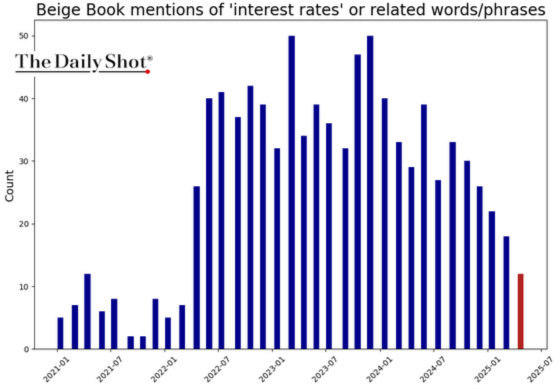

I can’t believe I’m saying this but I kind of miss the days when interest rate concerns were at the forefront of investor concerns, including mine.

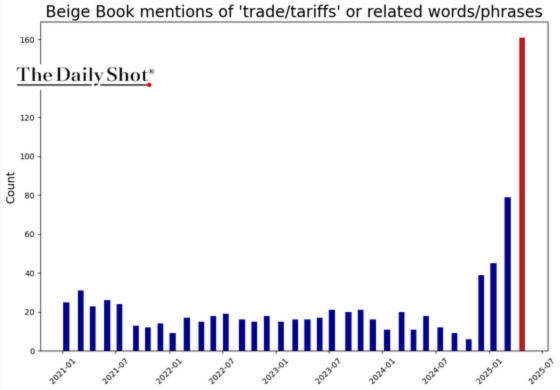

Now it’s been replaced by trade and tariff fears.

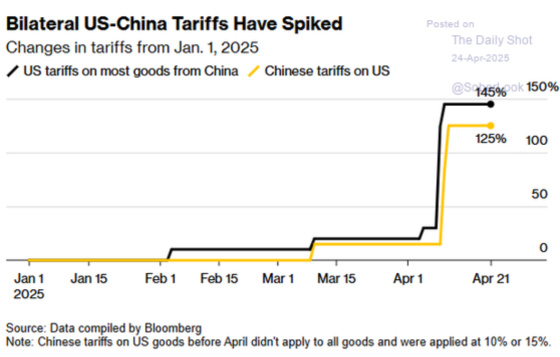

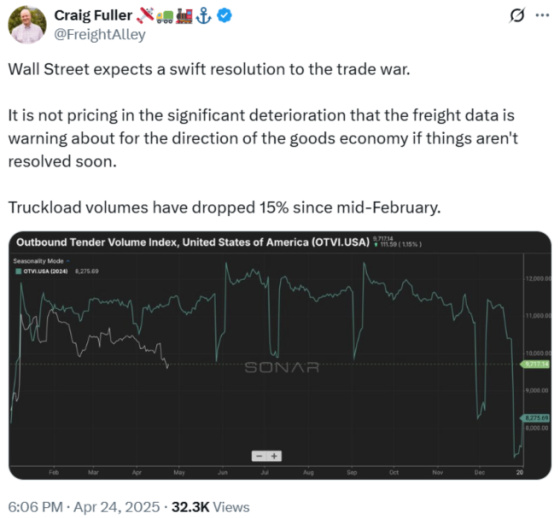

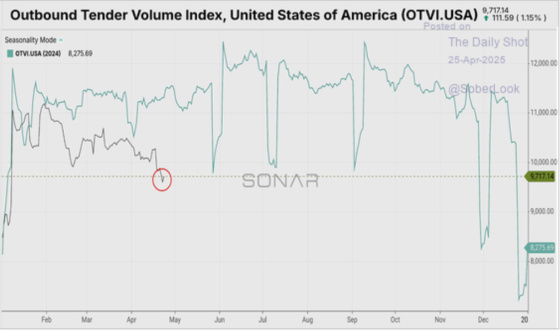

It’s not surprising given this chart. If this isn’t a stark depiction of a trade war then I don’t know what is. Perhaps it’s only a skirmish that will quickly simmer down but immense damage has already been done.

