Last week I had my annual cardiologist appointment which involves having an echocardiogram and EEG. I have been doing this for a number of years because I had mitral valve prolapse and a corresponding leaky valve which required annual monitoring. For many years the situation was stable until 2020 when the valve started leaking much more than it had been and was starting to enlarge the heart.

I always thought in the back of my mind that surgery was not a matter of if, but when. The when became now in early 2021 and I underwent a very involved robotic surgery to repair the valve. In spite of the very experienced surgeon saying that it was one of the worst valves he had ever seen he was pleased with how the surgery went. Only time would tell if his optimism would translate into sustainably improved heart function.

Fortunately it appears that his optimism was not misplaced as my cardiologist could not have been more pleased with how well my heart was performing. In fact he said that from looking at the images and data one would never know that I had surgery. He said that it’s hard to top perfection but I should continue to keep coming back to see him annually.

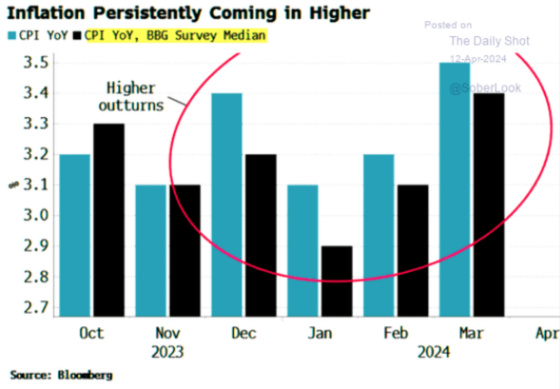

Last week’s CPI report definitely put my improved heart to the test. It rocked the market and reset expectations, yet again, of when the Fed would start lowering rates. It was strong enough to have some pundits like Larry Summers say that the next Fed move should be to raise rates which was not good for my heart.

CPI has been consistently coming in higher than projections as this chart shows.

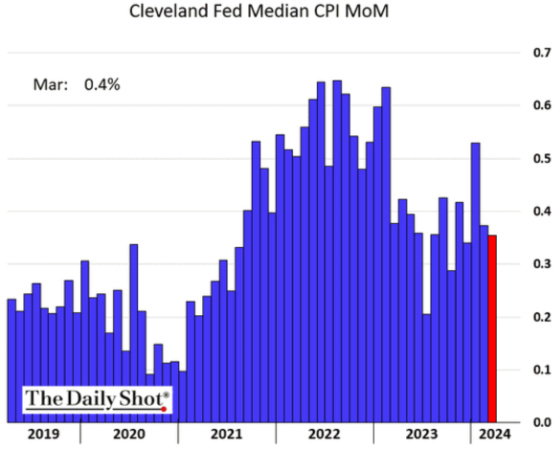

I tend to pay close attention to Median CPI as this doesn’t strip out or overweight any of the inputs to CPI. It calculates the median value each month. Although it has come down from its peak, it is still persistently higher than pre-Covid.

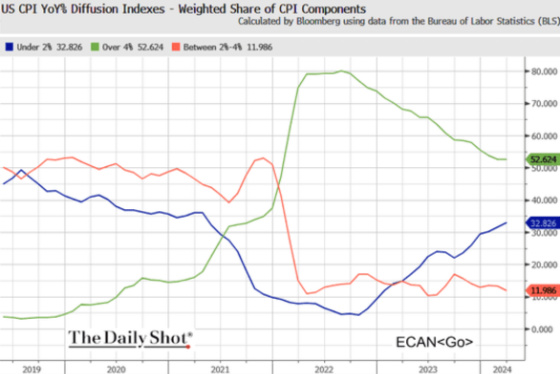

I find this chart interesting as it shows the percentage of CPI components growing at greater than 4%, less than 2%, and those in between.

One can see that those components increasing by more than 4% on an annual basis is coming down but it’s still significantly higher than pre-Covid and the early stages while the sub-set growing at less than 2% is increasing and getting closer to pre-Covid levels. We just need the green line to come down more rapidly and the orange line to get closer to where it was prior to 2022 to get inflation sustainably below 3%.

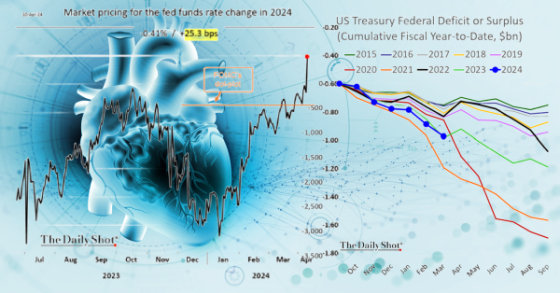

After pricing in 1.60% in rate cuts in January, the market is now only pricing in approximately 0.41% for 2024.

