I read a very interesting theory about Donald Trump‘s master strategy when it comes to the trade war with China. Trump believes that he can win a trade war, but he can’t do it alone. He sees that the Chinese are reacting with an aggressive fiscal and monetary stimulus to counter the negative impact of the trade war on their economy and believes the United States needs to do the same.

I do think that Trump does have a pretty good feel for markets and investor psychology and he has criticized Chairman Jay Powell of the Federal Reserve for lacking that. As the following headline and article summary shows, the one thorn in Trump’s side economically has been the Federal Reserve for its unwillingness to lower interest rates as he believes that this is holding the economy back and could get in the way of his reelection.

By being extremely aggressive with China, and now Mexico with tariffs, Trump is not only trying to create more leverage in a negotiation with each of those countries for different reasons, he is also clearly having an economic impact on the U.S. economy that is not positive. I think he’s willing to take the risk that the impact on the stock market will be short-lived because if he can force the Federal Reserve to loosen policy then I think he believes that the stock market will not be hit too badly as it will encourage investors to take on more risk and it will also help the economy and improve his chances for reelection.

It appears that J.P. Morgan’s chief economist agrees that the Fed will have to ease as he writes the following via Zero Hedge:

In the dovish corner, we have JP Morgan which as of this morning has turned so bearish that the latest report from the bank’s chief economist, Michael Feroli, says that

“Making Abysmal Growth Attainable” again would require not one but two rate cuts before the end of 2020!

As Feroli writes, “last night’s tariff announcement adds yet another trade-related headwind to the growth outlook. If the Administration follows through on the proposed actions, we believe the adverse growth implications would prompt Fed easing. Even if a deal is quickly reached with Mexico, which seems plausible, the damage to business confidence could be lasting, with consequences that might still require a Fed response.”

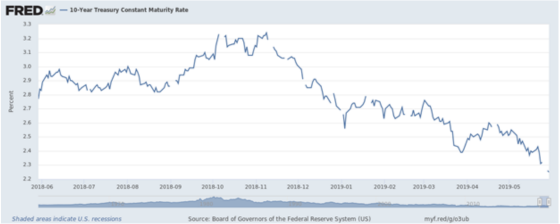

I don’t believe that you win trade wars. They are generally inefficient as they sever very efficient supply chains and raise prices across the board and reduce buying power. But that’s not the purpose of this blog. What is unequivocal is that Treasury investors are 100% certain that the economy is slowing and will definitely do so in the future as there has been a significant drop in long-term interest rates by more than one percentage point from their recent peak.

The yield curve is back to being inverted when comparing the 10-year Treasury note yield to the 3-month Treasury bill yield. It’s interesting to note from the graph below that recessions tend to materialize about 18 months after an inversion takes place and when a recession occurs, the curve has already steepened. I will be on the lookout for the curve steepening as a leading recession indicator rather than signaling we are out of the woods.

I was reading an interesting analysis by Moody’s about the inverted yield curve and some of the historical precedents if it stays at this level for a period of time. This is what Jon Lonski says about inverted yield curves and recessions, which is generally consistent with what I observed.

For the three last recessions (including the Great Recession), the initial meaningful inversion of the Treasury yield curve led the arrival of a recession by a seemingly long 16 months, on average. Thus, if June 2019’s month-long average shows the fed funds rate topping the 10-year Treasury yield by at least 10 bp, the next recession may not arrive until October 2020, or just in time for the next Presidential election. During the 2002-2007 business cycle upturn, the federal funds rate first topped the 10-year Treasury yield’s month-long average by at least 10 bp in June 2006. Thus, 19 months elapsed between the initial meaningful inversion of the Treasury yield curve and the December 2007 start of the Great Recession.

And when it comes to what inversions mean for future short and long-term interest rates, history suggests they will be lower.

Recently, the 10-year Treasury yield was 11 bp under the fed funds rate. In terms of the month-long averages since 1984, there have been 42 months where the federal funds rate topped the 10-year Treasury yield by more than 10 bp. For 32, or 76%, of the 42 months, the 10-year Treasury yield was lower 12 months later. Moreover, in 40, or 95%, of the 42 months, the federal funds rate was lower 12 months later.

The latter statistic explains why markets now strongly expect a Fed rate cut by the end of 2019. As inferred from the CME Group’s FedWatch Tool, the futures market implicitly assigns a probability of 57% to a rate cut at the September 18, 2019 meeting of the FOMC, where the implied likelihood of a less than 2.375% midpoint for fed funds soars to 84% at the December 11, 2019 meeting of the FOMC.

And finally, Lonski also shows that the high yield credit spreads tend to widen over the next 12 months. This is not surprising as loan quality deteriorates and investors demand greater compensation for more perceived risk. From a real estate borrowing perspective this should translate to higher spreads as well, somewhat offsetting the lower Treasury yields.

It will be interesting to see if Donald Trump’s sons aggressively pursue refinances of his personal properties now that he has helped engineer long-term rates lower. If so, then maybe he is a stable genius.

{kind=link}

Gary,

With treasuries at 211 today, June 3rd, have you had any more conversations around fixed rates? You linked to your past post titled, “Obsessed by Curves: Yield Curves That Is” from April. I, myself, wholeheartedly believe in one taking a hard look at the ability to have flexibility built into the financing strategy; especially due to the general nature and cyclical market of Class A apartments. I believe your book gave a great ride into the sweet times and sorrow times around real estate debt financing and its place within an investment strategy.

With that being said, this is a level we haven’t seen since early September 2017. CWS actively manages its assets with the long term in mind, and I could imagine debt brokers reaching out due to the strength of the firm and its assets while having a large amount of variable rate in place. Granted, this current economic climate and trying to forecast a strategy is certainly one to remember – especially being that history forecasts that they will go even lower.

Thanks for the thought exercises on a weekly basis.

-Carl

Clever article with amusing ending : >