Rather than laboriously going through the Fed statement released after it cut rates by 25 basis points last week, along with Jay Powell’s key statements at his press conference, I thought I would turn to one of my A.I. assistants to produce an analysis of what was said and how investors reacted to last week’s move. After all, great answers can only result from great questions so hopefully my query is such that what follows is an analysis you find helpful, informative, and interesting.

Fed’s December 2025 Rate Cut: A Divided Committee Navigates Dual Mandate Tensions

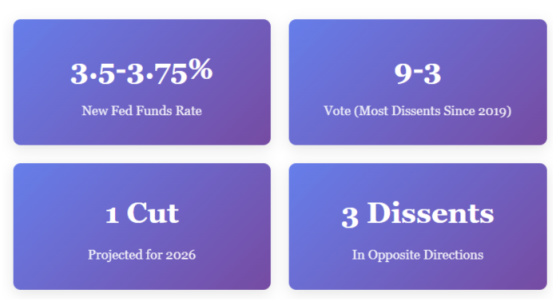

Key Takeaway: The Federal Reserve delivered its third consecutive rate cut on December 10, 2025, lowering rates to 3.5%-3.75%, but revealed unprecedented division with three dissenting votes—the most since September 2019—as policymakers grapple with competing pressures from weakening employment and elevated inflation driven primarily by tariffs.

In a decision that laid bare the deepening rifts within the Federal Reserve, the central bank cut interest rates by 25 basis points on December 10, 2025, but only after an unusually contentious debate that produced three dissenting votes pointing in opposite directions. The split decision—which Chair Jerome Powell acknowledged was a “close call”—crystallizes the Fed’s dilemma as it attempts to support a faltering labor market while inflation remains stubbornly above its 2% target, largely due to President Trump’s tariffs.

The Decision: A Quarter-Point Cut Amid Historic Disagreement

The Federal Open Market Committee voted 9-3 to lower the federal funds rate by 25 basis points to a target range of 3.5% to 3.75%, marking the third consecutive cut and bringing the total easing since September to 100 basis points. But the headline number masks a remarkable level of internal discord that threatens to complicate future policy decisions.

The dissenting votes came from three dramatically different perspectives. Chicago Fed President Austan Goolsbee and Kansas City Fed President Jeffrey Schmid both voted against the cut, arguing that rates should remain unchanged given elevated inflation. Meanwhile, Fed Governor Stephen Miran dissented in the opposite direction, advocating for a more aggressive 50-basis-point reduction to address deteriorating labor market conditions. This three-way split represents the most divided the Fed has been since September 2019.

What the Fed Said: Elevated Risks on Both Sides

The official FOMC statement reflected the committee’s balancing act, acknowledging that economic activity has been expanding at a moderate pace but noting significant risks emerging on both sides of its dual mandate.

“Available indicators suggest that economic activity has been expanding at a moderate pace. Job gains have slowed this year, and the unemployment rate has edged up through September. More recent indicators are consistent with these developments. Inflation has moved up since earlier in the year and remains somewhat elevated.”

— Federal Reserve FOMC Statement, December 10, 2025

Critically, the statement noted that “the Committee is attentive to the risks to both sides of its dual mandate and judges that downside risks to employment rose in recent months.” This language shift signals growing concern about labor market weakness, even as inflation persists above target.

Powell’s Press Conference: “It’s Really Tariffs“

Chair Jerome Powell‘s post-meeting press conference provided crucial context for understanding the Fed’s predicament. His comments revealed a central bank caught between competing priorities, attempting to support employment while inflation—driven primarily by policy factors outside the Fed’s control—remains elevated.

“Everyone should understand, and the surveys show that they do, that we’re committed to 2 percent inflation and we will deliver 2 percent inflation. But it’s a complicated, unusual, difficult situation where the labor market is also under pressure, where job creation may actually be negative.”

— Chair Jerome Powell, December 10, 2025

Powell’s Key Messages: Five Critical Themes

- Tariffs Are Driving the Inflation Overshoot: In his most pointed comments, Powell directly attributed elevated inflation to President Trump’s trade policies, stating flatly: “It’s really tariffs that’s causing most of the inflation overshoot.” He noted that away from tariffs, inflation would be in the low 2s, much closer to the Fed’s target.

- Job Growth May Already Be Negative: Powell revealed a startling assessment that caught many by surprise: actual job creation in the U.S. may already be negative, despite unemployment remaining relatively stable. He explained that an overcount in payroll numbers and declining labor supply are masking underlying weakness.

