I am a great admirer of those who have the ability and inclination to deconstruct great performance as well as negative ones too. Charlie Munger is famous for inverting. If you want to learn how to live a great life it can be just as valuable to educate oneself on the characteristics and quality of a miserable life.

Tim Ferriss in his tremendous podcasts focuses intently on deconstructing extraordinarily successful people and what has led to their success. The book Mastery, which I highly recommend, does this as well.

Along the same lines, I like when people are able to break down lengthy articles and interviews into important, more accessible components, and deconstruct the arguments and their validity. With this in mind, I thought I would take a shot at doing this with a lengthy interview with Boston Fed President Eric Rosengren by Marketwatch.

Shadowboxing With The Fed

Rosengren believes the Fed should raise rates to pre-empt inflation from overheating as he believes we are near full employment and very close to the Fed’s 2% inflation target. Let’s turn to the interview and deconstruct it. I have deleted portions of the interview that I thought were repetitive or not worthy of commenting on.

MarketWatch: You dissented from the September policy meeting in favor of raising rates. Could you explain why?

Rosengren: The reason I dissented was that I thought when we got to the September meeting, that we were relatively close on inflation to our [2%] target at 1.7% for core PCE, is pretty close to 2%, and that the unemployment rate, which currently right now is at 5%, is relatively close to full employment.

GC: The Fed’s 2% target is a minimum rate of inflation. We are still not there, despite the fact that we are supposedly close to full employment. Perhaps there is more slack in the labor market than is reflected by the unemployment rate or there are other forces at work globally that is keeping inflation muted. It seems presumptuous to think the Fed is behind the curve in terms of its interest rate policy when we are not even at 2% inflation and wage growth is still muted despite a relatively low unemployment rate. Does this chart showing the change in the Fed’s Labor Market Conditions Index suggest an overheating of the labor market? It looks more like it’s presaging a recession if anything .

And while projected future inflation expectations have started to tick up, one can see that they are still lower than they have been over the last 12 years. The market does not seem to be worried about what Rosengren is concerned about.

Rosengren: But the Summary of Economic Projections has people thinking that the federal fund’s rate in the long term will be around 3%. We’re well below that. So if we want to make sure that we stabilize around full employment, and around 2% inflation, we can’t wait.

GC: Since when have the Fed’s projections have any credibility? They have continuously overestimated growth and inflation and, correspondingly, interest rates.

Rosengren: There was another feature of the dissent, which I think was important, which is thinking about the risks. So my concern was, that if we wait too long, that we will overshoot what I think is a sustainable level of unemployment. And that will result in both potentially higher inflation, potentially higher asset prices, and that we would start reacting to that and we would no longer have the flexibility to move gradually. And I think if we start moving more quickly, and possibly have to do more, that we might very well overshoot on our monetary policy response, and if we did that, we might actually shorten the recovery rather than lengthen it.

GC: This seems to me he is shadow boxing ghosts. Monetary policy is a blunt instrument and from my perspective, the burden of proof should be on seeing inflation materialize after so many years of it being dormant versus taking preemptive action which can cause a fairly significant tightening of financial conditions that can spill through into the real economy.

Rosengren: So the way I would think about it is that I think that there is a cost to overshooting and as we get closer and closer to where our target is, there is going to be more of a cost if we overshoot. Historically, we haven’t been very good at leveling off at full employment, either from above or below. So if you look at the unemployment rate it is kind of a wave, and it doesn’t stabilize around where our estimates are of full employment. My own estimate is 4.7% [unemployment rate], the committee’s 4.7%-5%, so I’m at the low end, but ideally I’d like to stabilize right within that band and I’d prefer not to go way below that and I certainly don’t want to go way above it. And I think the best way to do that is to slowly remove our accommodation so that we are able to stay within that band.

GC: More shadowboxing.

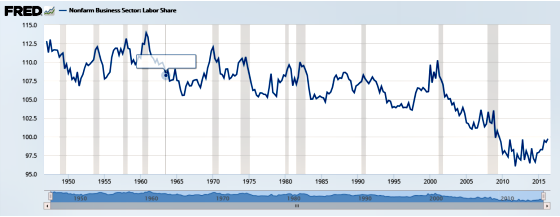

Does labor look like it has a lot of bargaining power over business? Yes, its share of nonfarm business output is growing but from a very low base.