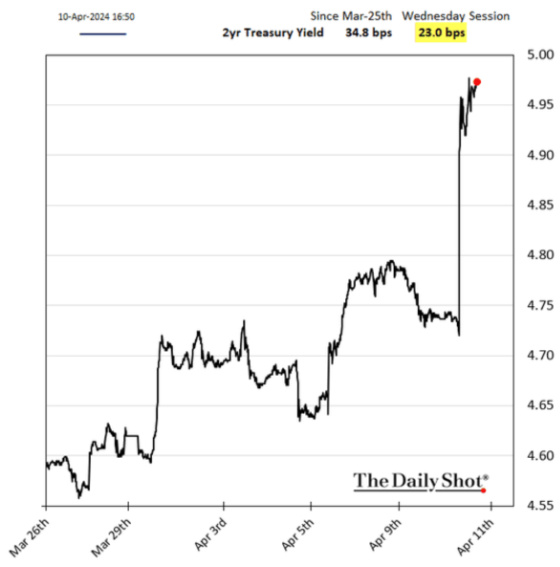

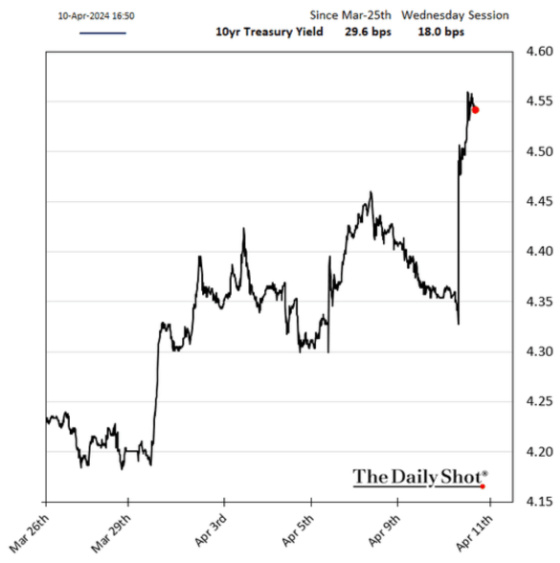

Commensurate with the market lower rate cut expectations, both the 2-year and 10-year Treasury yields shot up.

I have been saying that we are in a different environment that is heavily influenced by fiscal policy, which remains highly stimulative despite a low unemployment rate. This chart shows that the deficit is still quite significant even with the unemployment rate being less than 4%.

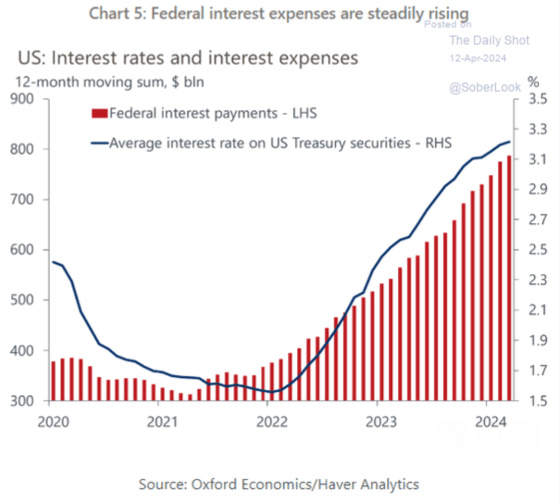

Another source of support for the economy and spending is the much higher risk-free interest income that is flowing to Treasury investors due to the material increase in interest rates. Savers are now really starting to benefit and they now have more income from which to spend if they so choose.