“There is an overcount in the payroll job numbers, we think. I think a world where job creation is negative, I think we need to watch that situation very carefully, and be in a position where we are not pushing down on job creation with our policy.”

— Chair Jerome Powell on labor market concerns

- “We Can Wait and See”: Despite cutting rates, Powell emphasized that the Fed is now positioned to adopt a more cautious stance going forward. With 100 basis points of cuts already delivered, he repeatedly stressed that policymakers can afford to be patient and assess incoming data.

- One Tool, Two Problems: Powell acknowledged the fundamental challenge facing the Fed: “You have one tool. You can’t do two things at once.” This stark admission underscores why the committee is so divided—monetary policy cannot simultaneously address weak employment and elevated inflation without favoring one mandate over the other.

- Next Move Won’t Be a Rate Hike: When asked whether the Fed’s next move could be a rate increase, Powell was emphatic that despite historical precedent, this easing cycle is different. “I don’t think that a rate hike is” the next move, he stated, closing the door on near-term tightening.

The Dot Plot: Only One Cut Expected in 2026

The Fed’s Summary of Economic Projections revealed that policymakers expect to deliver only one additional quarter-point cut in 2026, unchanged from the September forecast. This projection suggests the Fed believes it has done most of the heavy lifting on rate cuts and expects to hold rates relatively stable as it assesses the economic impact of both its easing and the Trump administration’s policies.

Fed Rate Projections: 2025-2027

The median projection for the longer-run neutral rate remained at 3.0%, suggesting structural changes in the economy may require permanently higher rates than the pre-pandemic era. This implies the Fed sees limited room for additional easing without risking a reacceleration of inflation.

The Quantitative Tightening Pivot: Balance Sheet Stabilizes

While the rate cut garnered most headlines, an equally significant development occurred just nine days earlier: the Federal Reserve officially ended its quantitative tightening program on December 1, 2025. This marked the conclusion of the largest balance sheet reduction in Fed history and represents a fundamental shift in monetary policy stance.

Major Balance Sheet Policy Shift: After draining $2.4 trillion from the financial system since June 2022, the Fed stopped reducing its balance sheet on December 1, 2025. The Fed is now reinvesting proceeds from maturing Treasury securities rather than letting them roll off, stabilizing the balance sheet at approximately $6.5 trillion—still about 60% above pre-pandemic levels.

Why the Fed Stopped QT:

The decision to end quantitative tightening came as bank reserves approached levels the Fed considers minimally “ample” for maintaining orderly money market conditions. At around $2.9 trillion, reserves were nearing the threshold that triggered funding market stress during the 2019 repo crisis, prompting policymakers to act preemptively.

The October FOMC meeting minutes revealed that “nearly all” participants supported ending QT on December 1, with only Governor Miran dissenting in favor of ending it immediately at the October meeting. This broad consensus stood in contrast to the sharp divisions over interest rate policy.

While the Fed has stopped reducing Treasury holdings, it continues to allow mortgage-backed securities to run off at $35 billion per month, gradually rebalancing the portfolio toward Treasury securities. This strategy addresses longstanding criticism that large MBS holdings distort housing market credit allocation.

What Ending QT Means:

Ending quantitative tightening removes a significant source of upward pressure on interest rates and improves liquidity conditions in financial markets. However, this does not constitute quantitative easing or a return to large-scale asset purchases. The Fed is simply no longer draining liquidity from the system—a neutral stance rather than an accommodative one.

Market analysts note that stabilizing the balance sheet should reduce volatility in funding markets and potentially ease long-term Treasury yields by eliminating the Fed as a net seller of government securities. This complements the rate cuts by ensuring smoother transmission of monetary policy through financial markets.

Market Reaction: Stocks Rally on Dovish Signals

Unlike the December 2024 meeting that triggered a market rout, the December 2025 decision produced a decidedly positive reaction as investors focused on the dovish elements of the Fed’s message rather than the internal divisions.

📈 Market Performance on December 10, 2025:

- Dow Jones Industrial Average: Surged 497.46 points (1.05%) to close at 48,057.75

- S&P 500: Gained 46.17 points (0.68%) to finish at 6,886.68, just shy of its October record high

- Nasdaq Composite: Rose 77.67 points (0.33%) to 23,576.49

- Russell 2000: Small-cap index jumped 1.3% to a record high, benefiting from lower borrowing cost expectations

Market Reaction: December 10, 2025 Close

Why Markets Rallied Despite Fed Divisions:

Several factors contributed to the positive market response. First, Powell’s explicit statement that the next move won’t be a rate hike reassured investors worried about premature tightening. Second, the revelation that tariffs—not underlying economic strength—are driving inflation suggested the Fed could continue cutting if trade policy stabilizes.