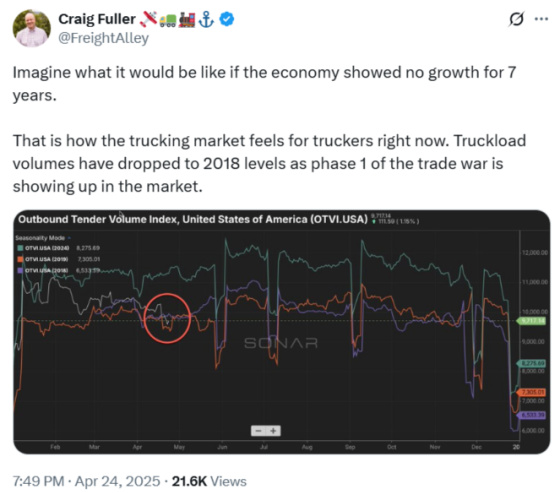

Craig Fuller is well worth following on X to get real time information about what is happening in the trucking and logistics world. Not surprisingly, the news is not good.

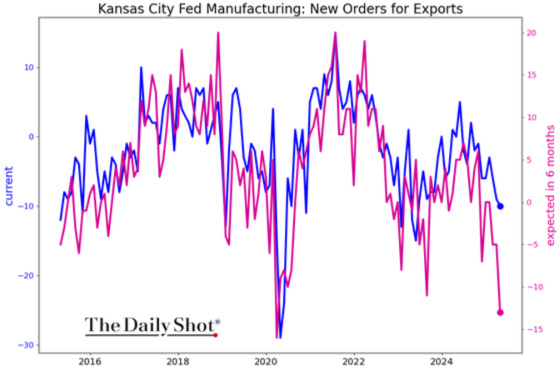

Given the increase in tariffs levied on U.S. goods and foreign disdain for Trump’s treatment of our allies, there is also a patriotic component to boycotting U.S. goods. As a result, the outlook for exports has deteriorated sharply.

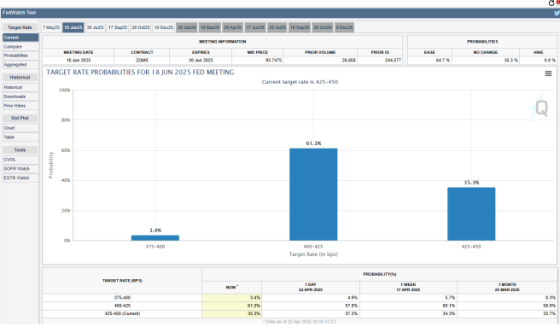

From a CWS perspective cuts in short-term rates would be helpful given our exposure to variable rate loans. I have been saying for a long time now that all roads lead to the job market. Until jobs start to roll over, we won’t see meaningful cuts. One Fed governor is explicitly mentioning the risk to the job market as being his most immediate concern such that he would be in favor of cutting rates if weakness materializes. A second is looking more broadly at overall economic weakness to justify a June cut. Either way, the Fed is preparing the markets for rate cuts ahead.

![]()

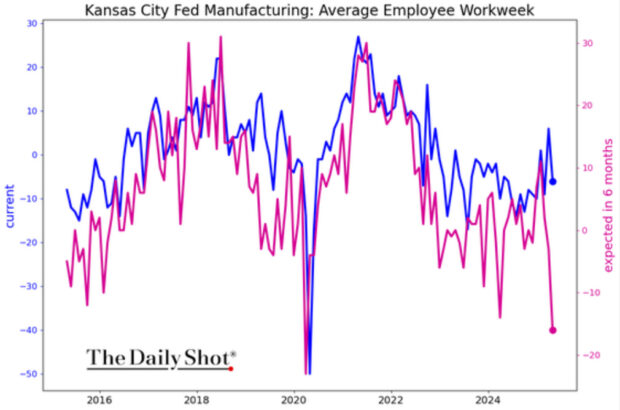

If the outlook for manufacturing employment in the midwest is any indication of future prospects for the employment market, then the Fed will definitely be cutting.

The market is forecasting a 0.25% rate cut by the Fed after its June meeting. The probabilities of a cut have remained well above 50% for the past month.

