Howard Marks, the billionaire co-founder of Oaktree, is considered to be one of the world’s most thoughtful and successful investors. He is famous for his lengthy and well thought out memos articulating his deep thinking and how it applies to investing. He is particularly interested in and astute about risk and how to manage it. His most recent memo goes into great detail about the various ways of categorizing risk and how investors and firms should look realistically at what can and cannot be measured and controlled. Marks says the following in his memo:

“Simply put, risk is low when risk aversion and risk consciousness are high and high when they’re low.”Click To Tweet

Because there is no single formula to measure risk it requires the management of it to be handled internally and not delegated to outsiders or financial models. Every participant in the investment process should be engaged in evaluating and managing risk and everyone should rely on their experience, judgment, and knowledge and not financial and statistical models. In addition, risk management should be constantly applied versus on an ad hoc basis as many individuals and firms are prone to do.

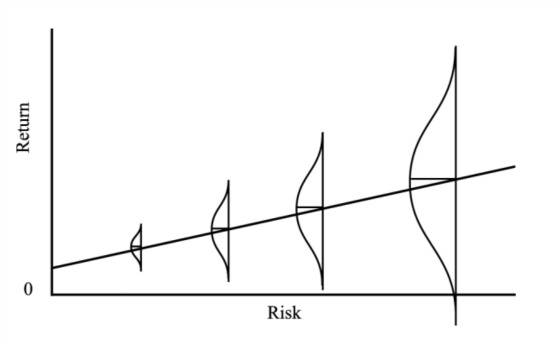

One of the great contributions to the memo is the following graph. Most graphs depicting Risk and Return show returns growing as more risk is being borne. Marks’ more accurately (and realistically) shows how returns can grow with more risk but so does the range of outcomes, both good and bad.

Source: Oaktree Capital Management, L.P.

To save you time if you’re not inclined to read the entire memo, I have summarized each of the 24 types of risks he identified. They are as follows:

24 Types of Risk

- Losing money – The possibility of permanent loss is the main form of risk.

- Falling short – Not having to make necessary payouts or income to live on.

- Missing opportunities – Not taking enough risk.

- FOMO (Fear of Missing Out) – Jumping on the bandwagon of risky investments for fear of living with envy.

- Credit – The risk that a borrower will be unable to pay interest and repay principal as scheduled.

- Illiquidity – The inability to sell when you need the money.

- Concentration – The risk of not being diversified when sectors drop in value.

- Leverage – Losses are magnified when investments decline in value by using borrowed money.

- Funding – The need to make a capital call when a loan comes due.

- Manager – The risk of picking the wrong one.

- Overdiversification – The standards of inclusion may drop leading to the potential of lower risk-adjusted returns.

- Volatility – This introduces an emotional component that may result in a permanent loss from selling too soon.

- Basis – This applies to arbitrageurs who go long one security and short another based on one being cheaper than the other and common patterns repeating themselves and yet something goes awry where the relationship breaks.

- Model – Excessive belief in a model’s efficacy can lead to excessive risk taking.

- Black Swan – Just because something hasn’t happened doesn’t mean it won’t happen. This is the statistically inconceivable event that materializes.

- Career – If rewards are shared asymmetrically then it may not be in a money manager’s best interest to take risks where there could be short term pain, but long-term pain for fear of losing clients or his or her job.

- Headline – This is when losses are big enough that they can potentially generate media attention.

- Event – Tends to apply to bondholders when the equity owners leverage up the company and put the bonds at more risk.

- Fundamental – Assets or companies underperform in the real world.

- Valuation – Overpaying for an investment.

- Correlation – Being less diversified than expected. Everything goes down much to the surprise of an investor.

- Interest Rate – The risk that higher rates can lower the value of fixed income securities and other yield-oriented investments.

- Purchasing Power – The risk that cash received in the future will be eroded in value due to inflation.

- Upside – The risk of being under-exposed to very good economic and financial events that occur in the future.

This is a pretty comprehensive list and a great checklist to have handy to review when contemplating making an investment and the reasons for it as well as evaluating current investments and whether they should be sold or not. Obviously, a number of these overlap and can be magnified when combined with each other. The point is is that risk needs to be thought about quite comprehensively, continuously, and vigorously. At the end of the day, as Marks says:

“Loss occurs when risk – the possibility of loss – collides with negative events.”

Investors need to be cognizant of what can create the possibility of loss and give serious thought to the timing and magnitude of negative events unfolding.

“When clouds appear wise men put on their cloaks.” – Shakespeare

{kind=link}

Leave a Reply