Third, the Summary of Economic Projections featured stronger growth forecasts and lighter inflation expectations than many feared, supporting a bullish narrative. Finally, ending quantitative tightening on December 1 removed a key source of market uncertainty and improved liquidity conditions.

Ryan Detrick, chief market strategist at Carson Group, captured the sentiment:

“Powell got out his three wood and hit it right down the middle. The market got the cut it wanted and although a January cut isn’t the base case, by no means did they put cold water on that potential move.”

The Underlying Challenge: Government Shutdown Distorts Data

Adding to the Fed’s difficulties, the ongoing federal government shutdown—now in its 43rd day—has severely disrupted the collection of key economic data. The unemployment report for October is unavailable, and the November employment data scheduled for release on December 16 may be unreliable or delayed.

⚠️ Data Uncertainty Complicates Fed Decisions:

The government shutdown is creating significant blind spots for Fed policymakers. Without reliable employment data, the Fed must rely on alternative indicators and anecdotal evidence to assess labor market conditions. Powell acknowledged this challenge, noting that December data “may be distorted” by the shutdown’s effects.

The shutdown is estimated to subtract 0.2% from GDP growth each week it continues, with approximately 750,000 federal workers going without pay and additional contractor furloughs adding to the economic drag. This compounds the difficulty of assessing whether job market weakness is cyclical, structural, or shutdown-related.

What This Means for 2026 and Beyond

The December meeting leaves the Fed in a precarious position heading into 2026. With only one additional cut projected for the year and mounting evidence of labor market deterioration, the central bank may face pressure to ease more aggressively if employment conditions continue weakening. However, persistent tariff-driven inflation limits the Fed’s room to maneuver without risking its credibility on price stability.

Looking Ahead: Markets currently assign roughly 70% odds that the Fed will pause at its January 27-28 meeting, digesting the cumulative impact of 100 basis points of cuts. The path forward will depend heavily on whether the government shutdown ends, how labor market data evolves, and whether the Trump administration’s trade policies stabilize or intensify.

The unprecedented three-way split among Fed officials suggests future decisions may become increasingly difficult. If data shows further labor market deterioration, hawks like Goolsbee and Schmid may feel pressure to support additional cuts despite inflation concerns. Conversely, if inflation remains elevated, doves like Miran may struggle to build support for more aggressive easing.

The Bottom Line

December’s rate cut will be remembered not for the 25-basis-point reduction itself, but for what it revealed about the Fed’s internal divisions and the complex policy environment it faces. The committee delivered accommodation to support the labor market while simultaneously stabilizing its balance sheet and signaling caution about further easing—a carefully calibrated package designed to address competing pressures.

Powell’s candid acknowledgment that “you have one tool, you can’t do two things at once” captures the fundamental dilemma. The Fed cannot simultaneously combat tariff-driven inflation and support a weakening labor market without making difficult trade-offs. The three-dissent vote underscores these tensions, with officials genuinely divided about which mandate deserves priority.

The end of quantitative tightening provides some relief by improving market liquidity and easing financial conditions without requiring further rate cuts. But with inflation still elevated, employment potentially turning negative, and critical economic data unavailable due to the government shutdown, the Fed faces one of its most challenging policy environments in recent history.

“We are well-positioned to wait to see how the economy evolves. It’s a very challenging situation. A very large number of participants agree that risks are to the upside for unemployment and to the upside for inflation.”

— Chair Jerome Powell, acknowledging the dual-sided risks

For markets, borrowers, and the broader economy, the message is clear: the Fed has delivered significant easing but is now entering a data-dependent waiting period where future moves remain highly uncertain. The next few months of economic data—if the government reopens and collection resumes—will determine whether the Fed resumes cutting, pauses for an extended period, or faces the uncomfortable scenario Powell insists won’t happen: raising rates again.

{kind=link}

So, what is the likely outlook for long-term interest rates? The Fed has less influence on them and the most likely 2026 Fed actions are to do NOTHING! I think that we need to place more focus on the labor market. My guess is that there remains a substantial level of Biden’s obligated funds for infrastructure and there is also an increasing AI investment. However, it’s not clear to me that the skills available in unemployed labor is a good match with what is needed to fill these labor demands. My guess is that there will be a modest decline in employment and that the Fed cannot do anything to alleviate it. All issues aside, the housing market would benefit from a decline in interest rates and the Fed should attempt to aid that. Chuck