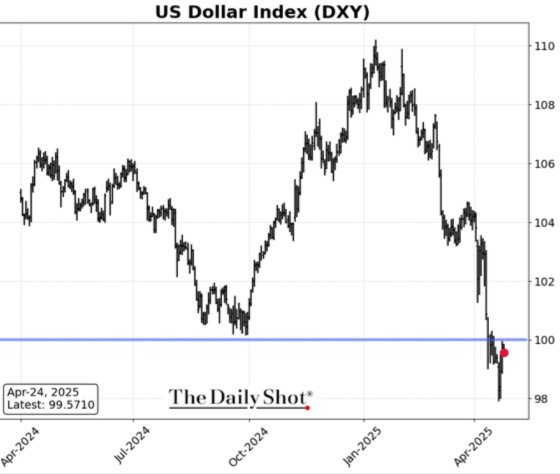

As the U.S. has approached not just an America First policy, but one that can also be perceived as America Only, the perception of the United States being the anchor of international economic stability and a proponent of stronger global ties is waning. This has led to dollar depreciation as investors want less exposure to the United States since Trump is perceived as having a more nationalistic economic policy that may not always be very investor friendly.

U.S. companies with a meaningful percentage of their sales from overseas benefit from a weaker dollar as their foreign currency revenues become worth more in dollar terms. This is being reflected in their share prices.

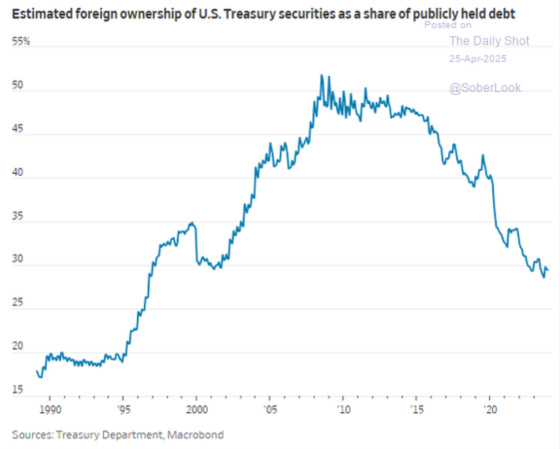

There is some understandable concern that the Trump administration’s more hostile approach to other countries, especially our historical allies, may lead to foreigners dumping Treasuries. This fear appears to be overblown given that foreign ownership of U.S. Treasury securities has been coming down steadily in terms of its percentage of all publicly held debt.