And this has carried over to improved wage growth but this too is still at levels that do not suggest the labor market is getting overheated. This is just what the economy needs. There is a deficiency in aggregate demand because labor’s share of economic output is so low. Wage growth can help improve this situation. It shouldn’t be something to fear given the low labor share of output.

![]()

MarketWatch: But growth has been consistently disappointing. The Fed has had to cut its forecast for growth this year.

Rosengren: So the economy was certainly weaker in the first half of the year than we were anticipating. So if you look back to the beginning of the year, we raised rates last December, nothing really happened for the first two weeks and then we got into January and people became concerned about whether China would grow as fast as people were anticipating. And we started to see stock markets around the world go down fairly appreciably and so people downgraded their forecasts.

GC: I would argue that much of the carnage in the stock and bond markets during this time was a result of the tighter financial conditions that resulted from the Fed raising rates. Namely, the higher dollar and how this rippled through to emerging markets and export-oriented multi-national firms. Risk aversion took hold and credit spreads widened and capital became harder to come by. China had to take some drastic actions to defend its currency.

The following graph shows how the dollar appreciation that took place between 2014 and early 2016 bled over into a significant widening of high yield bond spreads which resulted in much tighter financial conditions. All of this took place because of the Fed telegraphing that higher interest rates would be coming. And what happened? Only one increase in the federal fund’s rate has taken place. Since then the Fed had backed off a bit which led to some dollar depreciation and a fairly remarkable compression in high yield spreads. The point of all of this is that the market is very fragile and just a hint of the Fed being more aggressive than what the market has priced in for future rate increases sends it into a tizzy fit.

Rosengren: And so if we get a situation where an event from abroad causes us to reevaluate what we think is actually going to happen, we should take that into account, we shouldn’t ignore new data. And I didn’t anticipate the Brexit vote was going to go the way it did, but it did. When something like that happens, we should take that into account as well. I’m not expecting a China or a Brexit to occur in the next three or four months. So, yes, we were surprised at the beginning of the year, and our forecasts were for things to be a little bit stronger. There are big errors around our ability to forecast. So we need to be relatively humble. But we still have to make our best guess as to what we think things will be going forward. The problems abroad were not that easily forecast. In December, I don’t think we were expecting the kind of slowdown that we saw both in the United States and globally. Brexit was a little bit easier to anticipate. And I think some of the worst of the negative impact actually didn’t occur. So in that circumstance, it was a legitimate concern to worry about Brexit. It turned out not to be as big an outcome as some people were worried about.

GC: I appreciate the humility and his recognition that the United States is no longer an island and that we must take into consideration what is occurring around the world and how it may impact our economy. I don’t think he appreciates or acknowledges the feedback effect that Fed policy can have on the world and boomerang back to us. The dollar impact of Fed policy is real and the Fed must take this into consideration.

MarketWatch: You mentioned asset prices. Could you explain to our readers what your concerns are?

Rosengren: On the stock market, the P/E looks a little bit elevated but is not out of the norm of historical experience. If you look at price-to-rental rates for residential real estate, they don’t look outside the norm of what we’ve seen historically. The two financial market prices and asset prices that look a little unusual relative to historical experience is the 10-year Treasury rate and commercial real estate. So both of those are asset classes that look like they are a little bit different than what we’ve seen in historical experience. So I am monitoring that quite closely and I think that is something that we should watch.

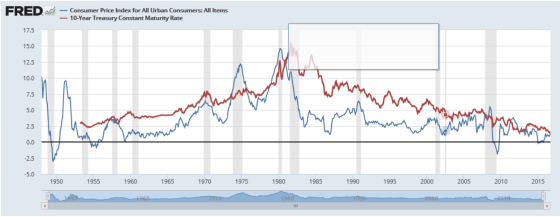

GC: I think the following chart should explain most of the drop in 10-year Treasury yields that has been taking place since 1981: Declining inflation. It seems pretty simple to me and nothing to worry about. The world now has approximately $12 trillion in negative yielding debt, leaving the U.S. rates among the highest in the developed world. It is the most liquid market in the world so I would be hard pressed to call it a bubble.

