepticism as to their effectiveness. There was also concern as to whether tariffs would end up having the opposite effect.

From what I have read, the Treasury Secretary is a strong believer that China’s mercantilist strategy has had a detrimental effect on the United States economy and social order. It turns out that he was heavily involved in George Soros’ fund breaking the Bank of England in 1992 and generating a $1 billion trading profit. It appears he may be using the same playbook when it comes to China.

I have read things praising Bessent’s intellect and market knowledge but I must admit that I had to pause after reading this tweet as I have a huge aversion to people who think and act from an ideological perspective. If what he says is true then I now have some deep reservations about Bessent. On the other hand, he knows the importance of stable, trustworthy markets so I also think he will advocate for a much more gradualist set of policies to attempt to regain investor confidence and more orderly liquidity flows.

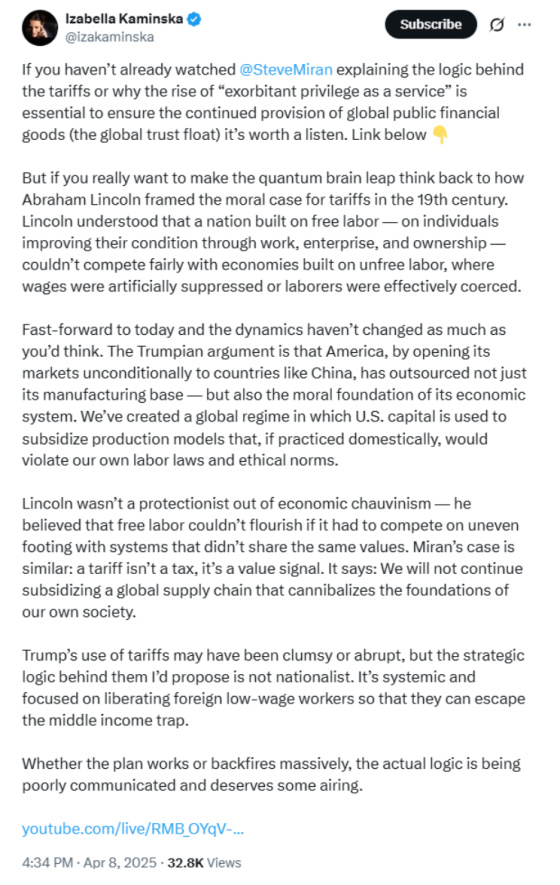

So what is really happening? It appears that Trump and Bessent are heavily influenced by a paper written by Stephen Miran released in November 2024 called “A User’s Guide to Restructuring the Global Trading System”.

Here are the key points:

- The vast majority of global trade is denominated in dollars which means that most countries need to import dollars as their economies grow.

- This leads to dollar appreciation versus local currencies and makes U.S. exports less competitive.

- As the provider of the global reserve currency, the United States has to be the consumer of last resort and absorb excess production from other countries, particularly China.

- Dollar appreciation can lead to financialization of the economy as manufacturing becomes hollowed out. This means the economy becomes more reliant on leverage and financial transactions versus making tangible goods.

- By subsidizing global growth at the expense of the U.S. industrial base it becomes more difficult for the United States to finance the global security umbrella and continue to make provisions to keep the dollar as the reserve currency.

- To skirt previous tariffs China exported goods to other countries and had minor processing done and re-exported those goods to the United States.

- By applying across the board tariffs, countries can then seek tariff relief which can only be granted if they agree to apply tariffs to China so they can’t skirt U.S. tariffs.

- If countries want to be under the U.S. security umbrella they must agree to and adhere to the new U.S. trade protocols. Market access is now a component of U.S. foreign policy.

I thought this take was interesting as well as it discusses the moral and societal aspects of having opened our markets unconditionally to China and other mercantilist countries.

And while I’m quite sympathetic to some of these arguments, I also know that imbalances do not happen overnight. Rather, they build up over decades and the system evolves to accommodate those imbalances which then grow even bigger. There is no way they can be resolved instantaneously by nuking it the way Trump and Bessent have gone about it. There is too much collateral tied to the existing system operating orderly. Currency values, interest rates, the security and liquidity of Treasuries, a global infrastructure of financing, distribution, and employment tied to global trade flows, particularly imports into the United States, are all reliant upon this system continuing to operate in an orderly fashion.

As an example, there are so many car dealers that import foreign automobiles and employ a significant number of people to sell and service those cars. It’s estimated that over 150,000 people are employed by foreign automakers in the United States. Trump’s approach risks eviscerating these businesses if they are forced to dramatically increase their prices beyond the purchasing power of the consumer base. If it’s a discretionary item then people will either not make the purchase or will delay doing so until the price adjusts, their incomes go up, or they cut back on other spending to afford these purchases. Sales and profitability will collapse, jobs will be lost, investment will be curtailed, and this will ripple through the economy.

If all of these dominoes fall then this will 100% be a Trump recession and there is not one thing he can say to make an effective counterargument. It’s hard to pin the Great Financial Crisis on any one individual as well as the Covid economic collapse, but this one will be associated with one person, and one person only, Donald Trump. The Great Depression is very much connected to Herbert Hoover and Donald Trump risks creating a similar association.

I will end this post by sharing a cartoon that was on the same page as the article excerpt I showed above from 1930. It has tremendous applicability today. I have to believe that Warren Buffett’s $334 billion of cash and short-term securities ($284 billion in T-bills) via Berkshire Hathaway must feel quite good to him right now as it should for anyone with a decent amount of personal savings.

{kind=link}

Great post Gary. While I agree that the blame for any recession we have at this point will lay squarely at Trump’s feet, I don’t necessarily agree that it would be 100% his doing. He may be the one that lights the match, but his predecessors prepared the kindling and wood and sprinkled it with kerosine. Time will tell.