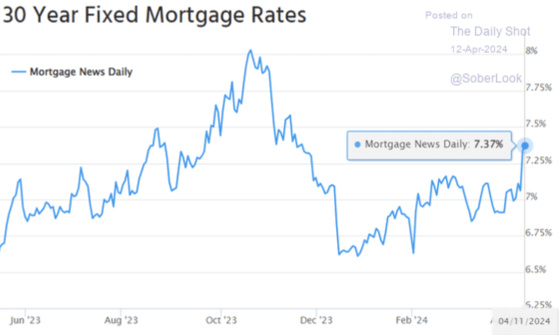

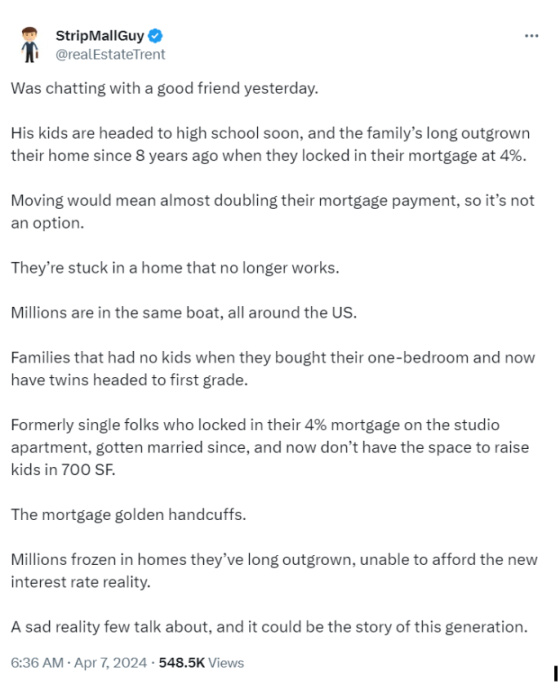

Higher rates are filtering back through to the mortgage market which will make it even more difficult to unfreeze the home buying market as the payment shock to exit a lower cost home that is encumbered by a very low interest rate mortgage to repurchase a much higher priced home utilizing a much higher rate mortgage is too much for many potential home sellers to bear.

I saw this on X which speaks to the challenges the housing market faces.

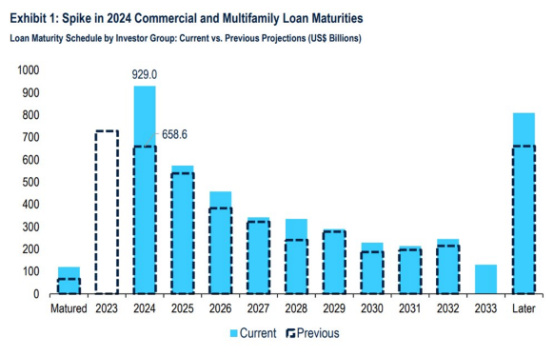

Although I think my heart held up well this week, the rapid rise in rates may cause more stress and heart challenges for borrowers with loans coming due in 2024. As this chart from PGIM Real Estate shows, a large dollar volume of loans had their maturities extended from 2023 to 2024.

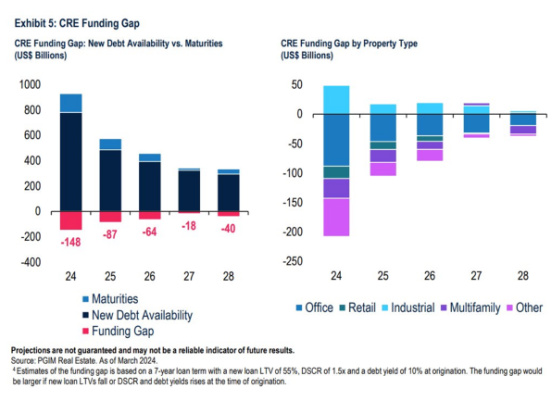

If they are unable to procure additional extensions then there is a material gap between the loan balances outstanding versus what current underwriting standards and interest rates would generate in terms of new loan proceeds. PGIM real estate estimates the funding gap to be approximately $150 billion with apartments representing $50 billion.

Of course if interest rates drop again then the funding gap could shrink materially. As of now, however, I think the underwriting assumptions PGIM is using is in the ballpark and suggests, absent continued loan extensions, apartment owners will either have to access capital from themselves, their investors, or outside parties to deleverage in order to meet the funding gap. And even if borrowers are able to extend their maturities, they may be required to make loan paydowns or post additional collateral so the need for more money may still exist under those circumstances, albeit usually far less than what is required to close the funding gap.

Anyway you look at it, the rise in long-term rates corresponding with the market pricing in fewer Fed rate cuts in 2024 is putting more pressure on the underwriting of loans that are maturing in 2024. At CWS our first major tranche of maturities will hit in the first half of 2025 so we will skirt the 2024 maturity wall. Nevertheless, we are already gearing up to position these properties to be ready to pull the trigger early if rates drop and loan proceeds increase. And if we end up refinancing closer to maturity it is imperative for us to position these properties to have the best execution possible when the loans mature. I’m glad my heart is strong and healthy as I need this to be the case going into a more challenging financing environment. And while we have a fairly smooth 2024, unlike many other property owners, we are acting as if 2025 will be equally difficult.

{kind=link}

Gary great to hear you’re doing well! Scary stuff but you prevailed.

I Been reading your blog for about a year and a half now. In an attempt to learn about multi-family loans.

I come from the wholesale side of mortgage lending.

I enjoy reading your blog it’s a treat for me even if I don’t understand but I’m catching on.

If you have any suggestions I’m all ears, books or maybe one day you will write about the basics of multi-family loans and types.

So again glad you’re still on the planet!