He mentions commercial real estate being elevated relative to historical trends. There is definitely a correlation between the low long-term interest rates about which he expressed concern and real estate prices as real estate investors often utilize leverage to finance the purchase and development of commercial property and apartments. Thus, borrowing costs will impact how real estate is valued.

Real estate is also impacted by credit conditions more generally of which the risk-free rate is one component. Other variables are the spreads over that risk-free rate, how much debt service coverage is required, maximum loan to values, fees being charged, and covenants levied. The stock market and residential real estate are not immune to the 10-year Treasury yield and they are seemingly fairly valued. Commercial real estate has without question appreciated meaningfully but the spread between cap rates and interest rates is still at historically high levels, therefore offering investors a potential cushion against rising rates.

The following chart shows that commercial real estate spreads are historically elevated and have been higher than average since the recovery took hold. This does not look frothy to me.

And it appears that construction lending is tightening for commercial real estate developers. This is definitely the case for apartments.

Loan delinquencies don’t seem to be an issue but that is the case late in the cycle. They’re not a problem until they are a problem. Nevertheless, they are at very healthy levels currently.

MarketWatch: On commercial real estate — isn’t it a small sector of the economy?

Rosengren: It is not that small a sector. So in one of my earlier talks, I actually showed the flow of funds, roughly a trillion and a half [dollars] in the banking sector, I guess it depends on what you think is big, but by my estimate, a trillion, and a half is pretty big. And I think one reason why some people are not concerned is that it is not all in the largest banks. So it is distributed among kind of community banks, mid-sized banks as well as some of it in large banks. But it is a big enough asset class that is held by leveraged institutions. It has been a problem historically. So in the late 1980s and early 1990s, we had a commercial real estate problem in New England that affected not only New England but the mid-Atlantic and the West Coast. Abroad we have seen instances where commercial real estate exacerbated recessions, such as in the Nordic countries. So we’ve had enough historical experience in the past that I think it is worth paying attention to and making sure it doesn’t get too out-of-hand.

GC: I have no issue with his response. One can see that this sector has grown fairly rapidly from a lending standpoint over the last two years after dropping and plateauing.

MarketWatch: About the bond market, that’s a global market. Aren’t yields low because of a flight-to-safety from overseas?

Rosengren: So I would call it more a reach-for-yield than a flight-to-safety. So that is one of the many factors that affect the 10-year Treasury rate.

GC: What evidence does he have to support his assertion? U.S. Treasuries are some of the most liquid and safest instruments in the world so when people buy them it’s usually more for safety than speculation or reaching for yield.

I guess you can say, when all is said and done, I’m more in the Janet Yellen camp that we should let the economy run hotter and see the whites of the eyes of inflation before tightening monetary policy even more than it has been. And yes it has been tightened. It may be loose by historical standards, but it is far less loose than it was.

From my perspective, the burden of proof is on the Fed members that want to raise rates to have stronger arguments than we need to have more bullets in the chamber when the next recession comes or that we may lose control of inflation if we don’t act now. Taking action now could bring about what these members fear: a recession with short-term interest rates near 0% and there is very little evidence that labor has the power to induce a wage-price spiral, particularly when one overlays the global competitive dynamics and a very slow-growing labor force not only here, but even more dramatically so around the world. Finally, with housing costs representing a large component of CPI and these costs rising relatively rapidly due to rising rents, raising interest rates can actually serve to curtail housing supply, as higher rates make it more costly for apartment builders and therefore requires even higher rents to justify new construction. In addition, should higher short-term rates translate to higher long-term rates, then this will impact the mortgage market and spill over to the demand for single-family homes as well, Mr. Rosengren, please check your paranoia at the door before the next Fed meeting.

Over to You:

Do you feel that the burden of proof is on the Fed? Where are interest rates headed?

{kind=link}

Leave a Reply