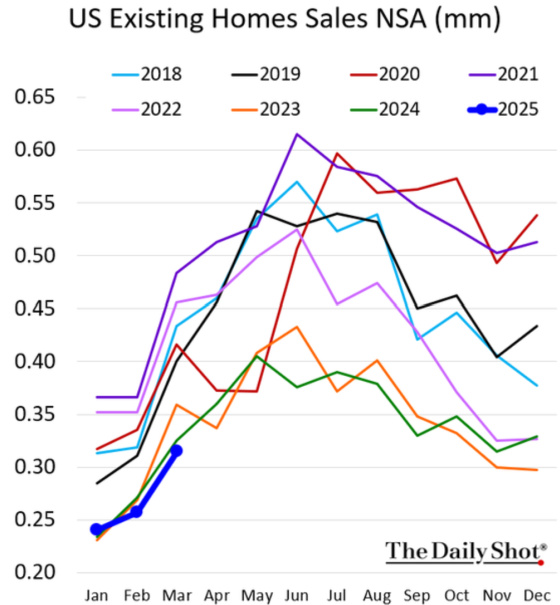

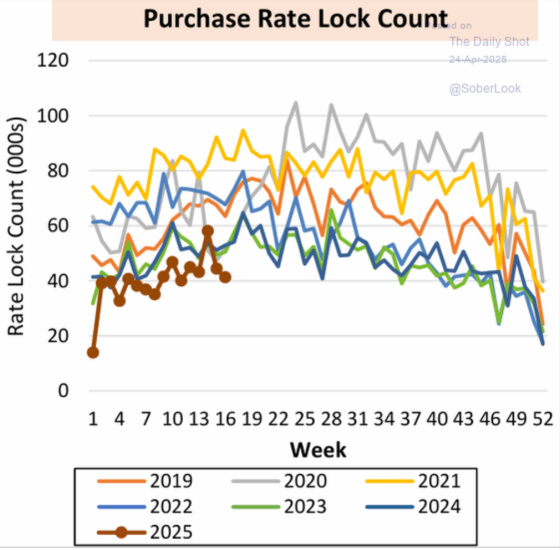

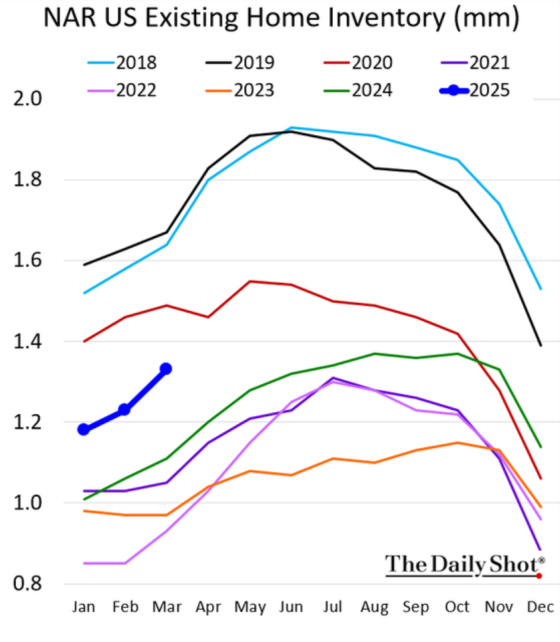

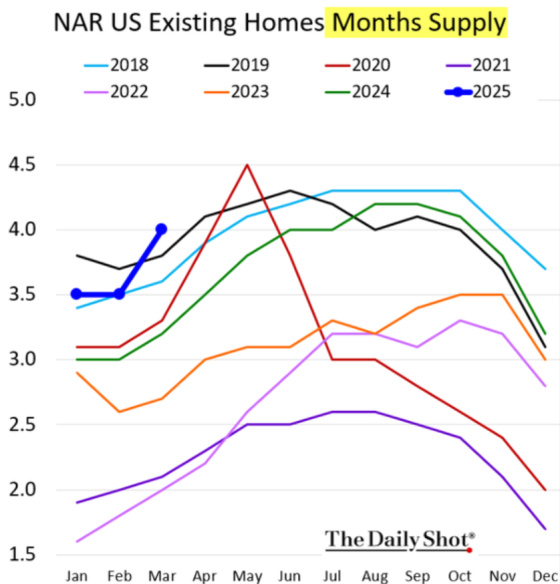

Now that the fuse has been lit on the international trade front such that there will absolutely be a meaningful contraction over the next few months, is there another source of demand that may offset this? What about housing? Sorry Charlie, the news is pretty poor here as well. Existing home sales are quite anemic and with consumer confidence waning, prices still elevated, and mortgage rates high, albeit dropping a bit, I don’t expect a turnaround over the next few months to offset the contraction in trade.

With sales slowing and inventory rising, homes are sitting on the market for a longer period of time.

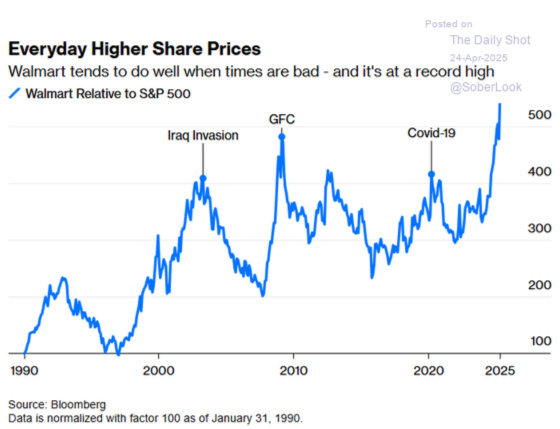

I will wrap it up with this interesting chart related to Walmart. One can see that Walmart’s peak outperformance relative to the S&P 500 occurs during times of maximum economic weakness. We are at another peak so one can take the glass is half-empty approach and say it’s definitely going to get worse before it gets better or the half-full approach and look at it that the worst could be behind us as the previous peaks tended to take place during the worst parts of those downturns.

All I can recommend is to buckle up, stay alert, drive carefully, and keep your distance as you don’t know what might be around the bend in terms of the condition of the road or other cars piled up.

{kind=link}

Leave a Reply